EU short-term outlook: Dairy herd reduction of 1.5%

Rising costs slowed down milk yield growth (1.2%) in the EU in 2021 and led to a stronger than expected dairy herd reduction (-1.5%).

The data is outlined in the spring 2022 edition of the short-term outlook report, published by the European Commission today (Tuesday, April 5).

According to the report, in 2021, the EU milk sector experienced unprecedented developments. The seasonal trend historically observed in the EU raw milk price did not materialise and prices grew throughout the whole year.

Despite the price increase, EU milk deliveries dropped by 0.3%, the first time since 2009.

EU milk deliveries could continue declining at least in the first half of 2022, before recovering slightly at the end of the year. Overall, this could result in flat milk deliveries for the whole year.

The feed affordability could keep the yield growth at a similar rate to last year (+1%), while the EU dairy herd could be further reduced (-1%), according to the report.

Inflation and input costs for dairy

The short-term outlook report indicates that rising inflation and input costs are likely to result in upward pressure on consumer prices also for dairy products.

While EU cheese and butter consumption could still increase slightly, use of milk powders is expected to be reduced with some replacements taking place for cheaper proteins.

Overall, the cheese and whey production stream could continue being the most preferred option while some production recovery is expected for Skimmed Milk Powder (SMP).

Milk

In 2021, the EU milk sector experienced unprecedented developments. The seasonal trend of price decline during the spring flush did not occur, and prices improved in every month of the year, according to the outlook report.

In December, it reached more than €40/100kg (+18% compared to January 2021). The trend continues by February 2022, with no strong signals of a possible short-term relaxation.

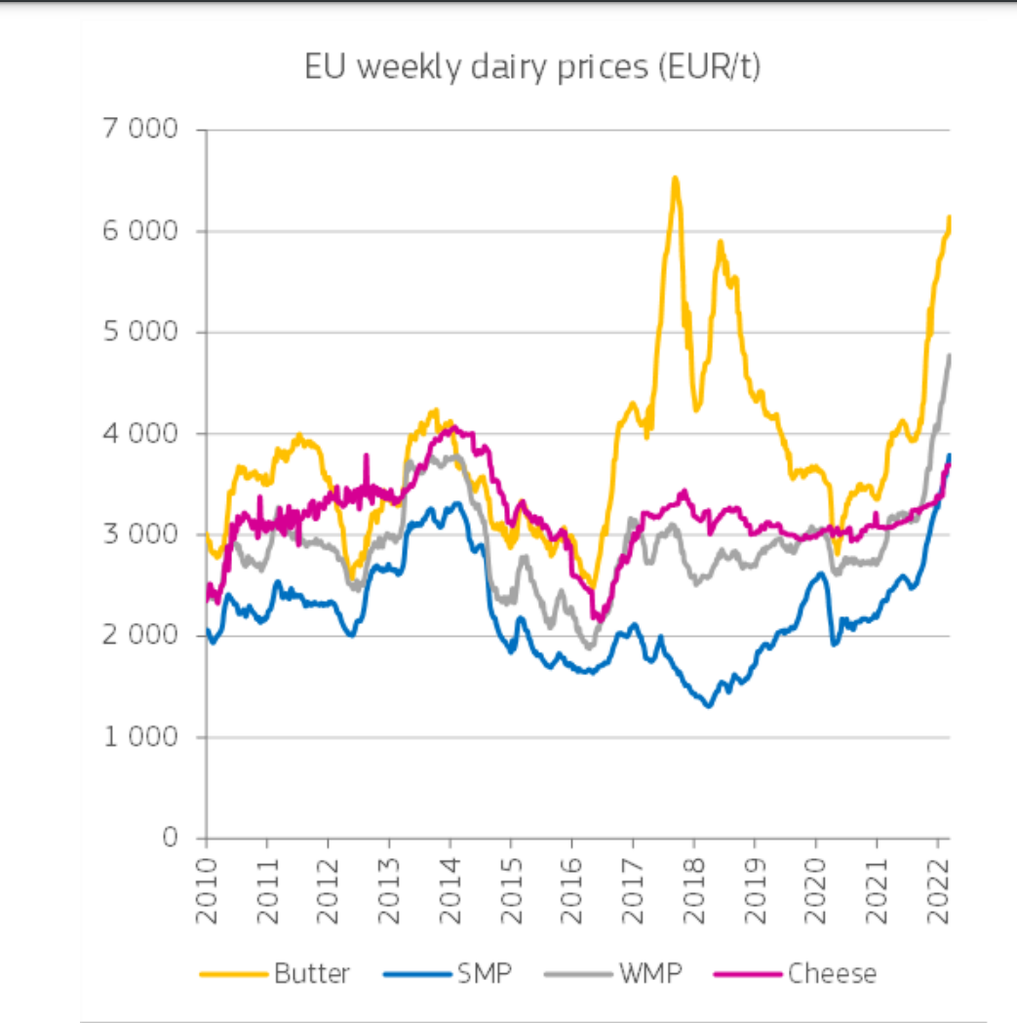

This development was mainly supported by a tight supply coupled with a strong demand in China, especially for milk powders (SMP +27%, WMP +32%), but also cheese and cream, targeted to foodservice and food processing.

In mid-March, EU SMP prices were close to €3,800/t, levels last seen in 2007. At the same time, EU butter prices climbed over €6,000/t.

Combining these two, the EU milk price equivalent is above €50/100kg, supporting the upward trend for farm gate milk prices. Prices of EU cheeses climbed as well. EU cheddar prices are around €3,700/t, the highest since 2014 before the Russian banon EU agri-food imports which hit the cheese market particularly hard.

EU consumer prices for dairy products are increasing as well (+7% for fresh whole milk, +6% yoghurt, +5.3% for cheese and curd in February compared to the same month last year).

Global milk supply

Another factor supporting the upward trend of prices is the tight global milk supply, according to the commission's report.

While US production grew 1.4% in 2021, drought impacted milk production negatively in Oceania during the usual peak of its season.

This hampered production growth in New Zealand (+0.1%) in 2021 and led to a decline in production in Australia (-0.9%). Increasing input and feed prices led to a reduction of the dairy herd in the US.

Together with higher prices of raw materials needed to invest in processing capacities, a slowdown of milk production in the US is expected, at least in the first half of 2022.

As Oceania is entering the months of lower production, the global milk supply should remain tight until a possible recovery in the second half of 2022, according to the report.

Dairy prices should therefore remain high during most of this year. Global dairy demand grew in 2021, linked to the relaxation of Covid-19 lockdown rules and economic activities taking off again.

However, rising energy and commodity prices, as well as inflation, could slow down this recovery. In the case of China, the demand could be reduced due to existing stocks, increasing domestic production and the spread of the omicron variant in Asia.

The report states that as long as the zero-Covid policy is maintained, this could put millions of people into lockdowns, reducing the foodservice demand.