Factories hold firm on quotes, but deals being done at higher prices

There has been little movement in the prices factories are offering for steers and heifers, as many have opted to maintain quotes at last week’s levels.

For the most part, factories are offering 390-395c/kg for steers and 400-405c/kg for heifers. These quotes exclude Quality Assurance Bonus payments.

However, some finishers have noted that buyers are willing to pay 5-10c/kg on top of the base to secure supplies.

Deals are also being done on transport and clipping charges to encourage farmers to offload supplies in the coming days.

But, procurement managers have indicated that cattle supplies remain relatively strong on the ground and, as a result, they have resisted the temptation to increase the base price this week.

Despite the lack of movement in the steer and heifer market, there has been some uplift in cow prices with quotes up by 5c/kg on last week.

P-grade cow prices are currently sitting at about 320c/kg. O-grade cows are making 330c/kg. Buyers are beginning negotiations with farmers at 340-350c/kg for R-grade animals.

Beef prices

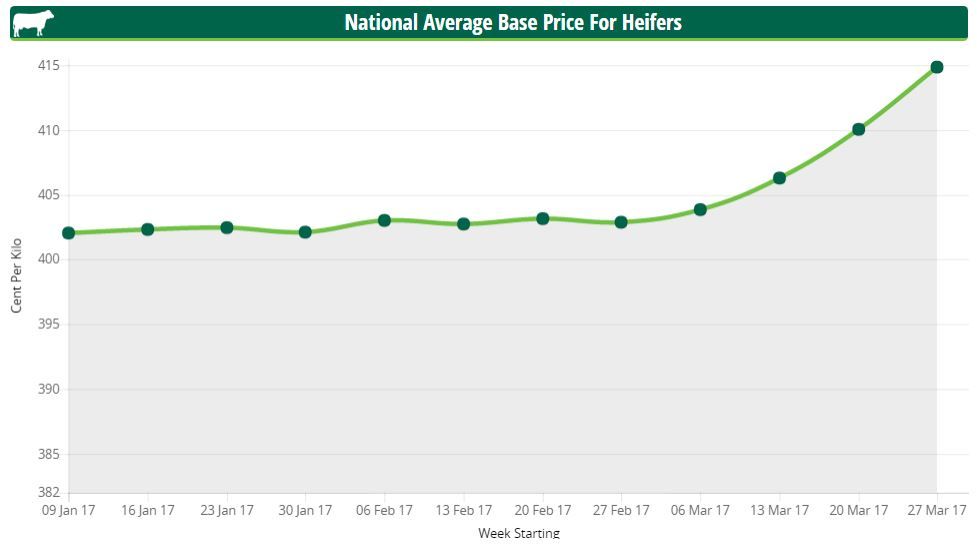

When breed-specific and other bonuses are included, farmers were paid an average price of 415c/kg for base heifers during the week ending April 2.

This was an increase of 4.76c/kg on the week before.

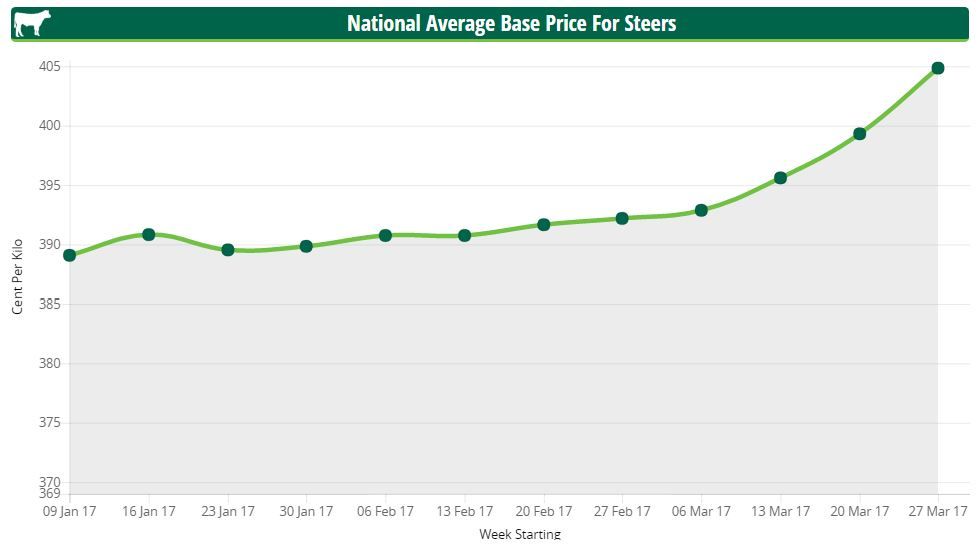

Steer prices also improved during the week ending April 2 and were up by 5.55c/kg to 405c/kg.

Cattle supplies return to normal levels

Cattle supplies have slowly started to return to normal levels, with 30,330 head slaughtered during the week ending April 2, figures from the Department of Agriculture show.

Earlier this year, weekly beef kills stood at about 35,000 each week. This applied downward pressure on prices in some locations.

IFA National Livestock Chairman Angus Woods said agents and factories are finding it very difficult to get adequate supplies to meet strong demand.

“Feeders need to dig in hard and demand more at this time,” he added.

Looking at the beef kill in more detail, some 3,089 young bulls were slaughtered in Department of Agriculture approved beef plants during the week ending April 2. This was back by 206 head or 6.3% on the week before.

Heifer and steer throughput has also declined on a week-to-week basis, with supplies down by 384 head and 809 head respectively during the week ending April 2 – compared to the week before.

However, cow and aged bull supplies have increased from the previous week’s levels, with throughput up by 2.7% and 0.8% respectively.

Cattle supplies up overall in 2017

Figures from the Department of Agriculture also show that an additional 10,697 cattle (+2.6%) have been slaughtered in Irish plants this year.

An increase in cow, heifer and steer slaughterings make up the majority of this increase, but young bull and aged bull slaughterings are back by 11% and 15% respectively on 2016 levels.

Additional cattle supplies are likely to remain a key feature of 2017; an extra 100,000 head are expected to come on stream before the year ends. This is due to climbing calf births in 2015 and reduced exporter activity.

Main markets

According to Bord Bia, there has been a slight uplift in UK beef prices on the back of an ease in supplies.

Cattle prices from the AHDB remain stable in Sterling terms, with British R4L steers averaging 358p/kg or 418.81c/kg during the week ending April 1.

In addition, British R3 heifers made the equivalent of 411c/kg while Northern Irish R3 heifers made 406c/kg.

Bord Bia also reports that the French beef market has seen some uplift due to stronger seasonal demand ahead of Easter, with many retail promotions focusing on steaks, fillets, offals, loins, ribs and mince. These promotions, it says, were focused both on domestically-produced and imported beef. A small improvement was also seen in the Italian market as a result of higher demand.