Ciaran Fitzgerald: Inflation issues - action required

Inflation has become a major issue as Ireland and, indeed, the whole world emerges from the Covid-19 recession.

Ironically and, perhaps, significantly, in the context of global decarbonisation challenges, a notable element of global inflation increases derives from increased prices of fossil fuels such as coal, gas, and oil.

Discussion in Ireland of how inflation can be mitigated, if not controlled, has involved a lot of heat - understandable, given the impact of energy prices - but not a lot of light.

There has been little, or no, discussion, or analysis, of the global causes of price inflation - in terms of rising prices of fossil fuels such as oil, gas and coal - in the context of post-Covid-19 global economic recovery.

Nor has there been a discussion about what this means for the longer-term challenge of decarbonisation of economies, which is required to halt global climate changes.

Where does food and agriculture fit into this?

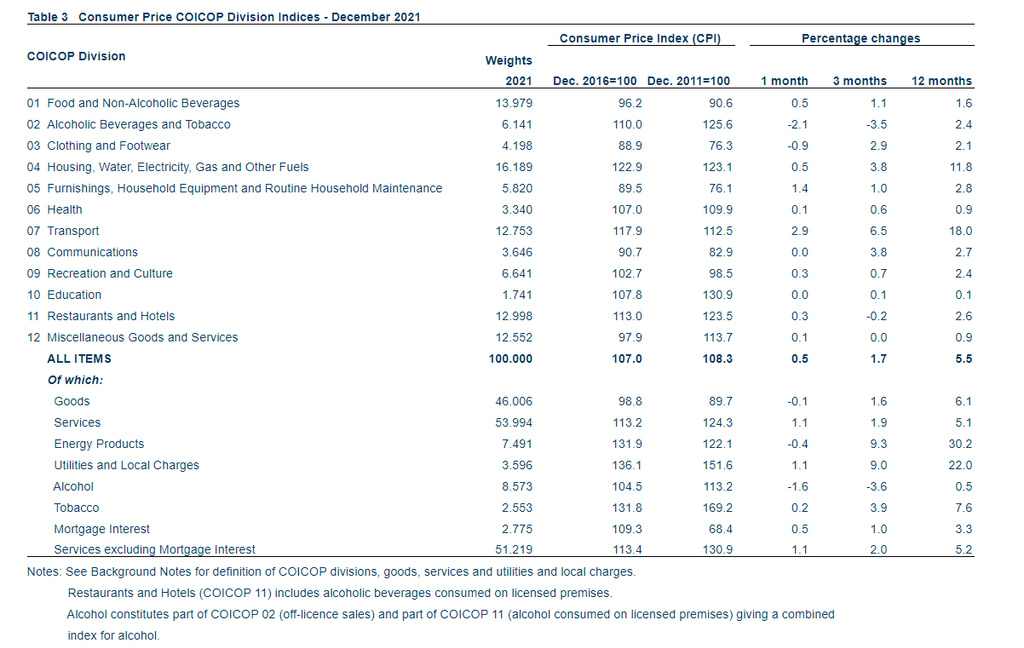

As I have stated in previous articles and, as per the table below from the Central Statistics Office (CSO), food prices have only gone down over the last 10 years, or more.

The CSO table shows that food prices in Ireland, as of December 2021, were at 90% of the prices in December in 2010.

The overall cost of living has increased by 8% over the same time period, which means that the real price of food has fallen by 18%.

In essence, food pricing has become totally disconnected from food-production costs in Ireland.

The difficulty for farmers and food processors in pointing out that this cost-price squeeze is unsustainable is that, politically, the mood music will say that this is a great outcome.

Indeed, at a level, there will be sympathy for farmers that prices have not moved in line with production.

But this tends to morph into the usual pantomimed discussion around why processors aren’t passing back higher returns to producers when, very clearly, the figures from the CSO show that there has been nothing to pass back.

It is hugely important - both in the context of the current price/cost squeeze and the impact of new decarbonisation legislation on the agricultural sector - that the real dynamic of this unsustainable disconnect between production of food and food prices is understood, and addressed.

Understanding and addressing

Fresh-food products, in particular, are being sold by supermarkets and discounters at, or below, cost. These are sold as loss leaders to consumers who, in a typical grocery shop, will purchase 50 items of which they are price sensitive to five or six.

The grocery retailer, supermarket or discounter takes a margin hit on the fresh food but recovers this, and more, across the remaining products.

There is no such margin recovery for the fresh-food supplier who is being slowly strangled in a manipulated price-cost squeeze - as indicated by the CSO figures, down 18% in real terms since 2010.

This cannot go on. And, yes, it can be stopped.

As I have said before this form of predatory/dominant pricing is not allowed in a whole cast of retail products, which are very dear to consumers' hearts including:

Given the recent uproar around inflation pressures, and criticism of government actions to address same, there is unlikely to be a great welcome for a food processor or farmer demand for fair-trade legislation that will be perceived as more bad news for the struggling consumer.

But to be very clear, what we know is that supermarkets carry between 15,000 and 25,000 single grocery items - stock keeping units (SKUs).

Discounters carry, on average, 1,500.

At the moment, the 50-100 fresh-food SKUs such in fresh dairy, meats and vegetables are being sold at no, or low, margin while the retailer margin is earned on the remaining products.

So, instead of doing nothing, which has been the policy of the last 16 years, can government introduce fair-trade legislation that states that a defined group of the fresh food products must be sold at cost-plus level?

The cycle of the last 20 years of retailer-dominated, relentless-downward or everyday-low pricing is totally out of kilter with consumer demand for renewable and sustainable food, and at odds with EU and national legislation and regulation intended to deliver on this sustainability agenda.

So, rather than expecting the food- processing sector and farmers to continue to suck up increased input costs, the food retailer must be compelled to do the right/sustainable/renewable thing - spread their margin earning capability across the full range of products to include fresh food.