Beef trade: Steers and heifers now trading at 360c/kg

For the most part, the majority of beef factories are now quoting 360c/kg for both steers and heifers; however, there are some farmers securing prices at 365c/kg – especially for in-spec heifers and bullocks where larger numbers are available.

Agents located around the country have noted an increase in the number of cattle available for slaughter and this has added slight downward price pressure to the trade for prime cattle, with some plants purchasing prime cattle at 355c/kg.

While some parts of the country have indeed received some rainfall over the weekend, other areas are still facing into drought-like conditions, with some farmers opting to move stock. But, saying that, others are in a better position grass wise and continue on as normal.

The determining factor here is geographical location.

Factory buyers are currently starting negotiations with farmers at 270-280c/kg for P-grade cows, 280-290c/kg for O-grade animals and 310c/kg or slightly more for R-grade lots.

Also, there is little change to the bull trade, with continued variation across plants.

Bull base quotes amount to 350c/kg for R-grades in the main, with O-grades hovering around the 340c/kg mark; U-grading bulls are making approximately 360c/kg in the meat plants.

The kill

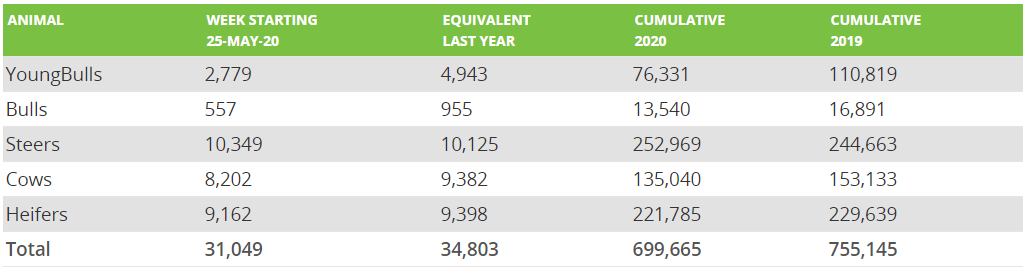

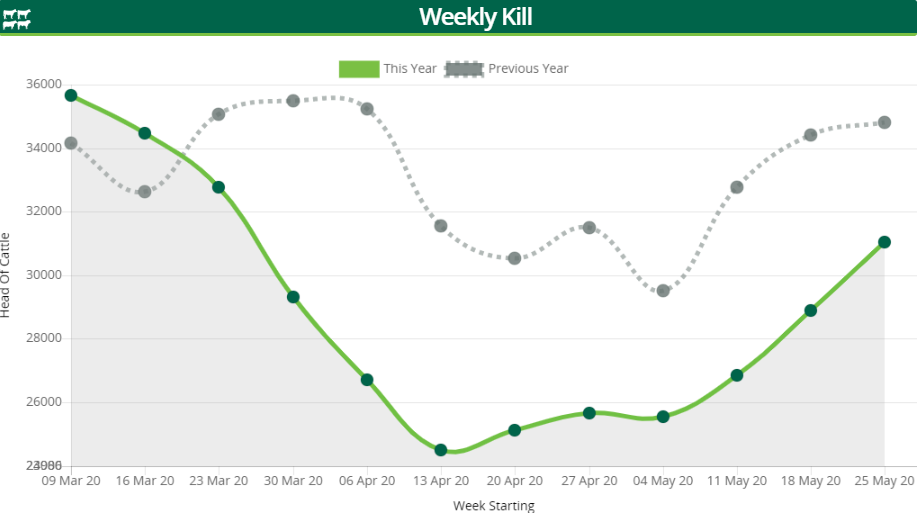

Figures from the Department of Agriculture’s beef kill database show that some 31,049 cattle were slaughtered during the week before last, with cows witnessing a large jump in numbers.

That week, steer and heifer slaughterings stood at 10,349 and 9,162 head respectively. Cow slaughterings accounted for 8,202 head, while young bull and aged bull throughput stood at 2,779 head and 557 head respectively.

Yearly supplies are sitting at 699,665 head – a decrease from the 755,145 head that were slaughtered by this time in 2019.