EU to become the largest producer of wheat by 2032

The EU will soon become the largest exporter of wheat in the world but worldwide growth of cereals is projected to slow down and the area of cropland in Europe is also likely to decrease, according to a new report.

The worldwide growth of overall cereal demand is expected to be slower over the next decade than it was in the past decade, due to slowing growth in feed demand, biofuels, and other industrial uses.

In western Europe, per capita food use of cereals is expected to be stagnant, or even declining, due to low population growth and consumer preferences moving away from staple commodities.

These figures outlining the projections of cereals in the EU and the rest of the world are detailed in the latest Agricultural Outlook 2023-32 report published by the Food and Agriculture Organisation of the United Nations (FAO) and the Organisation for Economic Co-operation and Development (OECD).

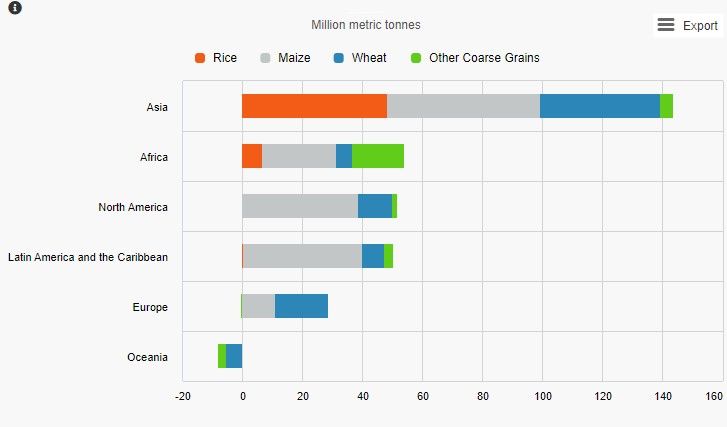

Production trends

The report shows that in western Europe, cropland is projected to decrease, since any increase in crop production is tightly regulated by policies on environmental sustainability, and as land used for fruits, vegetables and other crops is expected to decline.

In Europe, the report highlights that income growth will reduce per capita demand for basic foodstuffs, in particular for cereals, and thus facilitate a shift in consumption towards foods of higher nutritional value, most importantly in items that are dense in micronutrients such as fruits, vegetables, seeds, and nuts.

The EU is projected to become the largest producer of wheat by 2032, overtaking China, where wheat production is responding to demand decreases from negative population growth.

The EU, the second-largest wheat exporter, will account for 17% of global trade in 2032, although exports are projected below the record volumes of 2019 and 2022, according to the latest Agricultural Outlook 2023-32 report.

Compared to the base period, the EU is expected to maintain international market shares mainly due to constrained growth in the Black Sea region.

The export share of the top five maize exporters – the US, Brazil, Argentina, Ukraine and Russia (overtaking the EU as fifth-largest maize exporter) – will account for 88% of total trade towards the end of the projection period.

Mexico is projected to become the largest maize importer as import growth in the EU is slowing down and China’s imports are projected to stay below the large volumes in 2020 and 2021 which made the country the top importer.

The top five exporters of coarse grains, the EU, Australia, Russia, Canada and Argentina, are projected to account for 78% of global trade by 2032.

Feed and other uses

According to the latest Agricultural Outlook 2023-32, this year 41% of all cereals will be consumed by humans and 37% will be used for animal feeds, with the remaining 22% to account for biofuels and other uses.

While the EU is the second-largest user of protein meal, consumption is expected to decline as growth in animal production slows and other protein sources are increasingly used in feed.

By contrast, southeast Asia's animal production is increasing and is projected to raise demand for imports of protein meal.

In the EU, protein meal consumption is expected to grow at a slower rate than animal production due to improving feeding efficiencies.

In addition, animal products, primarily poultry and dairy, are increasingly marketed in the EU as produced without feed use from genetically modified crops, driven by large retail chains that results in lower demand for soya bean meal.

In the EU, most protein meal production comes from the crushing of imported oilseeds, primarily soya beans from Brazil and the US.

Production of other oilseeds is projected to increase at a slower rate compared to the last decade, due to increasing competition by cereals for limited arable land in China and the EU as well as stagnating demand for rapeseed oil as a feedstock in European biodiesel production.