Ciarán Fitzgerald: Focus on food prices is mere populism

The current focus on food prices seems to be more about populism than real concern about long-term trends, while Irish agriculture's move forward on lower carbon output does not seem to be recognised.

There has been a lot of heat but very little light generated in political and media circles around food prices in recent weeks.

Despite all of the noise, over the last three years in particular, around the 'new paradigm' imperative of sustainable food production and carbon budgets, the reality of the stunt that is dominant retailer pricing (masquerading as everyday low pricing), trumps everything still.

The point here is that the continuing ability to get suppliers to fund price falls and the body politic to fall over itself in calling for more, through loss leading by retailers, is still the core issue.

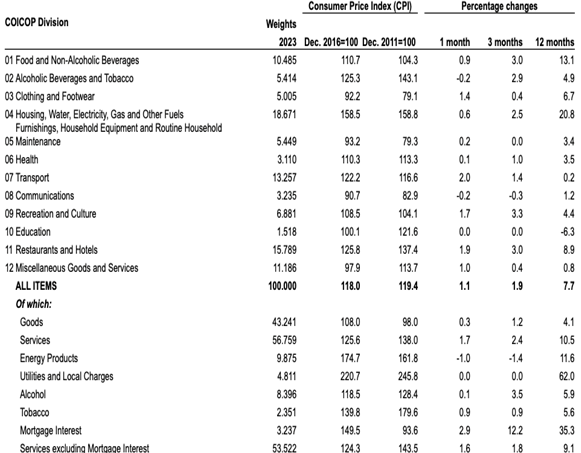

The chart above from the Central Statistics Office (CSO) shows the rate of price inflation across all sectors of the Irish economy on a 12-month basis, compared to base years of 2016 and 2011 capturing both long- and short-term impacts.

- As we all know, or did up until recently, inflation in Ireland and globally has largely been driven by energy price increases;

- As the table above shows, energy prices increased by 21% compared to last March, but reached higher levels;

- Crucially, energy product prices as shown in the bottom half of the table are now running 75% higher than in 2016 and 62% higher than in 2011;

- In contrast to this long-term inflationary impact, while food purchased as groceries increased in price by 13% year-on-year, food prices are only 10% higher than in 2016 and only 4% higher than in 2011;

- Food bought in restaurants or takeaways, while increasing by 8% year-on-year, is 26% higher than in 2016 and 37% higher than in 2011;

- Moreover demand from food outside of home has increased.

So all these calls for the government to do something now about food prices is moot.

Sustainability

The reality over the longer term is that fresh food in grocery retail saw almost no price increase between 2011 and 2021 and only in 2022/2023 has there been some price inflation.

Clearly, governments must be attuned to the availability of affordable food but governments must also be on top of ensuring continuity of sustainable food supply (particularly ones involving Green Parties).

In that sense, even before the onslaught of food 'woke-ism' by our environment friends, the fundamental understanding of the dynamics of food production supply and demand had unfortunately been very much dumbed down over last 20 years.

In essence, the farmer and the food processor were offered up to the food retailer / discounter as part of a Faustian pact that 'promised' everyday low food prices and was totally agnostic about either the economic or environmental sustainability of local food production and supply.

This agnosticism ignored the reality whereby increased production costs and regulatory constraints are completely at odds with everyday low pricing of fresh produce or Known Value Items (KVIs), and inevitably means a long-term fall-off in local supply capability.

This disconnect has meant that local production of fruit and fresh vegetables in particular, has diminished because of the cost price squeeze, to be replaced by imports from lower cost regions.

The Irish meat and dairy sectors only dodged a bullet firstly because the industries have world-class marketing capability.

They dodged another bullet when the DOHA Development Round of the World Trade Organization, which would have given up large segments of the EU beef and dairy markets, collapsed in 2008.

The sectors are also being sustained by increasing global demand for low carbon grass-based meat and dairy.

Nevertheless, the continuing systemic absence of joined-up thinking means a long-term disconnect between aspirations for sustainable food demand and the sustainability of local food production.

Food prices

The current 'circus' around food prices will move on and unfortunately the chance of a deeper dive into the reality of retail food pricing with it.

Meanwhile, the concern following the recent interview by Agriland with the head of Environmental Protection Agency (EPA) is that not only is the old dominant buyer trope still in place, but the current realities of Irish agriculture showing significant changes in introducing emissions-lowering production methods are not recognised.

The 'view' expressed by the EPA seems to be stuck in a 2019 time warp.

It doesn't reflect the adoption of the Marginal Abatement Cost Curve (MACC) emissions-reducing practices, the 20% reduction in fertiliser usage in 2022, the stabilising and reduction in the national herd (CSO data, Dec 2022) and the reality that the expansion phase in dairy has plateaued.

Real progress in adopting emissions-reducing practices in Irish agriculture has been made and more is needed and will follow.

By the way, Irish agriculture is way ahead of most other sectors of the Irish economy where the low carbon journey has not even started.

This real progress is verified on a daily basis by global customers and consumers who want more and more of Ireland's low carbon output.