Milk Price Tracker: Which co-ops top the league?

Last month, AgriLand and the Irish Creamery Milk Suppliers’ Association (ICMSA) launched our latest new development, the ‘Milk Price Tracker’.

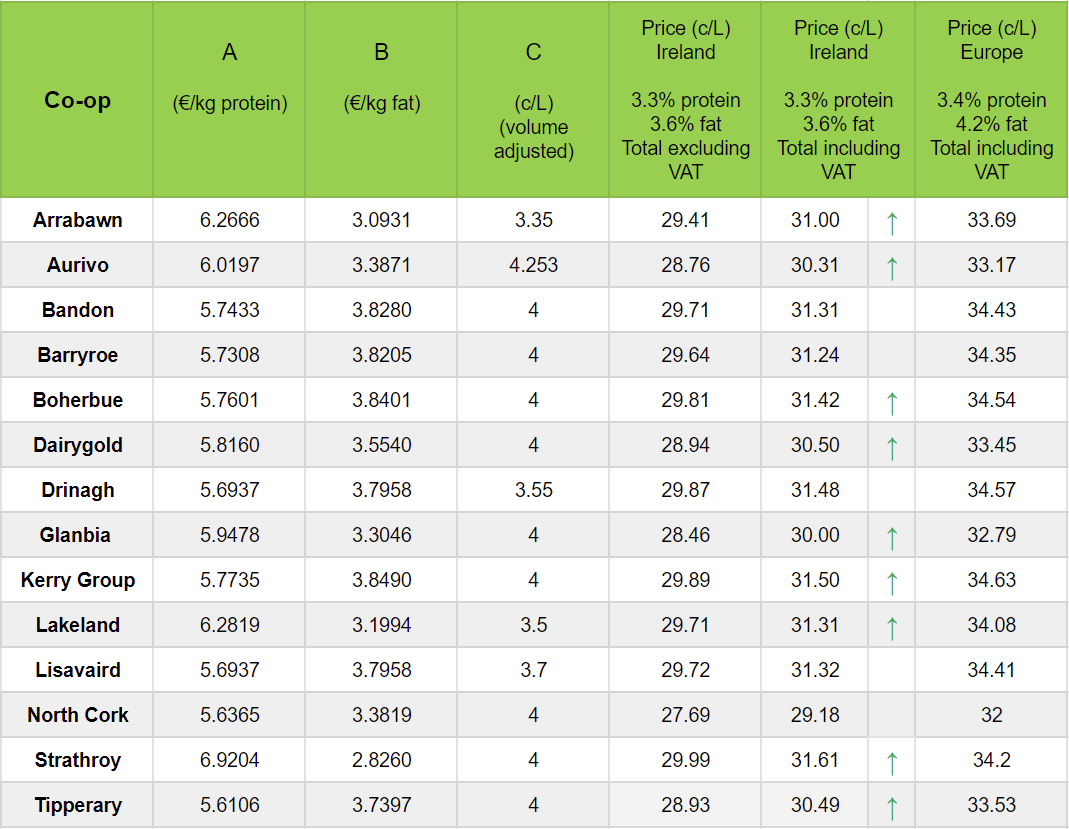

This month, we bring you our most up-to-date Milk Price Tracker table with the most recent milk prices – from the most significant Irish dairy co-ops – for the month of December.

We have added a new feature to this month’s table, where a green arrow indicates an increase in milk price; a blank space signifies no change in price; and a red arrow indicates a drop in milk price – although fortunately no co-ops dropped milk price for last month.

Not only does the table enable a supplier to see what his or her own co-op is paying, but they also provide visibility of what competing co-ops are paying – on a like-for-like basis.

It is important to note that the cent-per-litre (c/L) milk prices – shown in the table below – are calculated using the widely-accepted milk pricing system (an approach employed by most Irish co-ops).

It should also be noted that, when calculating the base prices (on a c/L basis), we have used a fixed mass density factor – to convert from kilograms (kg) to litres (L).

Moreover, the Irish c/L milk prices – quoted in the table – are base prices at the ‘standard’ fat and protein percentages cited by the vast majority of co-ops (i.e. 3.3% protein and 3.6% fat).

We also include base prices at ‘standard’ European criteria (i.e. 3.4% protein and 4.2% fat).

The milk prices in this table (below) are those quoted by co-ops for the month of December (2019).

