Finishing cattle early or late - how do price trends compare?

It is primarily the farmers finishing cattle off grass that are bearing the brunt of the beef trade price cuts this year as quotes for all categories of cattle have fallen again this week.

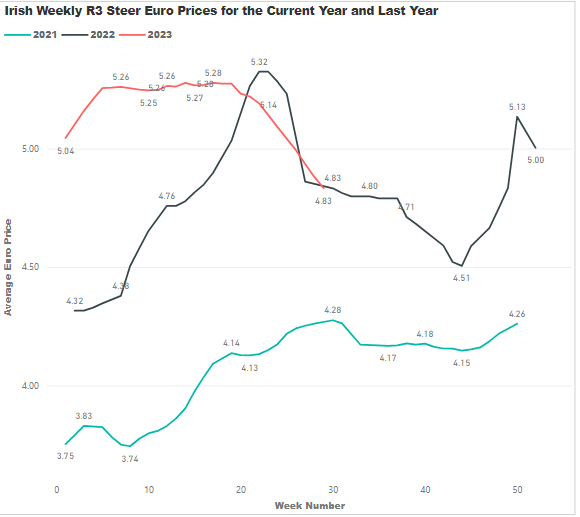

Late January to mid-May of this year saw prices for beef cattle peak (see graph below) which is the time of year when larger volumes of finished cattle are coming from sheds.

Irish beef price has been on a declining trend since mid-May, which is when larger shares of finished cattle begin to come direct off grass, in line with the Irish grazing season.

Finished cattle coming direct off grass continue to account for the majority of the beef kill until the end of the grazing season in the final quarter of the year.

Finishing cattle direct of grass is seen as a lower-cost system than winter-finishing cattle in the shed, but different beef farmers prefer the different systems for various reasons and many beef finishers finish cattle all year round to spread their risk.

Both this year and last year, the higher beef prices were paid for cattle finished in the first half of the year but in 2021, the trade was more favourable for farmers finishing cattle of grass in the second half of the year.

The graph below shows the weekly average R3 steer prices for 2021 (blue), 2022 (navy) and 2023 (red) - to date:

A weak trade in the back-end of the year is a negative for farmers finishing cattle off grass, but it can be suitable for winter beef finishers who are filling sheds of store cattle for a winter finish.

Ironically, a strong cattle trade in the spring results in grass buyers having to pay more for store cattle that will be finished in the back-end of the year.

Price movement in the cattle trade can be either positive or negative, depending on if a farmer is buying cattle or selling cattle and the direction of the price movement.

It remains to be seen how the beef trade will go in the final five months of this year and when the current declining price trend will level out and begin to increase again.

While the grass-finish system in the second half of the year is seen as the lower-cost option, steer prices are back approximately 55c/kg from peak earlier this year and farmers who bought store cattle this spring were buying cattle in a very strong trade.

Winter finishing is a higher-risk option due to higher costs but where farmers can manage these costs and when store cattle prices are back in the autumn and the trade comes favourable in the spring, it can be a lucrative option.