Beef kill: Concerns regarding medium-term cattle supply

While latest beef kill figures show factory cattle supplies are remaining relatively steady at present, concerns are mounting regarding supplies for the coming four-five months.

Autumn 2024 has been a most unusual time for the Irish beef trade, in that prices have increased into the back end of the year, contrary to the more common trend of prices easing into the final quarter of the year.

The settled weather conditions into October and November reduced pressure on farmers, with finished grass cattle to sell and the strong market demand helped to sustain the trend of rising beef prices being paid to farmers on a weekly basis.

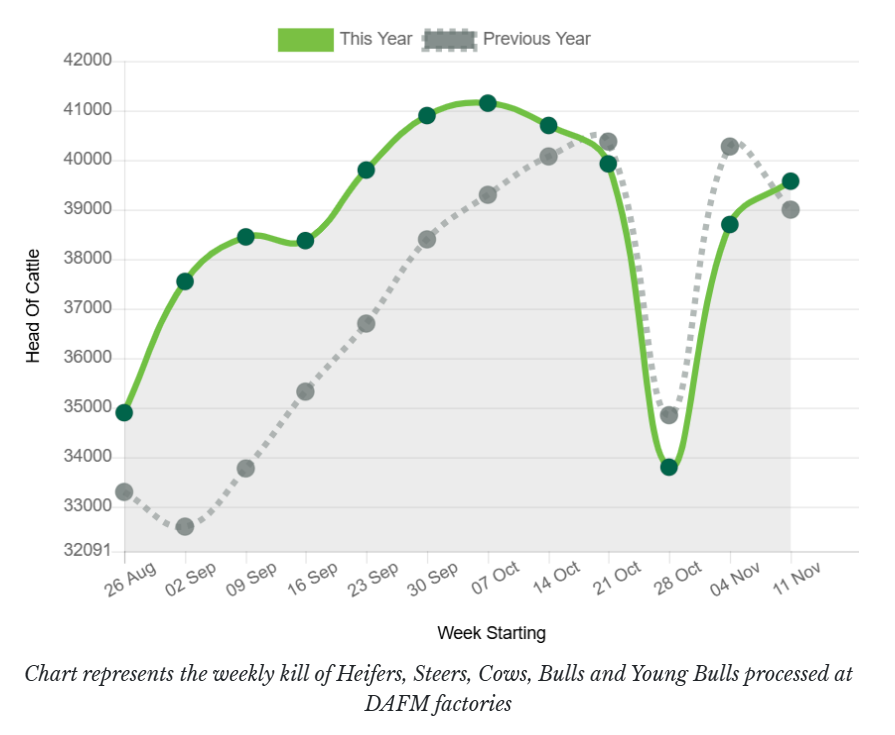

The graph below illustrates the overall weekly beef kill in the past 12 weeks of this year versus last year:

Most procurement staff admitted that there was no 'backlog' of finished cattle in the system this autumn, contrary to previous years where kill sheets may have been as good as filled up to three weeks in advance in late October and early November.

Procurement staff are now sourcing cattle that would have originally been intended for a few weeks later in the year.

The table below details the beef kill composition for the week ending Sunday, November 17, versus the same week of last year and the cumulative beef kill this year versus last year:

| Type | Week ending Sun, Nov 17 | Equivalent Last Year | Cumulative 2024 | Cumulative 2023 |

|---|---|---|---|---|

| Young Bulls | 2,070 | 2,134 | 93,553 | 102,378 |

| Bulls | 449 | 517 | 25,897 | 25,317 |

| Steers | 14,594 | 13,838 | 613,068 | 624,273 |

| Cows | 10,078 | 11,969 | 388,573 | 358,824 |

| Heifers | 12,369 | 10,537 | 455,802 | 433,705 |

| Total | 39,560 | 38,995 | 1,576,893 | 1,544,497 |

Bord Bia has forecasted beef kill numbers to tighten in the short-term, while firm demand for beef from key export markets is expected to continue.

Bord Bia expects the prime cattle kill to fall by 46,000 head and the cow kill numbers to drop by 10,000 head in 2025, with the overall kill for the year expected to be around the 1.69 million head mark or 4% below 2024.

Sources close to the market expect supplies of prime cattle to remain below demand levels into the first quarter of 2025.