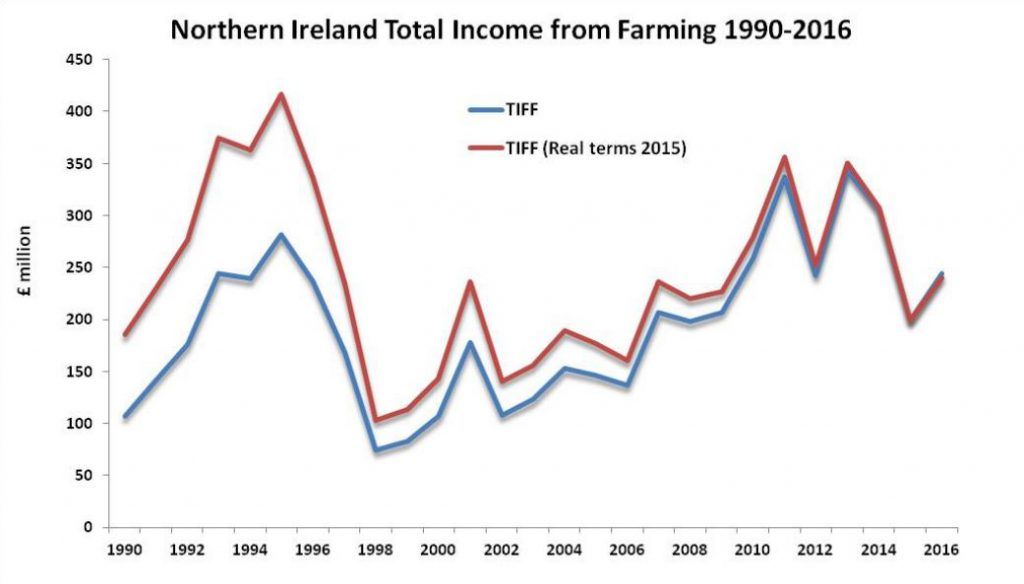

Farm incomes increased by over 20% in the North in 2016

Provisional figures indicate that the ‘Total Income from Farming’ (TIFF) in the North rose by 22% in 2016 (21% in real terms) to £244m (€283m) from £199m (€231m) in 2015.

The first provisional estimates for farm incomes in 2016 were released by the Department of Agriculture, Environment and Rural Affairs (DAERA), while revisions have been made to previous years.

TIFF represents the return on own labour, management input and own capital invested for all those with an entrepreneurial involvement in farming. It represents farm income measured at the sector level.

There was a 1% increase in the value of output from the livestock sector, which was offset by a combination of a 13% fall in horticulture plus a 2% reduction in field crops.

Farm Income Levels in the North

Farm Business Income measured across all farm types is expected to increase from an average £14,788 (€17,178) in 2015/16 to £18,943 (€22,005) in 2016/17.

This represents an increase of £4,155 (€4,826) or 28% per farm, the figures show.

The upturn in their incomes is mainly attributed to higher subsidy receipts combined with more favourable lamb and pig prices in the 2016/17 accounting year.

Dairy

Dairying remained the largest contributor to the total value of Gross Output, despite falling a further 6% to £452m (€525m) in 2016.

The annual average farm-gate milk price and the volume of raw milk produced in Northern Ireland both fell by 3% in 2016 to 20.2p/L (23c/L) and 2.2 billion litres respectively, DAERA figures show.

Cattle

Provisional figures indicated that the output value of cattle in the North was 6% higher at £425m (€493.7m) in 2016.

The average producer price for finished clean cattle north of the border was £3.19/kg (€3.71/kg) in 2016 while the average producer price for cull animals was £2.16/kg (€2.51/kg).

Sheep

The value of output from sheep increased by 15% to £73m (€84.8m) in 2016.

This increase was a combination of a 14% increase in the producer price to £3.91/kg (€4.54/kg) and a 2% increase in the number of lambs and hoggets slaughtered.

Meanwhile, the total volume of sheep-meat produced was marginally lower compared to 2015, according to DAERA, because of a reduction in the average carcase weight to 22kg.

Pig/Poultry

With regards to the intensive livestock sectors the pig sector improved by 6% to £122m (€141.7m) and the egg sector grew by a further 9% to £97m (€112.7m), but the value of poultry output reduced by 1% to £246m (€285.8m).

The producer prices in the poultry and pig sectors fell by 4% and 1% respectively, whereas the producer price for eggs remained unchanged.

Arable

The total output value for field crops in the North decreased by 2% in 2016 to £57m (€66.4m)

According to DAERA, this was as a result of reductions in the volume produced for barley and other crops because of the adverse impacts of weather on yields.

The value of output of potatoes in 2016 rose by 17% to £20m (€23.3m), which was attributed to changes in the volume of stock carried forward and an increase in the producer price which was partly offset by a reduction in the volume of potatoes produced.

Provisional figures show that the value of output for wheat decreased by 5% to £8m (€9.3m) and the output value of barley fell by 9% to £17m (€19.8m).

Horticulture

The value of output recorded in the Horticulture sector was also down year-on-year for 2016, by 13%, at £104m (€121.1m), estimates show.

The mushroom sector is the largest of these sectors by value, with an output of £53m (€61.7m).

Payments

In 2016, the estimated value of the direct subsidies (Basic, Greening and Young Farmer payments) was £276m (€321.3m), representing an increase of 18%, when compared with the 2015 payments.

DAERA attributed this to the more favourable exchange rate between Sterling and the euro.

Input Costs

The total value of Gross Inputs decreased by 2% in 2016, to £1.35 billion (€1.57 billion), figure show.

Feedstuff costs, which accounted for 53% of the total Gross Input estimate, reduced by 2% to £716m (€833.6m) in 2016.

Meanwhile, the total cost of fertilisers in 2016 fell by 7% as a result of a 16% reduction in the average price paid per tonne which was partly offset by an 11% increase in the volume purchased, according to DAERA.

There was also a reduction in total lime purchases, with the result that total expenditure on fertilisers and lime fell to £69m (€80.3m).

Total machinery expenses decreased by 7% to £129m (€150.2) in 2016, as a result of an 11% reduction in the cost of fuel and oils, provisional estimates show.