Ciaran Fitzgerald: Economics 101 totally dismisses Irish agriculture

As we absorb the fallout from the recent coalition government negotiations regarding sectoral climate budgets, it is very hard not to conclude that there is collateral impact for the size and scale of the Irish agriculture sector budget.

Therefore, the debate is far from over. These issues, in my view, derive from a combination of legitimate concerns and 'old chestnut' prejudices.

The ink was barely dry on the government sectoral emissions ceilings when An Taisce, not only announced concerns at what it saw was the low level of aspiration in terms of reduction in agricultural emissions, but sounded a warning that the government would be legally accountable in terms of matching the agreed sectoral reductions with the aspirations previously set out in the Climate Action Bill.

If past performance is an indicator of future action, it is not hard to see the potential for all of this to end up in some form of legal/judicial review activity.

Lobbying

The next area of concern for agriculture has to be the lobbying by several sectors that what is perceived as low targets for agriculture would automatically lead to higher targets for other sectors.

On a purely numbers-based assessment - if agriculture is 37% of emissions, then a low target in agriculture automatically transfers higher figures to other sectors.

However, as everybody and anybody in agriculture, and indeed in the environmental lobby knows, the Paris accord (which is the core agreement behind emissions reduction actions), very specifically recognised the unique importance of food production in delivering a balanced outcome to delivering climate action.

So, despite a vegan view to the contrary, the Paris accord and Intergovernmental Panel on Climate Change (IPPC) methodology recognise that stopping meat and livestock production is not a legitimate response to climate action.

Moreover, as has been previously stated, Ireland could have opted for a system of methane reductions separate to its carbon dioxide (CO2) commitments that would have seen no crossover, but a policy decision was made not to do so.

We can only express disappointment and exasperation that, yet again, the broad public narrative concerning climate change completely excludes the specifics of agriculture and the uniqueness of food in the climate context.

Rather, it focuses on the suppression of Irish cow numbers while ignoring fossil fuels entirely.

Economics 101

The final concern and perhaps ultimately the most damaging, is the continuing dismissiveness in public debate of the economic impact of the Irish agri sector.

Quite a number of the angst-driven statements expressing dissatisfaction with an agricultural emissions reduction target set at 25%, versus 75% in the electricity sector for instance, go on to express horror that a sector that represents only 1.5% of Irish gross domestic product (GDP) is getting special treatment.

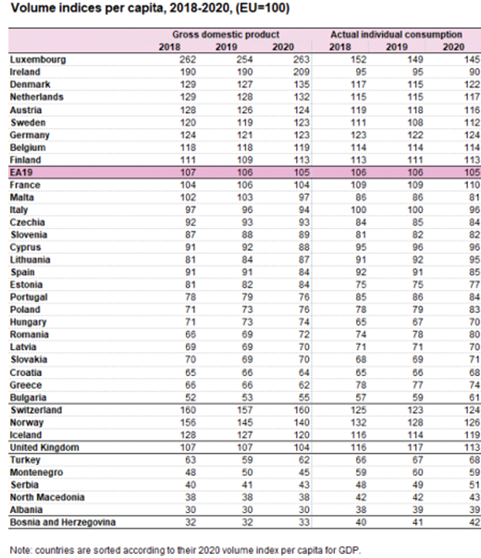

Firstly, can I say that it never ceases to amaze me that despite a multitude of Irish government and EU statistics to the contrary, when it suits an argument, all sorts of so-called economic gurus choose to forget that Ireland's actual economic output is about half of the official GDP figure.

This is because the profits of Apple, Google, Facebook and a large number of US pharmaceutical companies are not ours, or specifically our Minister for Finances, to spend.

As the chart below from Eurostat shows, when account is taken of transfer pricing and multinational profit repatriation, the Irish economy output falls from 209% of the EU average to 90%.

This economic reality is underpinned by an official Irish government annual publication entitled: Annual Survey of Irish Economic Expenditure.

The report demonstrates that while multinational companies export around €280 billion of products through Ireland, their real impact is the €28 billion annual spend in the Irish economy on wages, services and raw materials.

Irish agriculture supports 260,000 jobs across the economy and has Irish economy expenditure of €16 billion - three to four times the level of any other business sector, indigenous or multinational.

Future for Irish agriculture

The agri sector never lacks challenges and while climate budgets and environmental impacts have dominated recent debates, issues like Brexit, market and product diversification, price and income volatility and evolving global consumer demand are ongoing factors that need constant attention and re-evaluation.

As we see an increase in global demand for Irish grass-based agri output, freedom to farm in Ireland has become a core business-risk issue for Irish agriculture.

Based on the public discourse around recent events, it seems to me to be pretty clear that the vegan view and broad environmental lobby is unlikely to let up in terms of their messaging that Irish farming needs 'transformation', i.e. giving up livestock-based production entirely.

Part of the route to articulating how daft and small-minded this agenda is must be through better communicating the true economic impact of the sector and also the real depth of global demand for Irish produce.

But economics 101 needs also to wake up to what is real and what is simply pass-through in the Irish economy.