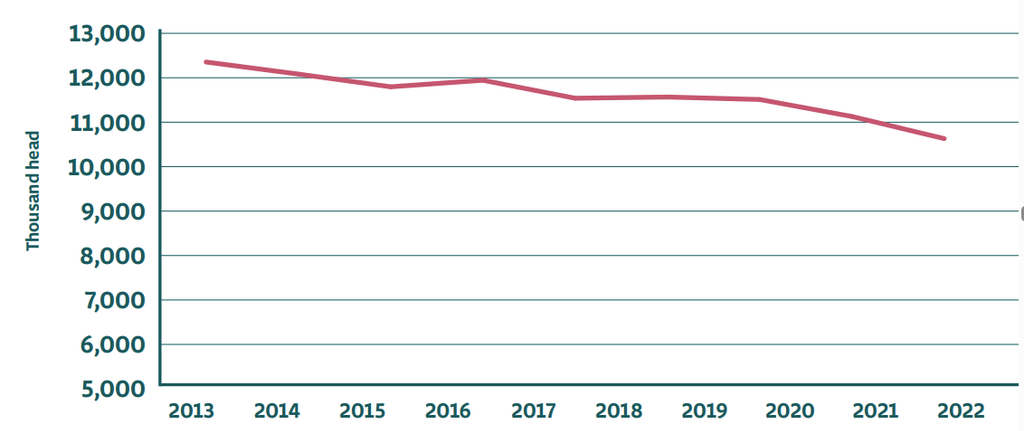

Irish pig producers reduce average holding size

Irish pig producers reduced their average holding size over the past 18 months according to the latest report from Bord Bia.

Minister for Agriculture, Food and the Marine, Charlie McConalogue launched the Bord Bia Export Performance and Prospects report for 2023/2024 today (Wednesday, January 10).

According to the report, Irish pig producers followed the same trend as their European counterparts in reducing the size of their holdings.

This impacted on output levels during 2023 with the volume of Irish pigmeat exports (excluding value-added pigmeat) 20% lower than 2022 levels at 189,000t.

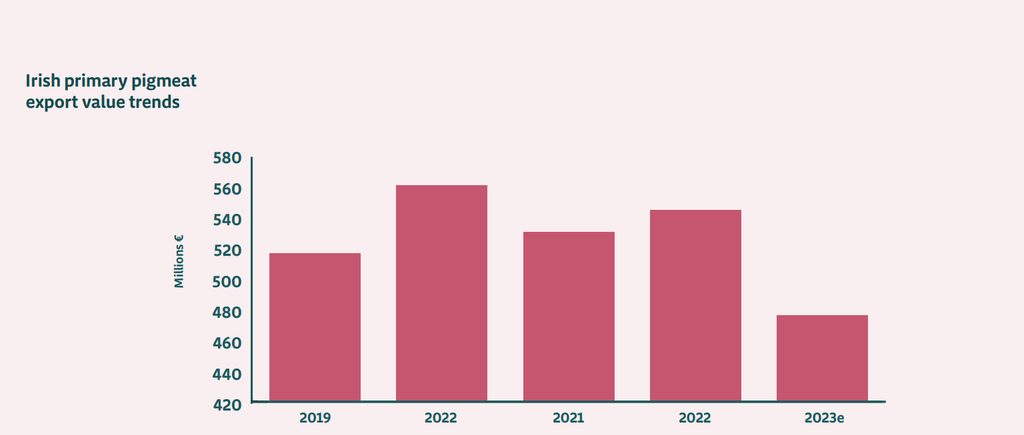

According to Bord Bia, equivalent export values were almost 13% lower at €475 million, despite higher unit pricing offsetting the significant reduction in export volumes as the year progressed.

Pigmeat supply chain

The report also states that changes in international market demand combined with higher costs of production over the last number of years has challenged the EU pigmeat supply chain.

Across Europe, producers responded to low producer prices, rising animal welfare issues and environmental concerns by reducing their holding size in key regions.

According to the Central Statistics Office (CSO), Irish pigmeat production fell by almost 11% to just over 224,000t for the first nine months of 2023 compared to prior year levels, reflecting a decrease in both pig supplies and carcass weights.

For the last quarter of 2023, Irish pigmeat production remained tight as producers took a cautious approach to expanding production against a backdrop of ongoing high relative production costs.

Despite EU pig prices breaking record levels during 2023, pig producers across the EU continued to exit the industry.

The June 2023 Livestock Census showed a decline of 2% or 233,000 head compared to prior year levels.

Significant pig producing member states such as Germany, France, the Netherlands, Poland and Denmark recorded lower numbers (Eurostat, 2023b).

This reflects producers taking a more cautious attitude to expanding production, especially against a backdrop of legacy debt from the cost of production crisis.

Rabobank has previously indicated that in northern Europe, higher animal welfare and environmental standards are forcing some producers to exit the industry.

However, some increase in the Spanish and Italian pig breeding herd helped to partially offset the ongoing decline in European numbers according to Eurostat.

Following on from the record EU pig producer prices that were set during the second half of 2022 in response to tighter supplies, 2023 saw continued strong prices, with Irish prices hitting record highs of €2.24 per kg deadweight excluding VAT by the end of August.

However, some decline in pig pricing was reported during the last quarter of 2023.

Exports

Shipments of Irish pigmeat to international markets fell during 2023 with these markets now accounting for 52% of exports compared to 64% during 2022.

This reflects weak demand across the Asian region, with exports to China, Japan, the Philippines, and South Korea impacted by weak import demand levels as EU pigmeat suppliers were less competitive relative to the US and Brazil, according to Bord Bia.

In addition, due to the pattern of lower Northern American prices throughout the year, shipments of pigmeat to this region were back by 45% to €20 million.

Compensating for lower international demand, exports to the UK increased by 41% to approximately €133 million reflecting extremely tight UK supplies.

Irish pigmeat shipments to EU markets were 7% lower at €94 million.

Outlook

According to the report, global pigmeat production is forecast to remain unchanged in 2024, with lower output in China anticipated to offset increases in Brazil, Vietnam and the United States.

Chinese production levels are forecast to fall by 1% to 56 million tonnes. While the United States Department of Agriculture (USDA) is reporting higher American production, some industry analysts believe that a significant production correction is facing the industry on the back of prolonged losses.

The EU pig industry continues to readjust from weak domestic consumption, and a lack of new markets to replace China by aligning production with lower demand levels.

The European Commission last year stated that EU pigmeat production is expected to increase marginally.

EU production in 2024 is expected to be around 10% lower than 2021, reflecting the structural changes that are occurring which is putting significant downward pressure on production.

Irish pigmeat production is expected to gradually recover from the first quarter of 2024, reflecting some recovery in the pig breeding herd on the back of higher prices and some downward readjustment in production costs.