Ciaran Fitzgerald: Why does inflation not apply to food?

Inflation is every where, but not in food or agriculture because the sector does not have selling power.

There is ongoing debate as to whether the biggest barrier to post-Covid-19 economic recovery is the new variant or variants, that effectively mean an ever elongating pandemic.

Or from some quarters, the threat of significant price inflation caused by a combination of delayed or truncated consumer spending and supply chain impacts of Covid-19 lockdowns.

It is interesting to read recent analyses and reviews of the Irish economy performance and forecast into 2022, not least in the context of the price inflation issue.

Inflation in sectors

One sector of the Irish economy that has been given huge plaudits is the pharmaceutical sector, which has definitely thrived under the challenges of developing the Covid-19 vaccine and the general increase in demand in the health care sector.

Without wishing to rain on anybody’s parade, I would suggest that while growth in Irish pharma is great in terms of traditional (but hugely overstated) Ireland gross domestic product (GDP) impacts, it is the sector's spending in Ireland, on people, raw materials and services, that truly defines its actual impact on the Irish economy.

As the figures from the Department of Enterprise, Trade and Employment's 'Annual Survey of Irish Economy Expenditure' show, expenditure by the pharma sector in the Irish economy is running at just over €3.5 billion euro/annum, or just 20% of the expenditure figure of over €16 billion annually by the agri-food and drink sector.

To labour the point here yet again - for every euro turnover in the pharma sector, the Irish economy gets 10cent.

Whereas for the agri sector, a euro turnover is matched by a euro spend in the Irish economy.

Inflation

A key 'strength' of the pharma sector is its mandated and protected pricing arrangements, so yes, while investment in new drugs and vaccines is hugely expensive, there is a mandated cost recovery mechanism by and large.

Unlike in the food and grocery sector where resale price maintenance is illegal, pharma companies can set the price of their products.

Good for them, and looking across the economy its hard not to conclude that the agri sector is about the only major business that doesn’t have selling power.

Energy providers and smartphone / I.T companies provide other examples of consumer markets where prices are not only set by producers, but there is no below-cost selling and, there are no own label copycat products.

In contrast to the economic reality of business sectors where price/cost recovery is supported through a combination of monopoly power or government mandated pricing, inflation, or even basic cost recovery, is not really happening in food pricing in any meaningful way.

As the tables and charts from the Central Statistics Office (CSO) below show, in effect, cost recovery in the agri food and drink sector hasn’t been a factor for the last six or seven years.

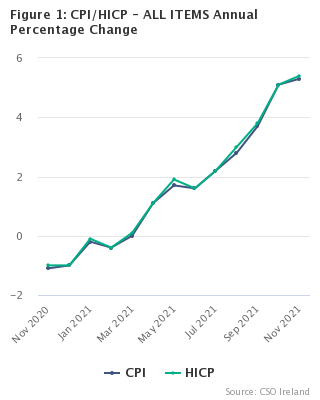

November 2021 CSO :

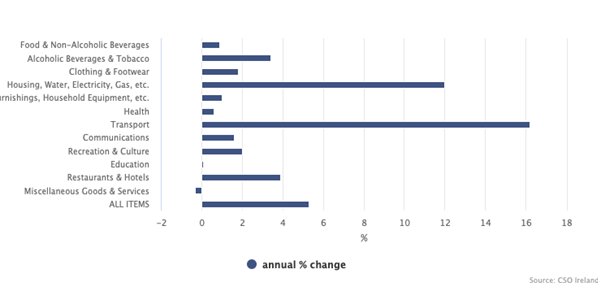

As per the latest November CSO figures, while prices in general year-on-year have increased by 5.3%, prices of food and non-alcoholic beverages have increased by only 0.6%.

The CSO analysis further states that “prices on average, as measured by the CPI, were 5.3% higher in November compared with November 2020. This is the largest annual change in prices since June 2001 (+5.3%)".

Food pricing

In contrast to the very significant yearly increases in the economy as a whole, the table below shows that food prices in 2021 have increased by only 0.6% year-on-year and are effectively running at only 95% of the 2016 level i.e., there has been 4.6 % fall in food prices since 2016.

There is something fundamentally wrong here.

While the EU Commission, and even national governments, may take consolation from the fact that food prices are 'under control', this mismatch between a high cost, highly regulated food production system across the EU, and never-ending lower and lower prices, cannot continue.

It is chronically unsustainable. Dominant buying power is driving this constant cost squeeze, whether by multinational grocery discounters or large-scale dominant supermarkets.

Across the EU, as in Ireland, three to five companies account for 80% of the grocery market.

Effectively no food supplier can sustain a viable business if they are not selling product to one or more of the dominant suppliers in any market segment and this monopoly dominant buying power is hiding in plain sight.

Monopoly

The twin drivers of this destruction in food value are loss leading and own label substitution.

The constant onslaught of TV ads eulogising every day low prices and weekly reductions in grocery bills, is very explicitly demonstrating how, in a multibuy scenario which is unique to grocery shopping, fresh food categories like liquid milk, cheese and meats, fruit and vegetables, are being priced at low or no margin to the supplier.

This is to encourage retail footfall, which ensures that the retailer/discounter recovers margin on non value items. With the food supplier stuck in a chronic below cost pricing spiral.

Part of the new, much talked about, reality for farming and food production in 2022 must involve the construction of a 21st century sustainable food pricing model.