'In-between period' sees lamb prices strike €5/kg

The lamb market is currently in an ‘in-between period’, as the glut of intensively-finished lambs has yet to become available throughout the marts and factories.

Given this, lamb buyers are struggling to source lambs; many are currently contacting traditional finishers to maintain throughput.

And with this shortage comes a higher price. As it stands, many farmers are achieving €5/kg for their lambs – up 10c/kg on last week.

Although processors are only quoting a base price of 480-490c/kg currently, the addition of QA and producer group bonuses is helping to bring the prices achieved at farm level up to the €5/kg mark.

Therefore, the ball is very much in the farmers’ court when it comes to marketing lambs. However, it must be emphasised that clipping charges are still in play in the market.

But, farmers may be able to use the tightening of supplies to negotiate deals where this charge – of up to 20c/head – is wavered. As one farmer put it earlier this week: “If the buyers want my lambs, they’ll give me back the 20c/head.”

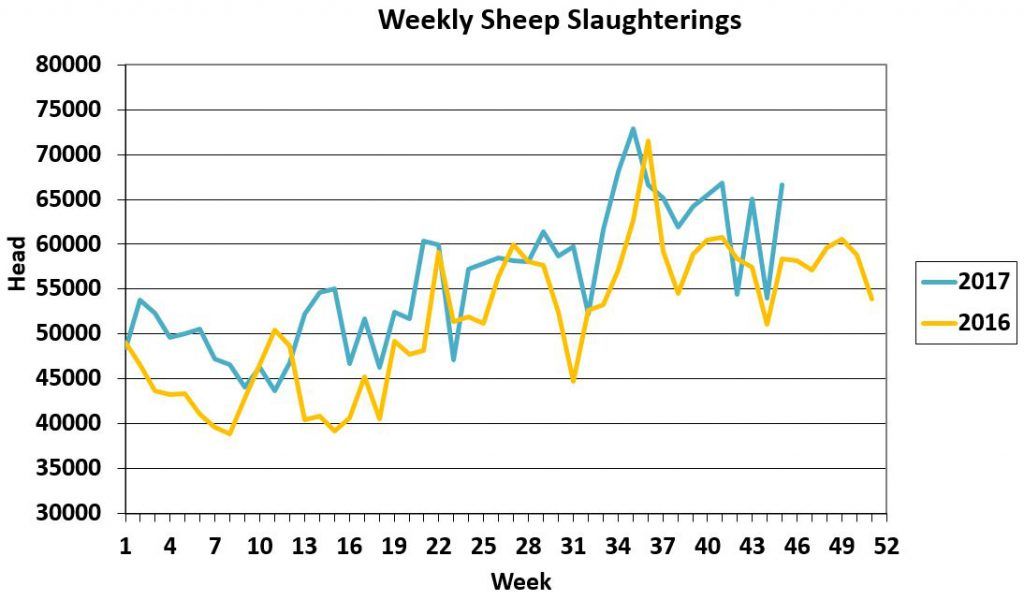

Tightening supplies

Over the last number of weeks, the number of sheep slaughtered in Department of Agriculture approved plants has tightened considerably.

The second week of November saw some 66,638 sheep slaughtered in approved plants; 55,771 of these were spring lambs and 10,766 were cast ewes and rams.

In addition, the cumulative sheep kill for the year is currently running about 10% ahead of 2016 levels. This comes as the hogget, spring lamb and cast (ewes and rams) kills have climbed by 18%, 4% and 13% respectively.