Ciaran Fitzgerald: Inflation has many impacts on agri sector

The year 2022 was a challenging one for the agri sector, but with output prices performing better than expected, the huge inflation in energy, fertiliser and general inputs costs - driven by both the Ukraine invasion by Russia and the post-Covid-19 supply chain adjustments - was just about managed.

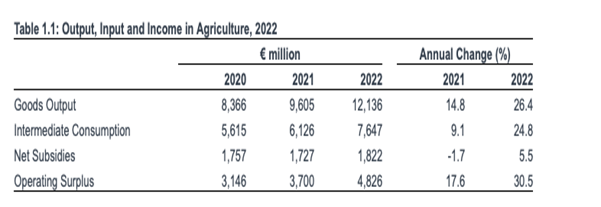

As per official Central Statistics Office (CSO) estimates for 2022, Irish agricultural output price inflation at 26.4% just about topped input costs, which increased by an average of 25%.

We know that, in more detail, fertiliser costs increased by over 175% and feed costs increased by more than 30%.

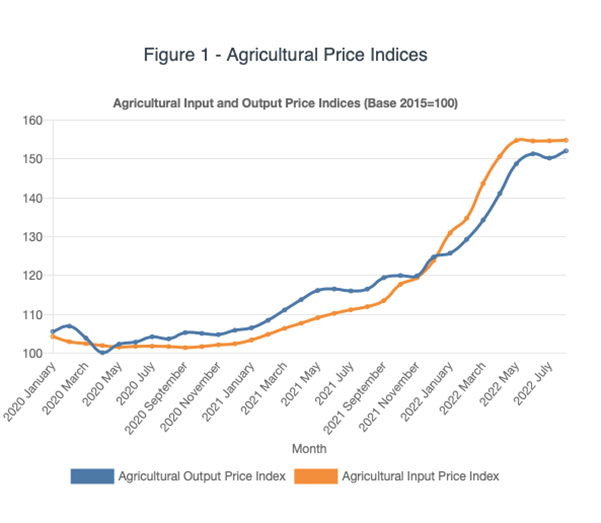

As the chart below highlights, for the farming sector, the relationship between input and output price inflation is very much a tightrope affair over time.

So, in many respects, the inflation in food prices in 2022 was hugely welcomed by the agri sector.

It came as a sea change from the pattern of food price inflation over the decade since 2010, which had seen food prices actually fall in both real and relative terms.

However, as we know, agri output prices are not the only source of income to the sector, with Common agricultural Policy (CAP) payments representing a varying, but very significant, part of incomes across the agri mix, from tillage and livestock production to dairy production.

Inflation

A recent paper on the impacts of inflation on the real value of CAP payments by the French-based think-tank 'Farm Europe' suggested that because the latest CAP was negotiated based on 2% inflation, the 8-10% inflation experienced in 2022 had reduced its real value by a gross figure of €85 billion.

€69 billion of this was arising from inflation reducing the value of Pillar I payments and a further €15 billion in Pillar II payments.

According to Farm Europe, ”record inflation, now 10% compared to the 2% when the CAP budget was set, could lead to a reduction in the real value of support”.

The organisation added: "Based on the European Central Bank’s inflation forecasts, the first so-called ‘pillar’ of the CAP, aimed at funding direct payments to farmers, stands to lose €68.6 billion.

"This would create quite a dent in the new CAP budget for 2023-2027, which has been set to a total of €387 billion," Farm Europe added.

While the report rightly identifies inflation as a huge challenge for a fixed CAP budget, the report makes the key point that the core issue here is not just fixed supports.

It is a philosophy illustrated most recently by Green Deal measures that promotes higher production costs and refuses to reflect this in the CAP. I believe this is core.

The CAP and EU policy for the agri-food sector has always been highly prescriptive and interventionist when it comes to food regulations and food standards, whether at farm or factory level.

The rationale or justification for this has been that the EU consumer demands quality and integrity and above all, food safety. No argument there.

Where this philosophy breaks down however, is in regard to the price of food in the EU and in particular the use of dominant buying power by a plethora of food retailers, supermarkets and discounters.

They price a range of fresh, highly regulated food products at, or below, cost and use them as loss leaders.

The disconnect is best framed as highly regulated, high-cost food production set against 'laissez faire... you're on your own' zero-cost recovery food pricing in dealing with huge buying power.

EU trade

The internal EU disconnect between the Directorate General for Health and Consumer Protection of the European Commission (DG Sanco), which wants the highest possible food standards, and the Directorate General for Competition (DG Competition), which insists that below-cost selling and loss leading is a robust expression of market forces, also spills over into EU trade deals.

A perennial problem of World Trade Organisation (WTO) negotiations was the complete failure of EU negotiators to do trade deals, whereby the quality and safety specifications for imported food had to mirror those imposed on EU producers.

The inflation issue is real in its own right and clearly has the capability of undermining CAP supports.

The most efficient and fairest way of addressing this would be to apply an inflation co-efficient to the CAP payments, where core inflation has exceeded, say, 4% or double the standard 2%, upon which the CAP is negotiated.

What the inflation challenge also highlights however is the bigger disconnect that exists between EU policy makers in trade and competition who, by their actions, promote cheap food, and the regulators in DG Sanco and agriculture, who insist on ever higher standards, input usage constraints, and ultimately higher production costs.

Perhaps the chaos in the EU energy market might persuade those dismissive of the CAP and EU agri to think again.