Beef kill: Supplies steady but no rush of cattle expected

A total beef kill of 32,400 head of cattle was recorded at factories approved by the Department of Agriculture, Food and the Marine (DAFM) in the week ending Sunday, June 25.

While the kill was similar in size to the previous week, the cumulative beef kill to date this year is back by just under 35,000 head.

Earlier this year, Bord Bia had projected the supply of factory cattle to fall by 60,000 head.

This drop in supply was expected primarily in the first half of the year, however as July begins and we enter the second half of the year, the supply has only fallen by a little over half of that.

Supplies could well be tighter than expected in the third quarter of the year, however Bord Bia has projected supplies of finished cattle to be strong in the final quarter of the year.

The table below gives an overview of the beef kill in the first 25 weeks of this year compared to last year:

| Animal | Week ending Sunday, June 25 | Equivalent Last Year | Cumulative 2023 | Cumulative 2022 |

|---|---|---|---|---|

| Young Bulls | 3,646 | 3,034 | 67,393 | 75,167 |

| Bulls | 615 | 635 | 13,463 | 13,693 |

| Steers | 10,885 | 11,329 | 296,314 | 306,070 |

| Cows | 8,701 | 8,992 | 188,987 | 197,110 |

| Heifers | 8,554 | 8,471 | 235,982 | 244,604 |

| Total | 32,401 | 32,461 | 802,139 | 836,644 |

The young bull supply has picked up over the past four weeks rising from 3,000 head in the week commencing May 22, to 3,650 in the week commencing June 19.

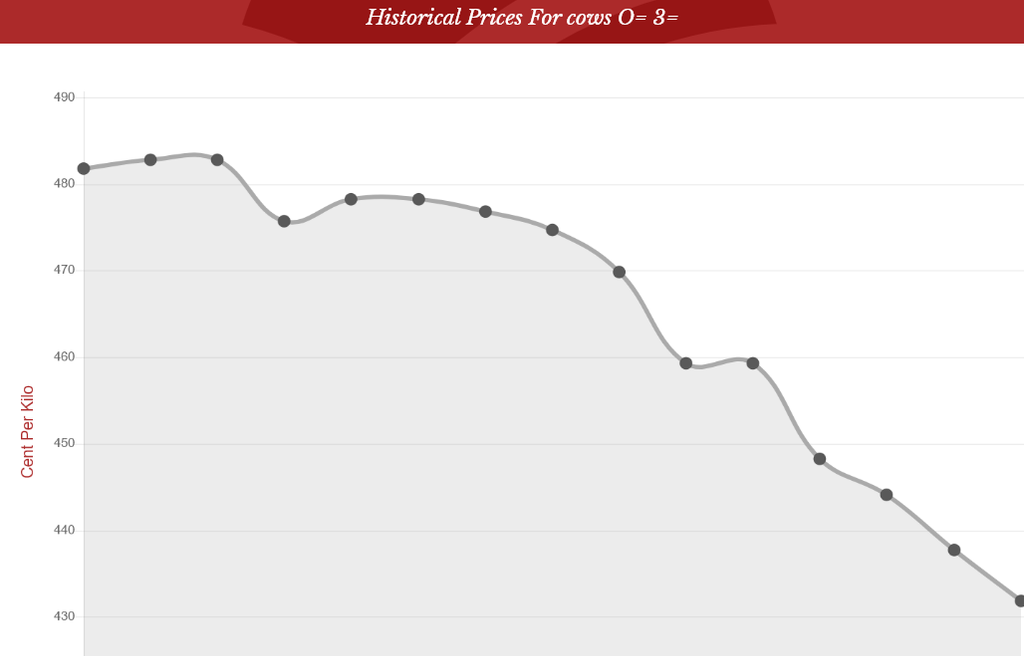

Prime cattle prices in week 25 of this year appear to be back approximately 20c/kg from peak but have fallen further this week (week 26). Cow price has taken the biggest hit with O=3= cows back by 50c/kg from peak.

The graph below shows the direction of travel of cow price over the past few weeks:

As the graph above indicates, the average price per kilogram paid for O=3= grade cows has fallen from €4.83/kg in the week commencing Monday, April 10, to €4.32/kg in the week commencing Monday, June 19.

Supplies of cattle are not expected to increase significantly over July but could well begin to increase significantly into August and from September onwards.