China’s food retail to overtake US as world's largest this year

The Institute of Grocery Distribution (IDG) has outlined that it expects China’s food retail industry to overtake the US as the largest in the world this year.

The IDG forecasts a compound annual growth rate (CAGR) of 6.8% between 2021 and 2026, with the total retail market value expected to reach CNY15 billion by the end of 2026. However, modern trade is expected to outpace this, growing by 8% each year.

According to Bord Bia, China’s retail sector remains highly fragmented, with the total share of the top 10 retailers expected to be just 7.8% in 2026.

The news comes as the Minister for Agriculture, Food and the Marine, Charlie McConalogue is leading his first post-pandemic, full ministerial trade mission to China in cooperation with Bord Bia this week.

As part of the trade mission to China, Agriland took part in a retail expedition around Shanghai on Tuesday (May 16).

The retail sector has evolved rapidly in China with consumers increasingly preferring convenience, innovation, security and quality to price.

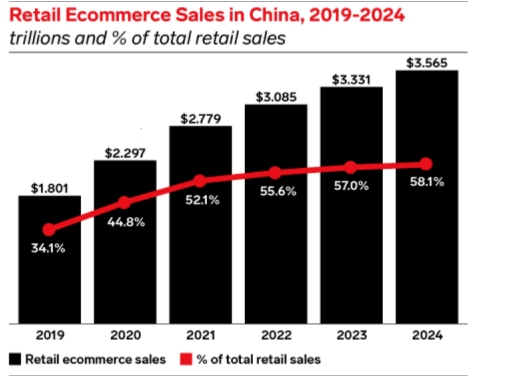

With the rapid expansion of the consumer market and the development of digital technologies, China’s e-commerce industry continues to grow and ranks number one worldwide for its retail e-commerce sales.

In 2021, e-commerce in China contributed to more than half of the country’s retail sales, according to Bord Bia.

The chart below shows current retail and e-commerce sales in China from 2019 to date, and a forecast for 2023 and 2024.

Alibaba’s Taobao and Tmall account for 50.8% of this market share, followed by JD.com with a market share of 15.9% and Pinduoduo with a market share of 13.2%.

These are just some of the domestic platforms that dominate China’s e-commerce market.

Other platforms, including Kaola, Little Red Book (Xiaohongshu), and Dianping, also comprise a large portion of the market share.

Covid-19

Amidst the Covid-19 pandemic, social media emerged as a powerful tool for e-commerce inChina, as retailers increasingly turned to social media to engage with consumers.

According to Bord Bia, social media tools, such as livestreaming, private traffic, and the use of key opinion leaders (KOLs) and key opinion consumers (KOCs), became key drivers of e-commerce growth in China.

Livestreaming in particular has gained immense popularity as a result of social distancing and stay-at-home measures, with brand owners and retailers leveraging KOLs and KOCs to promote their products and generate sales.

Private traffic, which refers to the development of communities on social platforms such as WeChat to interact with consumers directly and regularly, also saw significant growth during the pandemic.

By investing in building online communities, retailers are looking to establish customer loyalty and drive both e-commerce and physical store sales.

Private traffic is especially valuable as user acquisition costs continue to rise, allowing players to lower costs and gain greater control over their relationships with consumers.

As e-commerce continues to grow, Bord Bia expects social media to remain a vital tool for retailers looking to engage with consumers and drive sales.