Beef kill: Steady supply but short kill-weeks continue

While the supply of factory cattle dropped slightly last week, the overall trend in the past 10 weeks would show weekly supplies are gradually increasing, meaning weekly supply has been relatively steady.

Many beef processing sites are continuing to operate four- and three-day kills as the total number of cattle slaughtered to date this year (excluding veal) is 34,000 head below last year's supply level.

The dip in supply comes following a record-high cattle kill last year and Bord Bia has projected overall supplies to remain below last year, but it expects supplies in the final quarter of this year to increase.

The table below gives an overview of the beef kill to date this year:

| Type | Week starting July 3, 2023 | Equivalent Last Year | Cumulative 2023 | Cumulative 2022 |

|---|---|---|---|---|

| Young Bulls | 2,703 | 2,749 | 73,158 | 80,743 |

| Bulls | 530 | 587 | 14,728 | 14,801 |

| Steers | 11,550 | 12,763 | 319,555 | 330,330 |

| Cows: | 8,503 | 7,945 | 206,208 | 213,522 |

| Heifers | 9,301 | 8,999 | 254,037 | 262,346 |

| Total | 32,587 | 33,043 | 867,686 | 901,742 |

As can be seen from the table above, supplies of all types of cattle are back, but weekly cow and heifer supplies last week were higher than the corresponding week last year.

The cumulative supply of young bulls has fallen by over 7,500 head. While young bull prices remained strong last year relative to steer prices, the market preference remains for steer beef as opposed to bull beef.

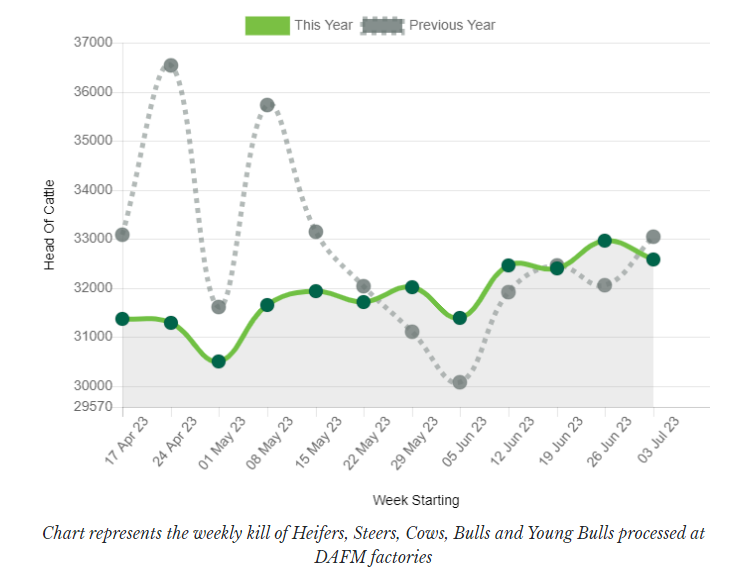

The graph below shows how the beef kill is comparing to last year on a weekly basis:

As can be seen from the graph above, this year's weekly beef kills have remained much more consistent in size than last year's which deviated much more on a weekly basis in throughput numbers.