'Next harvest could be a different story than this year on prices'

Having just come out of a dry year, where global grain yields were back and feed demand was strong, the high prices that were seen at harvest caused a flurry of winter planting and in turn an increase in the area sown.

Average yields in the coming season would not bode well for grain price according to James Nolan. The grain trader, with R&H Hall, gave farmers an insight into markets at the Quinns of Baltinglass tillage conference last week.

“Export regions including the Black Sea and countries which became net importers last year – such as Germany, Sweden and Denmark – have all increased acreage,” James explained.

Reduced cereal yields last season drove prices up, but that high price proved too much to take for many buyers and a move was made to products like maize which were priced significantly lower.

Corn or maize grain has dominated feed within Europe in recent years and I think it’s going to remain a price setter in the feed market in north-west Europe.

However, there is a draw down on stocks and James noted that: “While planted area isn’t an issue, weather may play a role – particularly in South America, where dry weather is kicking in at the moment.”

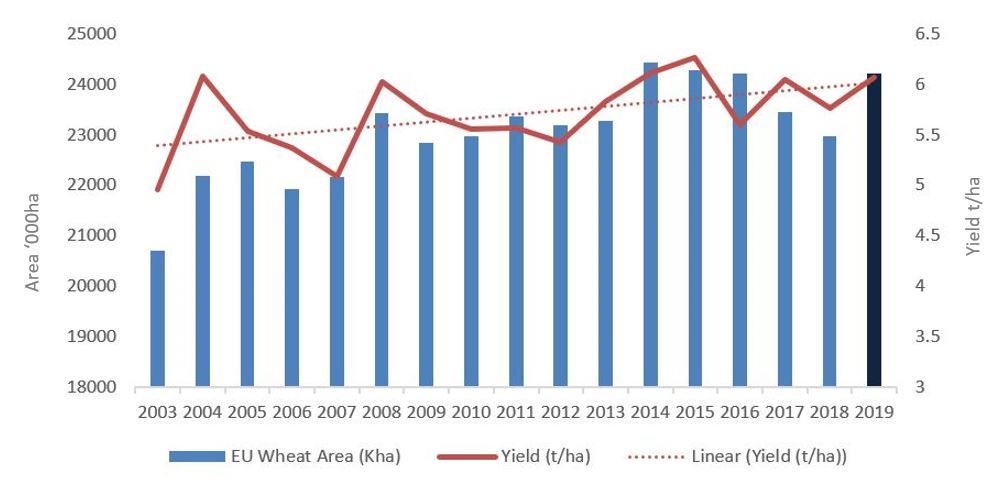

Increase in area planted

The planted winter cereal area in Europe has increased by 5-6% – that’s approximately 1 million hectares. The major exporters have increased area; Germany for example has increased its area by 6% from the 2017 season – the poor autumn of 2017 resulted in less area planted in the 2018 season.

Russia has increased its wheat area by approximately 200,000ha – that’s approximately two-thirds of the total tillage area in Ireland.

New crop outlook is purely dependent on weather and politics. We’ve seen high prices this year; it has incentivised farmers to plant again.

According to James, 2018 was the first year in seven where there was a draw down on wheat stocks.

“We’ve actually seen a draw down on wheat stocks and that was driven by the loss of production in major exporting regions – namely the EU and Black Sea. Australia has also become a massive issue.

Consumption has outstripped production.

The draw down has come from net exporters importing grain. Denmark and Germany for example both imported grain this season.

In one week in August last year Germany bought 1 million tonnes of wheat.

So what happens if yields are average next season?

The concern that the R&H Hall trader has is that if only average yields are reached in 2019, the increase in planted area will result in a large wheat supply.

All you can do looking forward is take a trend or an average yield.

James noted that there is potential for 148 million tonnes of wheat to be produced from 24 million hectares in the EU next season – that’s an increase of over 5% in EU wheat area. In the year just gone out 136 million tonnes were produced. The biggest increase in planted area came from the Baltic region.

“Demand has decreased this year; if we get this production increase where does it go? New crop in particular is much cheaper than the current crop.

“The market predicts that this area is there and is predicting an average yield. If this comes together there’s a big supply and we need to find a market, but the big unknown is yield.

There is no risk in new crop; the market does not perceive a risk today.

James explained that when new crop wheat prices start rising, they will struggle to find consumer demand.

“If it rises into April, May and June and it turns out that you get average yields, I think next harvest could be a different story than this year on prices.

If we get the supply at harvest and the demand is not there, prices could get tricky. You’d be fearful of harvest pressure this year if the supply comes and we’ve already lost the demand.

However, the dry autumn is a reminder of another high-price year.

“The autumn crop is gone into very, very dry ground and the big fear here is that the yield potential won’t be there to come from a very dry autumn into a dry spring, potentially another dry summer.

“You could be looking at yields being decimated, something like what happened in 2012.”

Current crop

Many Irish farmers still have grain in sheds. Unfortunately, the high of the market looks to have passed. High prices curtailed European exports, which are 27% behind the same time last year, James explained.

“The concern here is we only have four months left in the marketing year. Europe needs to export 0.5 million tonnes / week until the end of June.

Russia, this year, has 17 million tonnes less supply. Last year it exported a record 40 million tonnes. Its export pace is running 18% ahead of last year.

James added that if Russia continues at its current pace with wheat exports, it will have depleted its stocks by the end of April. Europe is waiting for that slow down in exports from Russia.”