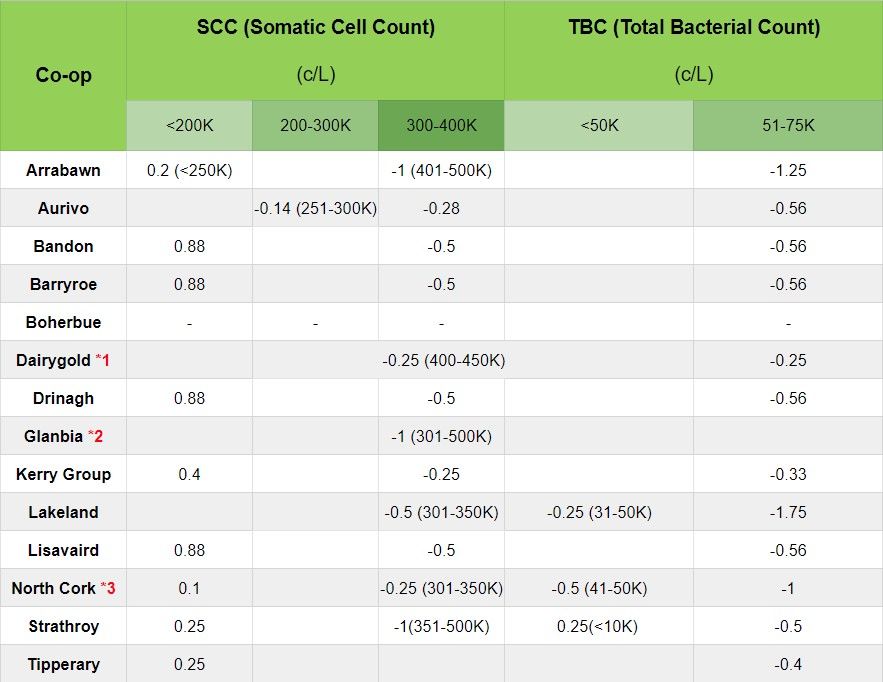

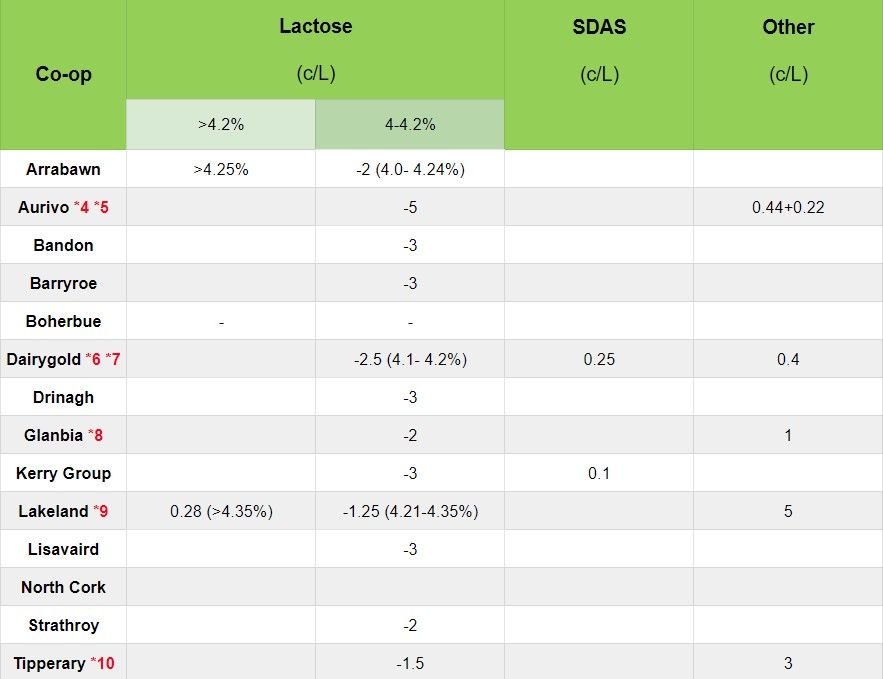

This table (below) outlines some of the most significant bonuses offered by the various co-ops, as well as some of the key penalties that may be imposed.

The focus is on bonuses/penalties that have the greatest impact on a supplier’s ‘milk cheque’.

With regard to all of these tables (above), please see these explanatory notes (below).

Commenting on the latest milk prices, ICMSA dairy chairperson, Gerald Quain, expressed satisfaction that milk purchasers and co-ops have somewhat raised their base milk price; but noted that considerable scope remained for further improvements in the coming months.

He stated:

Farmers can now track all prices and compare their own co-op, to other processors, on the most practical like-for-like basis; so we’re delighted that this type of information is in the digital space for all to see.

“The really noticeable point here is that the Ornua Purchase Price Index (PPI) was running over 32c/L for milk supplied in December and yet, here we are – a week before February – and still none of the prices quoted in the Milk Price Tracker are at this level.

“While some are coming close, it is essential that this comparison is available to all farmers, to view, check and note the discrepancies from the PPI.

“Hopefully, in the coming months, we’ll see a concerted attempt by the co-ops to raise their prices to a level that at least equals the Ornua PPI,” concluded Quain.