Looking back at the 2022 sheep kill

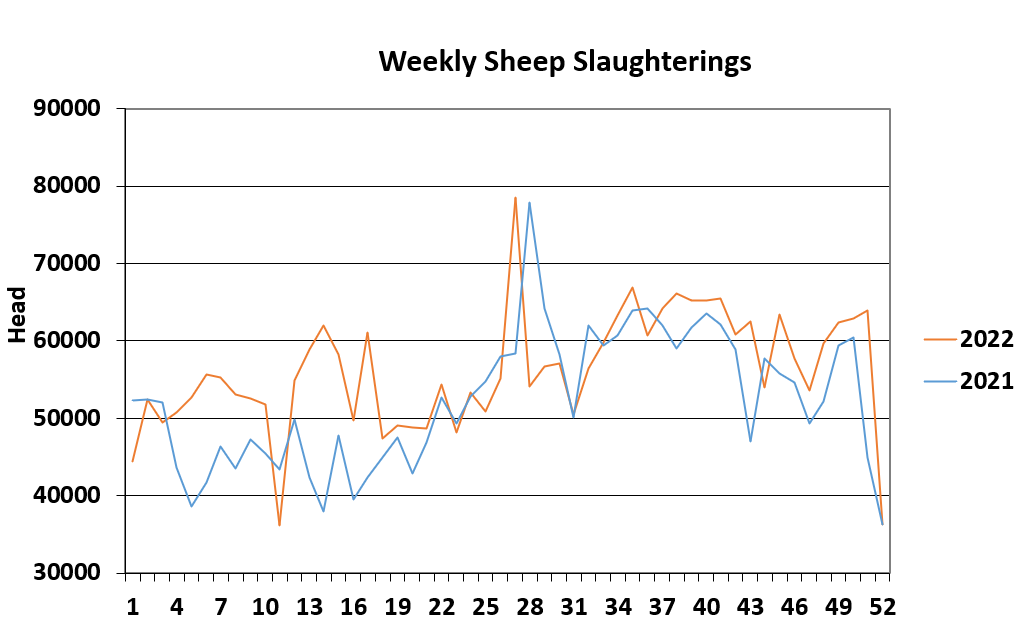

Looking at the final figures for 2022, released by the Department of Agriculture, Food and the Marine (DAFM), 2,992,046 sheep were processed in 2022.

This figure is 201,579 above the total figure of 2021, which was 2,720,467.

Looking at the kill figures in more detail, 915,004 hoggets were processed in 2022, up 216,868 on the 2021 figure of 698,136.

The number of spring lambs processed in meat processing plants came to 1,621,463 head in 2022, which is back nearly 49,000 head on the 2021 figure of 1,670,162 head.

385,428 ewes and rams were processed in 2022, which shows an increase of 33,392 head on 2021 when 352,036 were processed.

The 2022 sheep kill finished over 201,000 head above the final 2021 figure, with an expected high carryover of hoggets in 2023.

So what does the sheep kill figures tell us about the 2022 year? Well, it shows a reduction in spring lamb throughput, which can be attributed to high costs of inputs.

Reviewing the 2022 sheep kill

It was clear to see that fewer concentrates were fed to lambs throughout the year, with average carcass weights down on 2021 weights.

This meant more reliance was put on finishing lambs off grass and for many, they opted to market lambs at the marts rather than push them on expensive concentrate feed to finish for the factory.

This reduced the throughput of lambs in 2022 and more lambs being marketed at marts will lead to a higher carryover of hoggets into 2023.

The cost of the inputs looks to have pushed back many lambing dates on farms too, which may help the trade in the early part of spring when there may not be too many spring lambs around and if a high carryover of hoggets materialises.

This, however, will all be dependent on market conditions, which are "potentially going to be challenging" according to Seamus McMenamin, Bord Bia sheepmeat and livestock sector manager.

Ewes

The number of ewes processed is up on 2021 and this can be put down to two main factors, the first being a good cull ewe price.

An exceptional first six months of the year was seen for all types of cull ewes, with heavier types taking the limelight, pushing prices in excess of €200 at marts while factory prices were seen as high as €4.30/kg.

The latter half of 2022 saw a drop in ewe prices, but still a firm trade remained.

The second factor relates to uncertainty among farmers around the viability of lambing ewes this coming spring. When input costs and farmgate prices were put against each other this year, many farmers moved their on ewes instead in an effort to cut numbers back.