Rabobank lowers its 2023 milk production forecast

Ireland had one of the most notable farmgate based milk price declines in Europe in July, according to a new report from Rabobank.

According to the bank, Ireland's large exposure to the global milk powders market resulted in a major drop in preliminary July milk prices in 2023 compared to corresponding prices for July 2022.

It highlighted in its latest Global Dairy Quarterly report that this resulted in "more negative sentiment among Irish farmers".

In contrast according to Rabobank, on the European mainland milk prices showed more "resilience" particularly in France and Italy.

However the latest quarter three (Q3) report from the bank also suggests that some "modest downward adjustments" are expected in the months ahead.

According to Rabobank domestic demand growth is the "key factor" driving European dairy market recovery.

But although food price inflation slowed in quarter two of this year, the report outlined that prices remain well above 2021 levels and the bank does not expect a widespread response to the easing of food prices until 2024.

"Consumers are managing their expenses as their lost purchasing power has yet to recover," it warned.

One trend identified in the Q3 report is that dairy cow slaughter rates during the first five months of the year are down in most European countries, although the Netherlands is the exception to that.

Average EU slaughter cow prices were, according to Rabobank, under pressure during the summer months but it expects that the improved outlook for feed availability will ease pressure to lower herd sizes.

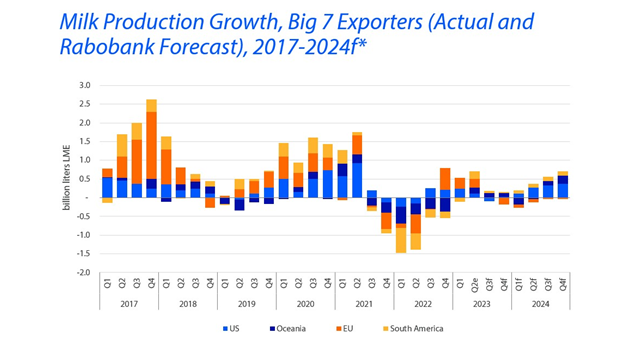

According to the quarter three report in recent months lower milk prices in most key global markets have reduced supplies.

Milk production from the "Big 7" - which includes the EU, US, New Zealand, Australia, Brazil, Argentina and Uruguay - export regions is anticipated to grow by just 0.3% year on year in 2023.

Rabobank stated: "The downgrade from last quarter’s estimate of 0.5% is driven by reductions in most key global regions, including the US, EU, and New Zealand.

"Into 2024, output is expected to climb by 0.4% - far less than the 1.6% annual average gain seen from 2010 to 2020".

But Lucas Fuess, senior analyst dairy at Rabobank, is optimistic that the current position regarding global milk production may reverse.

"In our view, however, a possible whiplash effect is growing in probability. We may see a demand resurgence emerging months before global milk output can recover.

“In the second quarter of this year, we declared that ‘it’s always darkest before the dawn' and although clouds remain this quarter, the storm will not last forever," Fuess said.