Ciaran Fitzgerald: What does Irish food production do for us?

It's that time of year again where a plethora of state agencies and research bodies will set out their assessment of the prospects for the Irish economy in 2023, often overlooking Irish food production.

Without sounding like a broken record, none of these agencies, as exemplified by the recent reports from the Economic and Social Research Institute (ESRI) or the Central Bank, make any reference to the outlook for Irish agriculture or agri-business.

Any objective assessment of Irish economy prospects must surely have something to say about a business sector that supports 220,000 jobs (almost one job in 10 in the Irish economy - CSO).

Perhaps even more importantly, as an industry that accounts for 30% of the total expenditure in the Irish economy by all business, indigenous and multinational.

Irish food production

This lazy and superficial 'consensus' among the great and the good in economic analysis, that refuses to look under the bonnet of the realities of multinational flows through the Irish economy that have a tiny Irish economy footprint, while ignoring the broad agri-food sector that spends €17 billion in the Irish economy annually, beggars belief.

The failure to delve a bit deeper into real Irish economy transactions is even more reprehensible, given that the Annual Business Survey of Economic Impact, as outlined in the series of charts below, is both accessible and very informative.

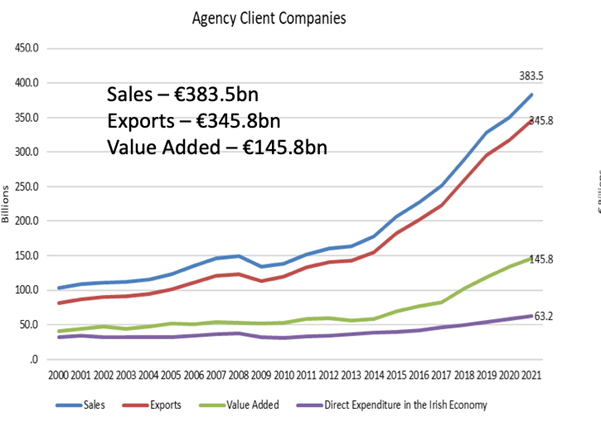

The first chart above outlines the overall performance of all business sectors, and the key takeaway is that while sales and exports account for €385 billion approximately, direct expenditure in the Irish economy is €63 billion.

The clear point here is that while sales and exports is a measure of the global performance of businesses, expenditure in the Irish economy is a true assessment of the impact of these businesses in Ireland.

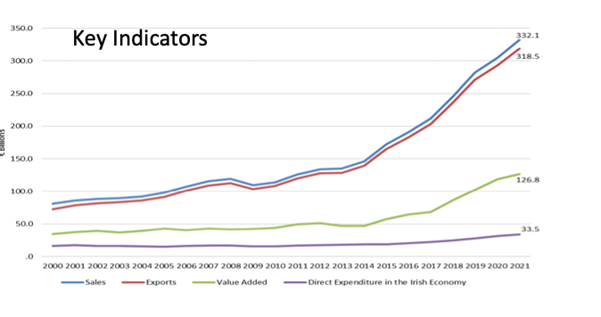

This skewedness (shown in the graph below), is particularly acute for the multinational sector and demonstrates that for every euro of exports (totalling €330 billion) only 10c (€33 billion) is spent in the Irish economy.

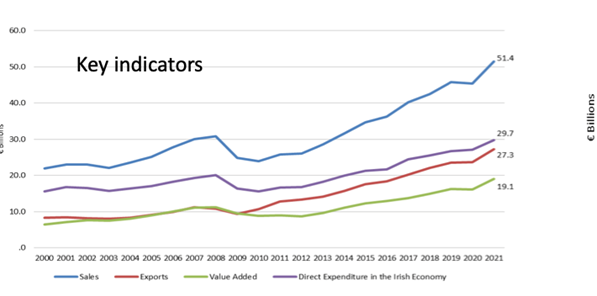

In contrast, the chart below shows that for the indigenous businesses of which agri-food accounts for 60% of total economic activity, export value is more closely related to Irish economy expenditure and thus Irish economy economic impact.

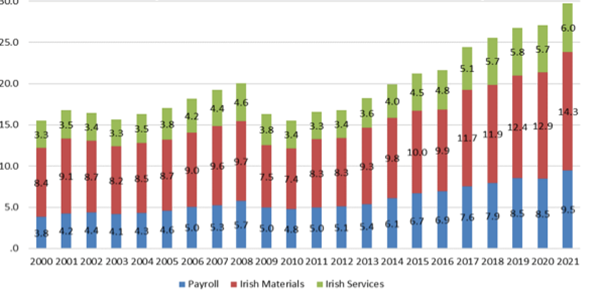

The next chart from the report breaks down the Irish economy by the indigenous business expenditure (including agri-food) by category, with by far the biggest spending category being on Irish raw materials.

This is in contrast to the multinational sector where wages are the biggest spending heading.

To be very explicit, as confirmed by the Central Statistics Office (CSO), we know that the value of Irish agri output in 2021, which is reflective of the price of raw materials purchased by the food/drink sector, was in excess of €10 billion.

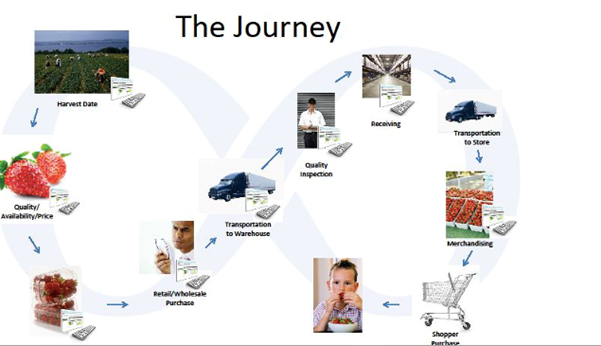

Moreover, as again confirmed by the CSO, and as outlined schematically in the flow chart above, the Irish economy multiplier impact of raw materials purchased from the Irish economy is at least double the impact of expenditure on wages or services on Irish economy performance.

So, in summary, Irish economy expenditure, rather than the monetary value of sales or exports that have low or no Irish economy footprint, is a much more reliable indicator of real Irish economy activity.

Economic report

Fortunately, Enterprise Ireland on behalf of the Department of Enterprise, Trade and Employment, produces a detailed annual report which is both accessible, definitive and informative.

It is not in any way dismissive of the impact of the multinational sector on the Irish economy, but is balanced and realistic as an assessment of the multi-dimensional aspects of Irish economy impact.

In particular, it acknowledges the key role played by an agri-food sector that spends €17 billion, at a multiplier impact of 2.0 equivalent to €34 billion in cumulative expenditure in the Irish economy.

Clearly for the agricultural sector, 2023 looks like a difficult year with a distinct possibility that the pace of decline in output prices will be greater than the fall in the price of inputs, particularly in the dairy sector.

However, at the same time and again based on objective criteria underpinned by reports from the FAO/OECD and EU Commission, we know that the demand for Ireland’s grass-based agri-food output is increasing, underpinned by strong global demand for sustainable food production.

We also know that in addition to the ongoing challenges of price and income volatility for the sectors across Irish agriculture, the huge cost of decarbonisation from farm to factory looms large to meet both global customer and regulatory requirements.

Balanced economic analysis, based on an informed, realistic assessment of Irish agriculture's unique economic impact does not in any way take away from the 'focus' on multinational inward investment.

However, it does better reflect the necessity to be more than an economic one-trick pony.