Ciaran Fitzgerald: Agriculture - complexity and begrudgery

There have been a number of factual reports and analyses published over the last couple of months that objectively point to the fact that Irish agriculture is in implementation mode when it comes to its decarbonisation challenges and improved environmental impact.

A number of these internationally validated reports also underpin the global context of the food demand versus decarbonisation challenge.

E.g., the publication of the new Teagasc 2023 Marginal Abatement Cost Curve (MACC) curve outlines both the roadmap / progress to-date for emissions-reducing production practices.

It captures very succinctly the balancing factors impacting reducing emissions through better adoption of what Teagasc refers to as 'pathway' measures versus reductions through changes in livestock numbers.

Also around the MACC implementation issue looms the difficult question of exit schemes.

Emissions

Meanwhile, the Environmental Protection Agency (EPA) report on national emissions in 2022 showed a reduction in agricultural emissions, while transport emissions continue to grow.

International perspectives highlight strong global demand for dairy and meat.

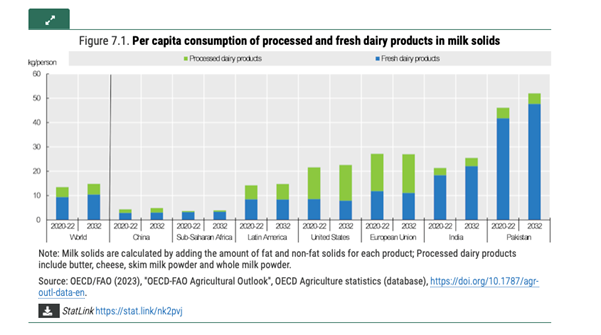

A number of international outlook reports, and most specifically the OECD/FAO outlook report to 2032, show a strong steady increase in global demand for dairy and meat products to 2035 and beyond.

They also highlighted the fact that, with constraints on production in the EU and other regulated production areas, this very substantial increase in global demand, particularly for fresh dairy products, will most likely be met by increased production in non regulated and high carbon-emitting regions.

The chart below outlines dairy consumption trends across global regions.

The OECD/FAO report highlights both the continuing impact of the Russia/Ukraine war on price and availability of key inputs such as fertiliser and feed, and the longer term considerations raised by both the war and the input price rise, with regard to food availability and self sufficiency.

I would argue that both reports, while complex and detailed, are highly accessible in terms of informing the reader as to how the different and often competing economic and environmental pressure points might play out.

Perception of agriculture

This is in direct contrast to the general ignorance surrounding the continuing onslaught in the national media against Irish agriculture which reflects small island politics and equal measures of economic and environmental ignorance.

Recent outbursts from the Irish Times have confirmed a disingenuous narrative that portrays farmers as serial climate deniers and suggest that current local and global weather events are a direct result of government inaction.

A recent article used a 2014 survey of farmers' attitudes to climate change to vilify current 2023 practices.

Think about 2014 - milk quotas were abolished but the quota system was still in place, plus across the economy all debate on climate action had been muted as we and the rest of the EU tried to deal with the impact of the great recession when the financial sector blew up the world economy from 2008 onwards.

We were hoping that dairy growth could provide much needed economic growth, jobs and exports at the time.

But then again, the national media narrative isn’t just negative or blind to current Irish agricultural production methods and their improving emissions profile, but is also dismissive and myopic in terms of recognising the real economic impact of the agri-sector.

This sector supports 220,000 jobs across the economy and is the largest business sector in the Irish economy in terms of expenditure (DETE Annual Survey of Irish Economy Expenditure).

An analysis of the resilience of Irish agriculture over the last 30 years shows a dynamic outward-looking business sector that has successfully engaged in continuous change management.

The Irish dairy sector, post-quota removal in 2015, has increased production from five billion to nine billion litres, delivering an increase in Irish economy spend to €5 billion per annum from €1.6 billion, and has seen the value of exports increased from €2 billion to €6.5 billion euro annually.

Similarly the beef sector in the late 1990s and early 2000s was selling 60% of its output as a frozen beef commodity to markets in north Africa and the middle east and transformed itself throughout the 2000s in to a retail-focused, fresh food sector.

It's hard not to conclude that at the heart of Irish agriculture's adaptive skills is a dynamic capability and 'worldly wiseness' based on a singular focus of delivering what global consumers want and adapting to global trends in sustainable production.

In direct contrast, much 'Dublin 4' commentary is 'informed' by a local small island xenophobic and increasingly 'woke' bubble.