Ciaran Fitzgerald: Food pricing issue remains a core challenge

As I have said previously, the EU Green Deal, while clearly admirable in concept, contains a continuing disconnect in EU food and agricultural policy, with regard to food pricing.

The EU is rigid, zero tolerant and highly interventionist on food quality standards, production methods, animal health and food hygiene and increasingly, environmental and climate impact regulations.

However it has been silent, abstemious and 'laissez faire' in refusing to intervene in any shape or form in food pricing.

Food pricing

The rigid application of regulation and compliance costs at production and processing level, ends at the factory gate it seems.

Thereafter the EU Commission refuses to get involved, trusting instead the invisible hand of competition and consumer preferences, cheered on by some pithy aspirational 'declarations' about sustainable pricing and support for climate friendly diets.

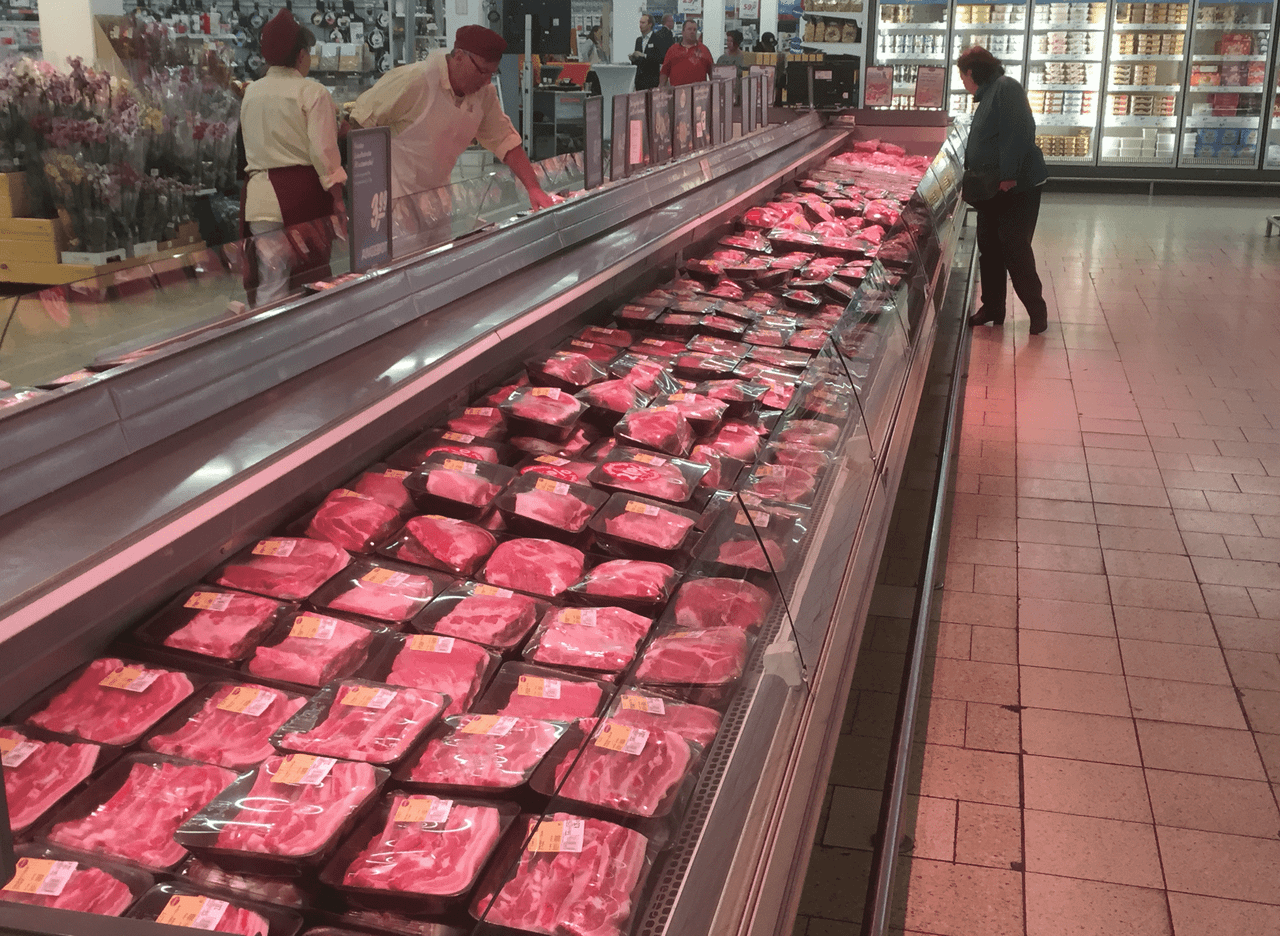

All of which means that production and processing costs rise, but there is no cost recovery in the European marketplace because dominant retail 'competes' for consumer footfall, by using fresh food products as loss leaders.

In essence, it is pricing fresh meat, vegetables, fruit and dairy products at or below cost.

Thereby killing producer margins and producer brands while replacing them with own label retailer brands, while the retailer captures any lost margin on the hundreds of other products sold in a multi-buy grocery shop.

It does not have to be like this

Any cursory examination of European consumer markets across a broad range of goods, shows that these markets function quite well.

This is despite producers of cars, mobile phones, I.T software and hardware, electricity and gas, medicines and pharmaceutical drugs, all having what is denied to food producers.

They all have built in or regulated selling power and even mandatory pricing policies, which enable the producers to have a say in the final price of the goods they produce.

In particular, it prevents retailers / resellers of this vast range of consumer products, to sell below cost.

Cars vs food

Indeed the car / automobile sector is quite interesting in terms of comparisons with the food sector, not just on price, but on the evolution of its climate action story and environmental challenges.

When the growing awareness of fossil fuel damage to the environment - particularly climate change - led to calls for government action in the 1990s, the long-term feasibility of everybody continuing to have private cars was mooted, and the primacy of public transport or cycling was proffered as a policy response.

