Beef kill: Factory throughput surpasses 1 million cattle

Over one million cattle (excluding veal) have been processed to date this year at Department of Agriculture, Food and the Marine (DAFM)-approved factories.

DAFM figures up to and including the week ending August 7, show that a total of 1,034,732 head of cattle (excluding veal) have been processed.

The number of cattle processed to date this year is running 83,602 head of cattle ahead of the same time period last year.

The table below shows the number of adult cattle processed both last week and to date this year:

| Animal | Week Starting August 1, 2022 | Equivalent Last Year | Cumulative 2022 | Cumulative 2021 | Cumulative increase |

|---|---|---|---|---|---|

| Young bulls: | 1,639 | 1,390 | 89,763 | 85,120 | +4,643 |

| Bulls: | 629 | 619 | 17,366 | 16,147 | +1,219 |

| Steers: | 15,296 | 15,314 | 387,933 | 362,708 | +25,225 |

| Cows: | 6,123 | 5,878 | 242,700 | 207,698 | +35,002 |

| Heifers: | 8,321 | 7,771 | 296,970 | 279,457 | +17,513 |

| Total: | 32,008 | 30,972 | 1,034,732 | 951,130 | +83,602 |

Looking at the cumulative beef kill figures for this year, we see an increase in the number of cattle processed in all categories.

The largest increase has been seen in the cow category with 35,000 extra cows processed to date this year compared to last year. DAFM data would indicate that the majority of these additional cows are coming from the dairy herd.

Interestingly, the number of young bulls finished this year has increased slightly, which is contrary to the trend of bull-beef systems declining which has been seen over the past number of years.

Steer and heifer throughput have both increased considerably to date this year with the number of steers processed up 25,225 head and the number of heifers processed up 17,513 head.

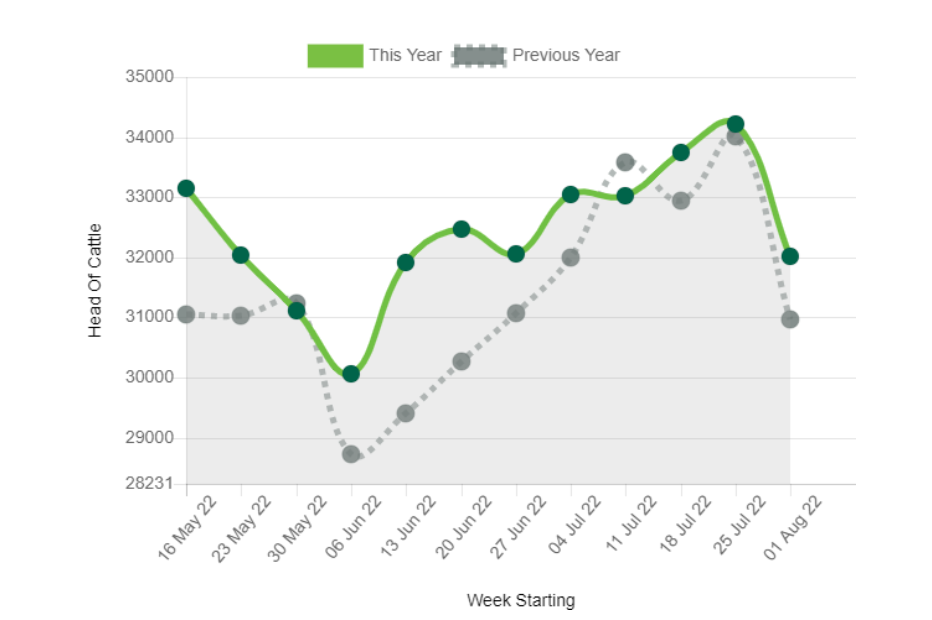

The chart below represents the weekly kill of heifers, steers, cows, bulls and young bulls at DAFM factories:

Last week's cattle throughput witnessed a drop in numbers as a result of the August bank holiday weekend and resulting four-day kill at most processing facilities.

Bord Bia has revised their estimations on the total factory throughput of cattle this year predicting somewhere in the region of 110,000-120,000 additional cattle to be processed.

A higher cow kill and lower exports to Northern Ireland are contributing factors to the increase in the supply outlook.