Beef trade: Cows come under price pressure

After holding relatively steady for an extended period, cow prices have come under pressure this week and most buyers have opted to drop quotes.

Where P-grade cows were trading up to 350c/kg last week, quoted prices have edged downwards to 330-340c/kg this week. A similar story is also evident for O-grade animals and buyers are starting negotiations with farmers at 340-350c/kg for these lots.

However, R and U-grade cow quotes remain largely unchanged from last week and buyers are offering 365-370c/kg and 375c/kg respectively to secure these lots.

Despite the dip in cow trading, the prime beef market remains relatively unchanged from last week. Factory buyers are currently offering 415-420c/kg for steers; however deals are being done at higher prices and some buyers are paying 5-10c/kg above base.

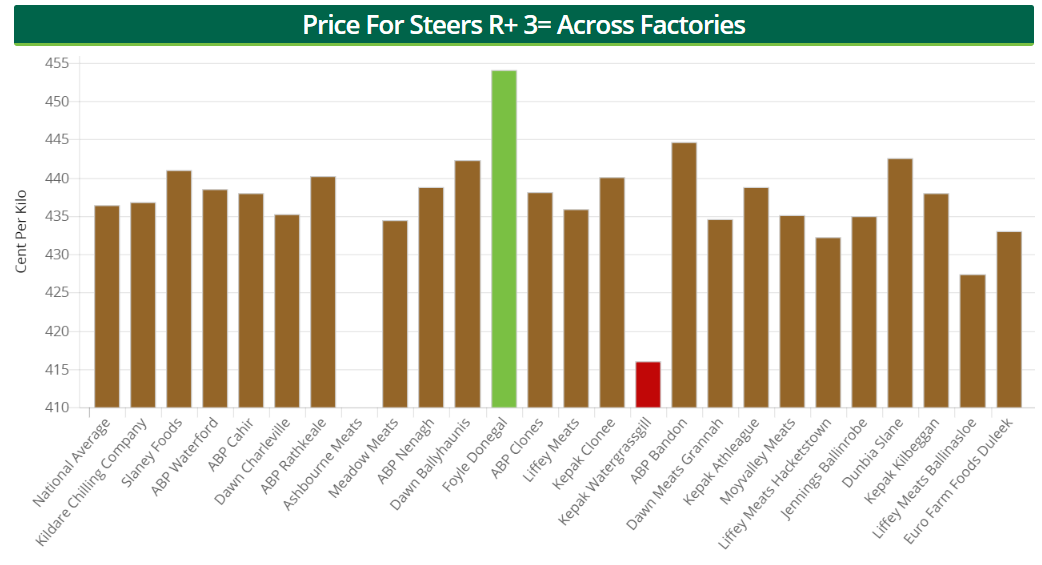

During the week ending June 6, in-spec, R+3= steers made a top price of 454.06/kg, while the average price paid stood at 436.46c/kg.

Meanwhile, factory buyers are currently quoting 420-430c/kg for heifers this week and, like previous weeks, deals are being done at 5-10c/kg above base.

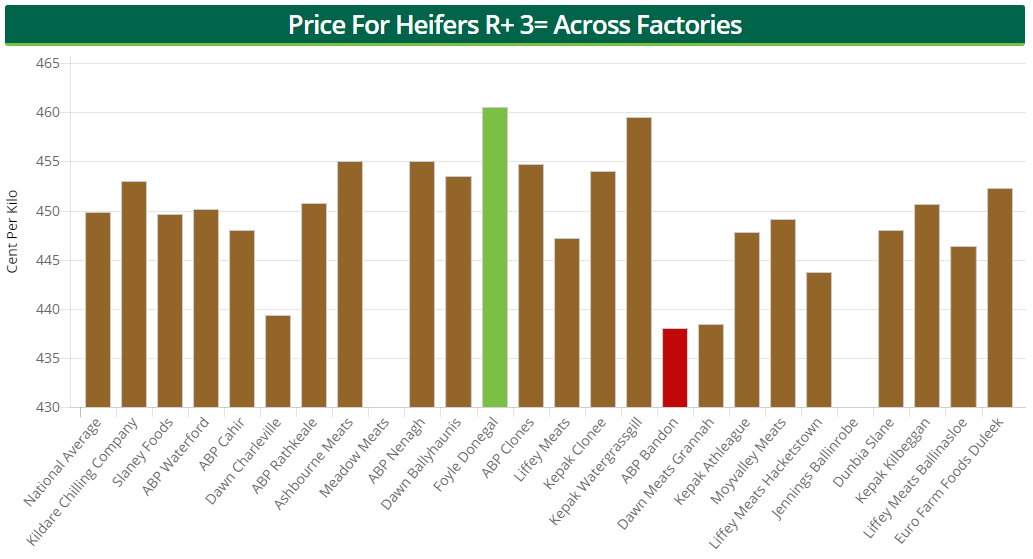

Looking at heifer returns during the week ending June 6, a top price of 460.49c/kg was achieved, while the average stood closer to 449.85c/kg.

Supplies

Some 31,986 cattle were processed in Department of Agriculture approved beef export plants during the week ending June 3. When compared to the week previous, the total weekly kill climbed by 157 head or 0.5%.

Throughput increases were witnessed in the young bull, bull, cow and heifer categories. However, steer throughput declined by 272 head or 2.4% on levels from a week earlier.

When it comes to the cumulative beef kill, some 724,198 cattle were slaughtered in Department of Agriculture approved beef export plants up to the week ending June 3 – a rise of 20,409 head or 2.9% on the corresponding period in 2017.

Notable increases were witnessed in the young bull and heifer categories – up by 3,050 head and 9,294 head respectively – while steer, aged bull and cow numbers also increased.