Ciarán Fitzgerald: What did supermarkets ever do for us?

The ever growing shortages of food produce on the shelves of supermarkets in Ireland and the UK are raising, yet again, significant concerns that the current grocery/food supply chain is inherently fragile and not sustainable.

As I previously stated, the whittling down of local food production capability in the name of supply chain efficiency over the last 20 years means that there is no local capability, particularly in fruit and vegetables, to replace international supply, which is creaking because of climate challenges or other disruptive factors.

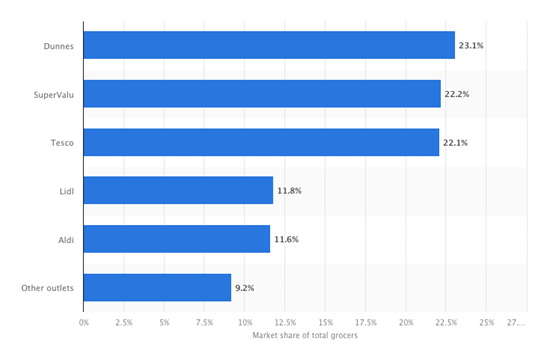

Across the EU and the UK, 3-5 large supermarkets/discounters account for 80% or more of total consumer spend on groceries.

In Ireland, the big three supermarkets of Dunnes, Tesco and Centra/SuperValu plus Aldi and Lidl account for just over 90%.

While supermarkets and discounters are in the firing line in terms of ignoring the resilience factor in supply chains in pursuit of everyday low-price supply, food policy thinking by national governments in Ireland and the UK and EU in the early 2000s is at the heart of the current hiatus.

The quid pro quo for allowing supermarkets and discounters dominant buying power was an assurance to government that food price inflation would be all but eliminated.

As we know, prior to last year's energy price and war-based surge in inflation, food retailers could point to the fact that in the period from 2011 to 2021, food prices actually fell by 11%, whereas overall inflation in the Irish economy was 7%.

This meant that in real terms, food prices actually fell by 18%. No surprise that local supply sources became uncompetitive.

An additional element to this lazy thinking was the simplistic approach to globalisation that food production in the EU would naturally taper off, as the EU became a services economy, to be replaced by supply from emerging economies like Brazil and Argentina for meat and dairy produce and Morocco/Alegria for fruit and vegetables.

The culmination of all of these ideological misconceptions is made more acute perhaps by the shock in terms of energy supply realities that the same type of magical thinking exposed last year.

The big takeaway here I would suggest is not that supermarkets/discounters are intrinsically inefficient, but that dominant buying power, by its nature, is focused solely on delivering bottom line returns for the supermarket/discount business.

Supermarkets and pricing policy

Dominant buying power is therefore, as we have seen, totally unfit for the role of balancing all of the parameters of efficient grocery food markets.

The crazy thing is that governments and the EU, in terms of its competition and markets policy, know this across a range of markets and vital consumer products.

They know this when it comes to the structure of energy markets, for instance, whereby the entity that controls the grid cannot be allowed to operate in consumer markets.

They also know this in terms of insisting that new/renewable sources of energy are supported by a supportive feed-in tariff that ensures new product innovation from sustainable sources can enter the market.

Energy pricing policy thus supports long-term investment and equally ensures that new product/renewables cannot be sold below cost.

Pricing policy in markets such as mobile phones and pharmaceutical drugs reflects the reality that dominant buying power does not deliver well functioning markets, but that selling power does.

These products cannot be sold below cost, unlike grocery products, nor can the producer/supplier be forced to provide an 'own label' supermarket competitor to its brand.

Selling power reflects the reality that without cost recovery, producers can't fund investment in new products, and lo and behold, consumers and regulators are comfortable with this.

Regulation

So, while it may not be possible to apply, in its entirety, the energy sector price and supply structures to the agri-food sector, or to treat fresh food products as equivalent to pharma drugs or mobile phones, food pricing regulation must change.

Because the current policy of allowing fresh food to be used as a loss leader never worked for the food production sector, and it now is clearly not working for the consumer.

The new fair trade legislation on Unfair Trade Practices (UTPs) will not deliver the fundamental change that is required to remedy the dislocation between the ever increasing cost of food production and low- or no-cost recovery.

Indeed, this gap is likely to increase as we see consumer preferences for the carbon footprint of food products reflected in new food labelling requirements.

A balanced supply chain for Irish food producers and consumers requires a clear route to cost recovery through an end to dominant retail pricing.