Ciaran Fitzgerald: Why export focus is a boon amid inflation

When talking about inflation, consider first that Ireland exports just over €15 billion worth of agri-food products annually.

For the largest agriculture sectors - meat and dairy - exports account for almost 95% of production.

The harsh reality for Irish agri-business is that international markets, for all their volatility and competitiveness challenges, are much more transparent and price responsive than our domestic Irish grocery market.

Over the years when farmgate prices have come under pressure, part of the public discourse around how this arises has been to compare supermarket/retail prices with producer prices.

There are a number of reasons why this simple relationship between grocery and ex-farm / ex-factory prices is at best, weak, if not non-existent.

Setting food prices

In the first instance, supermarket retail prices reflect what price the supermarket/retailer has set for the product.

Supermarket pricing policy, and in particular a policy of using fresh foods like meats, liquid milk and fresh vegetables as 'loss leaders', priced at, or below cost, has been the principal driving force behind food retail pricing in Ireland, the UK and across the EU.

We also know that this loss-leader approach is intended to attract in customers who then buy a full basket or trolley of goods containing 50 or more items, which the supermarket/retailer will price with a significant margin so that the retailer earns an overall profit.

Inflation 2022

Clearly a key economic and political challenge of 2022 is the capability to cope with the energy-cost-driven surge in inflation / cost-of-living, locally and globally.

For Ireland, as the table below shows, inflation pressures have seen the overall cost of living increase by over 9% at peak, with it still running at over 8% in September, according to the latest set of figures from the Central Statistics Office (CSO).

A deeper analysis of the main cost-of-living categories illustrates how much this surge in the cost of living is driven by energy cost increases which, as we know, are themselves driven by the war in Ukraine.

Energy costs (as per the table below), are up 68% year-on-year, while utilities costs have increased by 70%. Meanwhile, food prices are up by 10%.

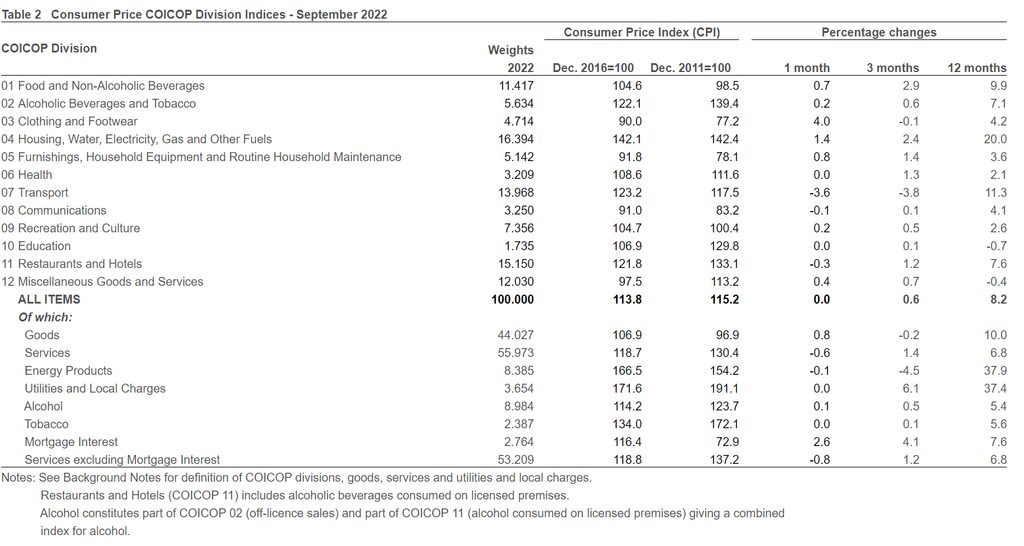

The table below from the CSO takes a deeper and longer-term look; it not only breaks down the current inflation picture by category, but also shows how prices have changed in comparison to both 2016 and 2011.

Food prices have increased by just 4% since 2016 and even with the 10% increase in prices this year, are still running at 1.5% less than food prices in 2011.

The food category here represents grocery food prices only. Food prices in restaurants and takeaway are covered in Division 11 (restaurants and hotels), where prices have gone up 22% since 2016 and 33% since 2011.

Cost of living

In terms of how economies like Ireland's might cope with the surge in the cost of living, there have been a number of areas of focus.

In the short-term, and in particular over the coming winter months, the focus has been on providing supports for the most vulnerable consumers to combat the huge increases in energy costs.

Also in the short- to medium-term there has been a somewhat more difficult 'negotiation' about salaries and pay levels.

This has focussed on trying to ensure that pay demands to cope with higher costs of living do not, of themselves, further fuel cost increases and embed an ongoing spiralling of cost of living, which was very much a feature of the 1970 energy crisis.

Input and output prices

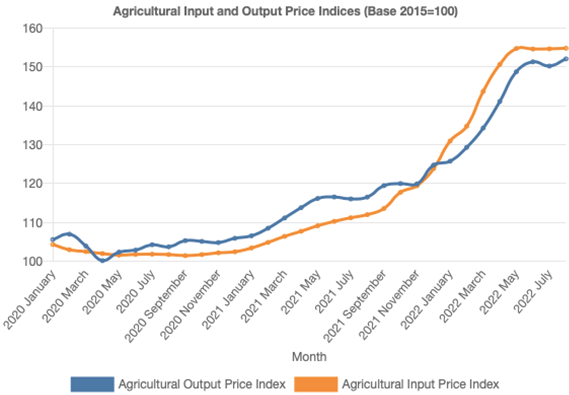

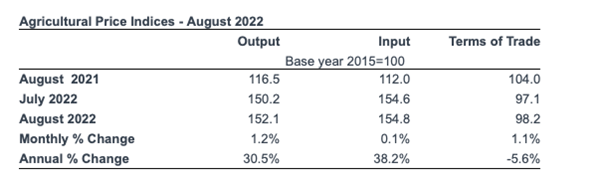

What the CSO general inflation picture does not show, but what is captured in the CSO agricultural input and output figures, is the huge surge in input costs for Irish agriculture.

These costs include fertiliser and feed, while fortunately there has also been a significant increase in output prices as indicated in the chart below.

For Irish agri-business then, while there are issues around the representativeness of food inflation figures as a measure of either on-farm or ex-factory prices for food products, the impact of increasing energy prices is best measured by agricultural price indices as indicated below.

Given the focus on managing the cost-of-living increases, now is probably not the best time to be highlighting the fact that domestic grocery businesses, supermarket and discounter alike, continue to use dominant buying power to use fresh food products as 'loss leaders' to shore up their profit profile.

In contrast, international markets operate much more like the free markets much admired by politicians and competition authorities, where buyers and sellers have much more equivalent status.

We are lucky then that the Irish agri-food sector, despite the challenges of Brexit, Covid-19 and the onslaught from the domestic environmental lobby, continues to demonstrate huge capability to adapt and secure international/global customers.

This enormous capability continues to support over 260,000 jobs across the economy, €15 billion in exports and €15 billion annually in Irish economy spend.