This notion of an end to private car ownership didn’t stick however. Not because it wasn’t environmentally beneficial, but because consumers / voters wouldn’t wear it.

Instead the replacement of internal combustion engines with electric battery or even hybrid ones, has been evolving official policy across the EU and indeed across the globe.

There have been strong commitments to phase out diesel cars firstly, and then petrol ones by as early as 2030 in the case of some national pledges, balanced by incentives / tax supports to purchase electric ones.

It seems to me that this evolution in the debate around private cars has useful comparators for the current contemplations about food.

More balanced approach to food pricing

This surely represents a more balanced approach than some of the sometimes hysterical, and rarely factual, anti-dairy and meat propaganda currently being pedaled.

Throughout the debate around the future of private motoring, cars of all hue - diesel petrol, hybrid etc, have continued to be positively priced.

Even diesel cars, despite an horrendous reputation for environmental damage, continue to be allowed to be produced (indeed getting some state aid in EU countries in 2020 under Covid-19 supports).

Surely an equivalent, balanced end result, in the case of meat and dairy would be a meaningful, statutory, price and policy support system, which guides consumers to choices that are best in class / more carbon efficient within the category.

Carbon efficiency in trade deals

Furthermore, as recognised in the Intergovernmental Panel on Climate Change (IPCC) report of 2019, this carbon efficiency concept could be built into World Trade Organisation (WTO) and bilateral trade deals, in order to address the very real issue of carbon leakage.

Importantly, such a balanced approach would be in line with the UN Paris Accord which supports ”increasing the ability to adapt to the adverse impact of climate change and foster climate resilience and low greenhouse gas [GHG] emissions, in a manner which does not threaten food production".

A meaningful and effective food price support mechanism, aimed at securing real value to low environmental impact carbon efficient agricultural production, including meat and dairy, would in my view, position climate impact measures in food and agriculture on a pragmatic, balanced, yet science-based footing.