Poultry exports increased by 7% in 2023

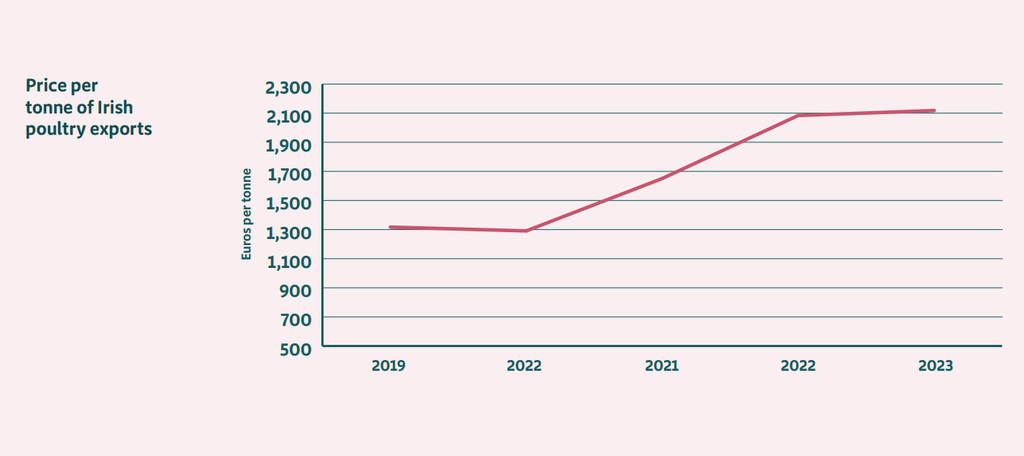

Overall, Irish primary poultry exports increased by approximately 7% to over €170 million during 2023, helped by stronger poultry supplies and slightly higher unit pricing.

That's according Bord Bia's Export Performance and Prospects report 2023/24 which was launched this week (Wednesday, January 10).

The global poultry industry consolidated during 2023 despite weak global economic growth and higher consumer prices according to the report.

The decline in feed prices helped boost output as the year progressed while global demand improved as consumer pricing showed signs of tapering off.

However, Rabobank has said that major operational challenges related to high costs and the impacts of avian influenza (bird flu) are keeping production growth relatively low.

Poultry

The Bord Bia report states that the Irish poultry industry benefitted from firm demand, combined with lower disease pressure in the sector.

Poultry throughput levels up to the end of October were running 4% higher at 95 million head compared to prior year levels according to Eurostat data.

For the main subcategory, chicken, the Department of Agriculture, Food and the Marine (DAFM) indicated that output increased by almost 3% to 85 million head.

This reflects firm demand, with more dark chicken being sold on the Irish market as price sensitive consumers continue to seek value.

According to Kantar Worldpanel, Irish consumer spend on dark chicken meat rose by 36% to €45 million during the 52-week period ending October 29th, 2023.

While poultry meat is the most competitively positioned meat protein, there has been significant price inflation in this category, according to Bord Bia.

The board referenced data from Kantar which showed that Irish poultry retail prices increased by almost 12% for the latest 52-week period.

High Pathogenic Avian Influenza (HPAI) affected the duck industry during 2022, however a strong recovery was evident in 2023.

In Europe, production growth across the region continues to be impacted by HPAI, especially in France and central Europe, and the increased prevalence towards slow-growing chicken, particularly in the Netherlands.

Despite strong seasonal demand for chicken, there has been disciplined industry growth as producers remain cautious against the threat of HPAI and geopolitical tensions that could cause another spike in production costs.

Exports

Increased poultry shipments to the EU helped to offset lower exports to the UK region. Key markets within Europe include the Netherlands, France, Denmark and Germany.

The Bord Bia reports stated that the Spanish market continues to show strong growth reflecting the penetration of the retail channel for dark poultry meat products, with exports more than doubling to almost €9 million during the year.

Elsewhere, poultry shipments to international markets were 19% higher at over €36 million.

Market access conditions to South Africa improved during the year, and exports also increased to other African markets such as Guinea, Ghana, and Benin.

Outlook

The outlook for the global poultry industry will be helped by improving demand and lower costs in 202, Bord Bia has said.

Europe’s market conditions look positive, but the industry faces pressure from rising imports, especially increased chicken imports from the Ukraine which jumped by 78% for the year to July.

European consumer spending is expected to come under further pressure. This squeeze on spending, according to Rabobank, is likely to cause further switching into the chicken category, with pork pricing expected to remain at elevated levels.

The United States Department of Agriculture (USDA) has also stated that HPAI remains a concern for the global poultry industry, and now that the virus has spread to most regions, increased global risk for production and trade will be evident.

If commercial flocks in any of the three key Brazilian producing regions are impacted, then the effect on global markets could be significant for the animal protein sector.