Beef trade: Bulls come under increased pressure in processing plants

Farmers with bulls fit for slaughter have come under pressure in beef processing plants, with some finishers finding it somewhat difficult to market their animals.

This has become a major concern for bull finishers – especially those with bulls at risk of becoming overage. And, to add to this concern, some plants have re-introduced weight restrictions on these animals.

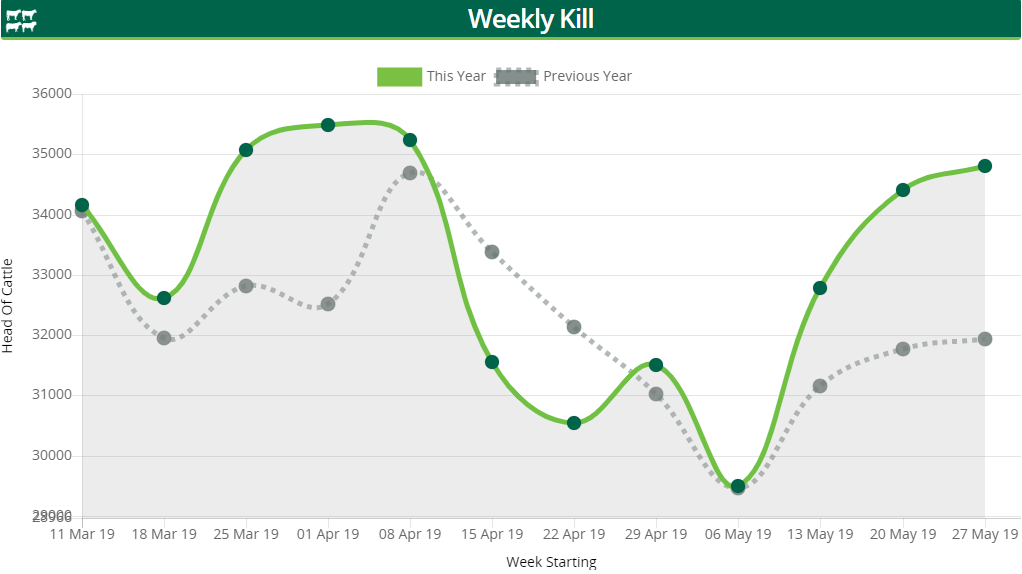

During the week ending June 2, the number of young bulls presented for slaughter increased by 530 head, while the number of aged bulls stood at 958 head.

Prices are very much dependent on location and demand of the individual processing plant, but under-16 month bulls have taken hit at the factory gate.

U-grading bulls are making in the region of €3.80/kg, while R-grades are being quoted at 10-15c/kg lower at €3.65-3.70/kg.

O-grading bulls are hovering around the €3.40-3.55/kg mark. There may be an additional 5c/kg more on the table, but this depends on a farmer’s individual negotiating power.

Moving to the prime cattle trade, some processors have moved to lower base quotes. Steers are now making 385-390c/kg and their female counterparts are securing 395-400c/kg. These higher quotes are again being secured by farmers with the most negotiating power.

The number of steers slaughtered during the week ending June 2 stood at 10,125 head – a 613 head drop on the previous week’s kill.

The heifer kill also fell during the same week; the number of these animals killed amounted to 9,398 head – a decrease of 657 head.

Finally, looking at the cow trade and kill, these animals have also felt some downward pressure, with P-grades hovering around the 290-300c/kg mark, with O-grades back to 310c/kg. Moreover, R-grading cows are securing up to 330c/kg.

For the same week, the number of cows bought by beef factories increased by 1,175 head – up from 8,207 during the previous week.

Other EU markets

Looking at prices elsewhere in Europe, according to Bord Bia, R3 steers were quoted in Great Britain for the week ending June 2 at £3.5/kg or €4.01/kg; this is a reduction of approximately £0.03/kg for the second consecutive week.

Moving to France, there was no change in the price quoted that week for young bulls, leaving the price at €3.76/kg, while O3 cow prices were €0.08/kg up on the previous week at €3.33/kg.

In Italy, Bord Bia says, young bull prices fell by €0.25/kg to €3.53/kg, while the German young bull price fell to €3.46/kg – a fall of €0.05c/kg.