Research: Beef production to decline in Europe in 2023

The global beef market remains solid, according to the latest beef report by Rabobank. However, growing economic and supply-side pressures may change that.

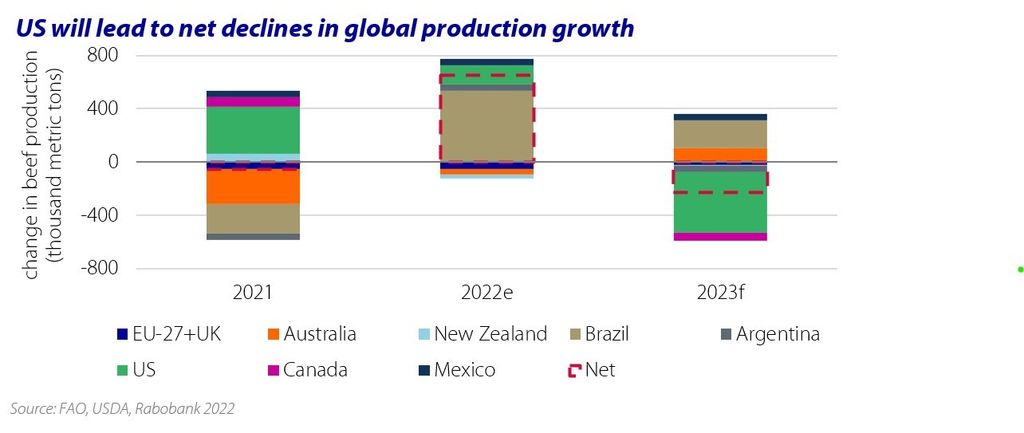

Global production in the first three months (Q1) of 2023 is expected to remain similar to the levels a year ago, but the market should keep an eye on the US, which is headed toward a downward production cycle that will impact prices and trade distribution in the coming years, according to the research.

Rabobank indicates that cattle prices are generally favourable, supported by positive seasonal conditions and resilient consumer demand. But given the slowing economic backdrop – with high inflation and waning consumer confidence – demand may yet soften.

Rabobank beef report

Angus Gidley-Baird, senior analyst – animal protein at Rabobank stated: “We also see emerging supply-side dynamics that will influence markets.

Global beef production is split by hemisphere, with northern countries generally in a declining production phase while those in the south are increasing.

Into Q1 2023, production in Europe and the US is expected to decline, while production in Australia, Brazil, and China should be flat or increase.

New Zealand shows a year-on-year production decline for Q4 2022, but rising production for Q1 2023. Overall, total production volumes for key markets in Q4 2022 and Q1 2023 will likely be similar to levels a year ago, according to Rabobank.

A strengthening US dollar (USD) saw most cattle prices in USD terms contract. But in local currency terms, rises were recorded in Australia (8%) and New Zealand (5%), while Brazil (-7%), Argentina (-4%), and Uruguay (-7%) were down.

The five-area steer price in the US was steady.

Decline in US production to influence market

According to Gidley-Baird, US beef production will begin a four-year decline starting next year.

US production should fall by 3% in 2023, with additional annual declines of 2% to 5% possible into 2026. That is the potential loss of 400,000 to 500,000 metric tonnes of beef production annually.

Previous periods of decline suggest US retailers and restaurants will look to the global market to fill this void, and US consumers will likely outbid the rest of the world to keep their fill of beef.

But other markets are unlikely to fill the gap, due local liquidation (Canada, Australia), structural herd declines (Europe), and trade policies (South America), according to the research.

The net result, according to Gidley-Baird: “We expect the decline in US beef production will not be met by production growth in other major exporting countries.

"Consumers will need to pay to access available supply, given the supply pressures in many markets. This could create a strong upside to prices and the redistribution of trade volumes," he added.