Post-Brexit subsidy changes will have a much bigger effect on farm viability than any other factor, according to one of the UK’s leading arable experts.

Martin Grantley-Smith, Agriculture and Horticulture Development Board (AHDB) strategy director cereals and oilseeds, addressed a full house at the Northern Ireland arable conference yesterday (Thursday, January 11).

Almost 200 farmers attended the event run by the Ulster Farmers’ Union, Ulster Arable Society and CAFRE.

Grantley-Smith said: “Subsidies will have the biggest effect on farm profitability – more than any changes to trade agreements.

- Scenario one – ‘evolution’ – where the UK leaves the Single Market but where the current free trade agreement continues;

- Scenario two – ‘fitter farming or unilateral liberalisation’ – tariffs on imports are set at zero and support is cut by 50%;

- And a third scenario – which we are calling ‘Fortress UK’ – where there’s no trade deal with the EU and WTO (World Trade Organisation) applies and support is cut by 75%.

Brexit modelling

Grantley-Smith used figures representing the average UK arable farm to show projections on how each scenario would affect the farm’s input costs and turnover.

He said: “This comes with a health warning – and that is that I have no more information about what will be in place post-Brexit than you.

“When it comes to what information we have we have to read between the lines.”

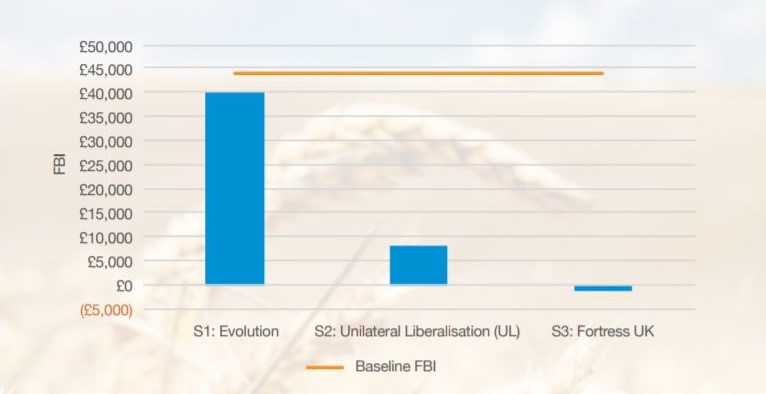

Source: AHDB

Under the most extreme option – ‘Fortress UK’ – the model farm made a loss. Extra expenditure was caused by a slash in subsidies and increased labour costs.

“We do now know from what ministers have said, that at some point, the current subsidy will move into an environmental subsidy. So there are certain things you can do now to put yourself in a better position to handle that,” he said.

Does size matter?

Grantley-Smith added: “You might say, ‘”Yes, but this isn’t my farm,” but what we find is that regardless of size the effects are the same.

“In this particular case, size doesn’t matter but performance does. If you’re in the top 25% of producers then you’re in a very good place to cope with these changes. In all of these models the people who are in the top 25% remain in profit.

“The top 25% of performers remain profitable in all three scenarios. What you have to do is get yourself in that position where you are in the top 25% or as close to it as possible – the closer you are the better you will handle any of these scenarios.”

The bottom line

The baseline Farm Business Income (FBI) for cereal farms is £43,796. Under scenario one – Evolution – this falls by 9% to £39,788.

Under scenario two – Unilateral Liberalisation – FBI falls by 81% to £8,216; while under scenario three – Fortress UK – FBI becomes negative after falling by 103%, making an annual loss of £1,341.

Why?

The 9% decrease seen under scenario one is driven mainly by decreases in value for oilseed rape and barley, caused by the loss of export potential, which is not compensated for by the smaller increase in the value of wheat output.

AHDB research highlights that this scenario is likely to slightly increase existing trends for consolidation in the sector, adding that there could also be a shift away from barley and oilseed rape towards wheat, potatoes and sugar beet, where this is agronomically possible.

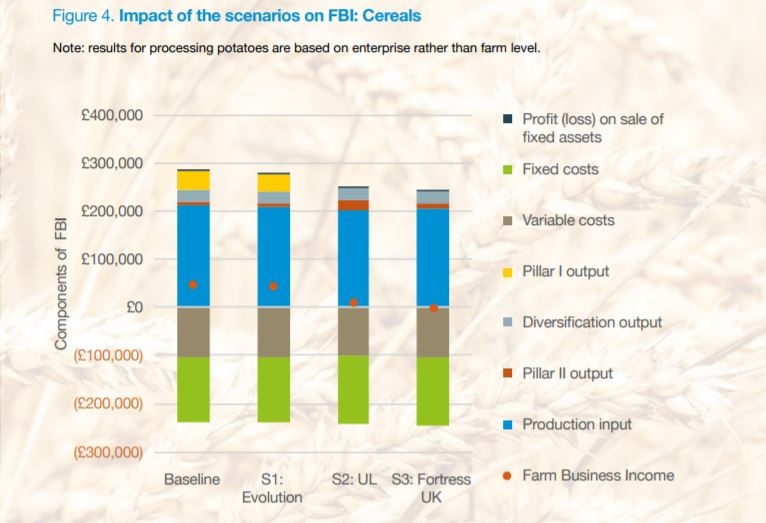

Source: AHDB

Under scenario two, the fall in income is driven mainly by the removal of Pillar I payments (£37,439 per business), which is only partially offset by the increase in Pillar II payments.

Decreases in the value of outputs and increases in regular labour costs also have an impact, although, reductions in regulatory costs provide some marginal relief for these changes.

Under scenario three, there is a smaller increase in Pillar II support, which provides less offset for the loss of Pillar I support and an increase in both casual and regular labour costs. The value of production output also decreases relative to the baseline.

There is likely to be severe pressure on less-efficient farmers and downward pressure on farm size, in order to reduce costs of paid labour.