Beef kill: Weekly cattle supply falls as prices edging up

Weekly beef kill figures have been in decline for the past four consecutive weeks up to the week ending Sunday, March 24.

While last Monday, March 18, was a bank holiday, resulting in a four-day kill at most factories, the general consensus is that cattle supplies on the ground are beginning to tighten slightly.

It remains to be seen what impact the wet weather throughout March will have on finished cattle supplies, however some procurement staff expect it could result in additional cattle availability in May, as farmers opt to keep cattle housed for finishing.

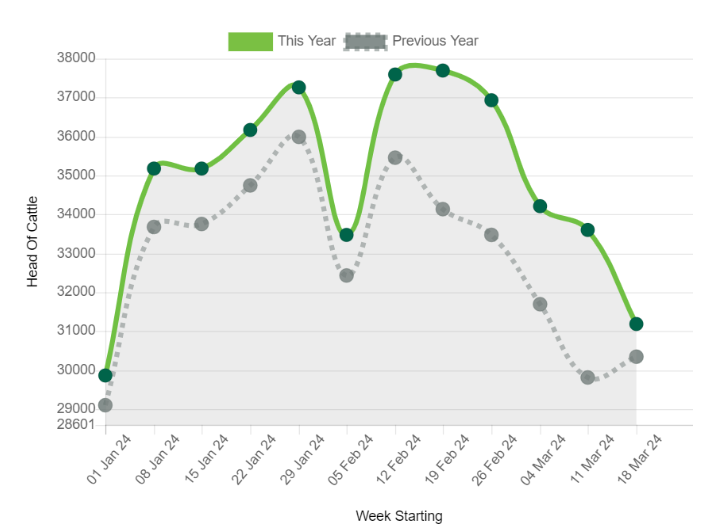

While weekly cattle supplies are in decline, interestingly, the total beef kill to date this year is running ahead of last year.

The graph below shows the weekly kill numbers in the past 12 weeks of this year versus last year:

As of Sunday, March 24, a total of 418,295 head of cattle have been slaughtered at Department of Agriculture, Food and the Marine (DAFM)-approved factories (excluding veal).

This year's cumulative beef kill is over 23,600 head of cattle ahead of the same time last year.

The table below gives an overview of the beef kill in the week ending Sunday, March 24, versus the same week last year and the overall supply this year versus last year:

| Category | Week ending March 24 | Equivalent Last Year | Cumulative 2024 | Cumulative 2023 |

|---|---|---|---|---|

| Young bulls | 1,706 | 2,038 | 32,610 | 34,728 |

| Bulls | 550 | 632 | 5,038 | 5,346 |

| Steers | 12,017 | 11,257 | 146,772 | 140,709 |

| Cows | 7,605 | 7,304 | 107,142 | 92,867 |

| Heifers | 9,296 | 9,118 | 126,733 | 121,015 |

| Total | 31,174 | 30,349 | 418,295 | 394,665 |

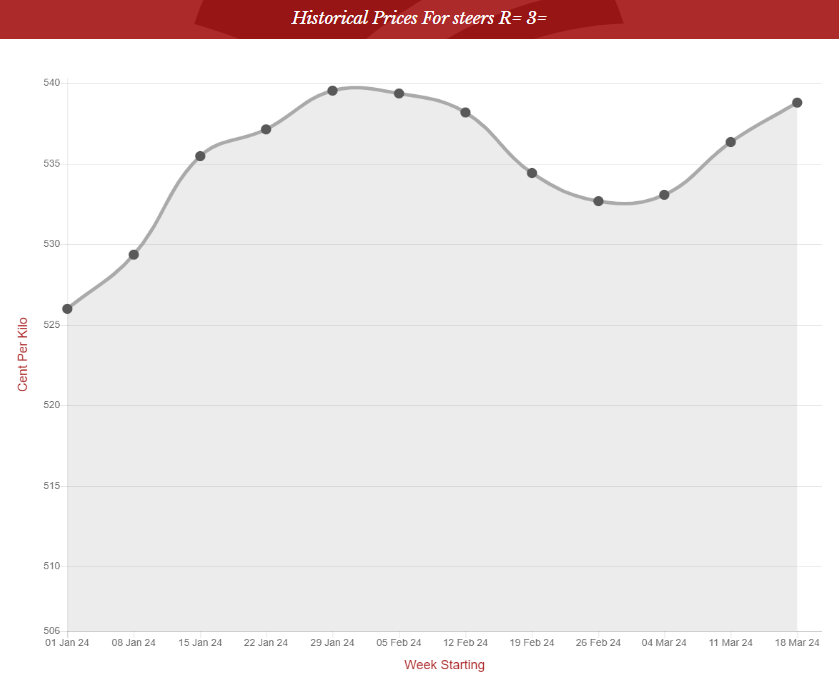

While cattle supplies have fallen for the past four consecutive weeks, the average R=3= grade steer (bullock) price has increased for the past three consecutive weeks.

The graph below shows the average R=3= grade steer price over the past 12 consecutive weeks:

In the week ending Sunday March 24, the average price paid inclusive of all bonuses for R=3= grade steers was €5.39/kg.

Further information on prices paid on a factory-by-factory basis is available to view by clicking here.