Ciaran Fitzgerald: EU needs to address price volatility in agri-sector

Fixed-price milk schemes are crucial, but the European Green Deal also needs to look at some form of crop and livestock insurance to deal with income and price volatility.

The current income squeeze in the pigmeat sector, and indeed the surge in input and energy prices across the agri-sector, highlight again the need for the Common Agricultural Policy (CAP) to look in greater depth at price and income volatility challenges.

Current agri commodity price increases are welcome, but clearly come with a number of major caveats.

The price of agri products has not gone up as much as the price of inputs such as feed and fertilisers, and there is always likely to be a rebound as substitutes are found or demand is curtailed.

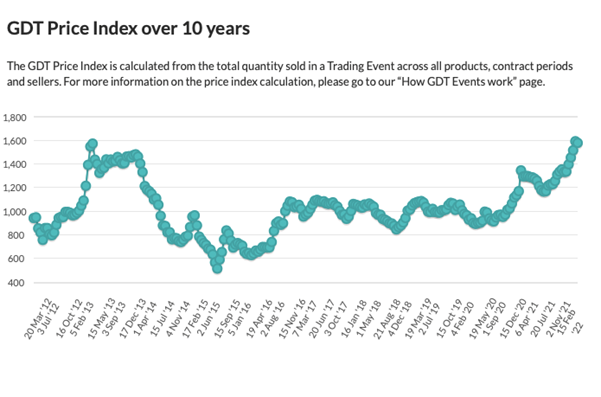

The above index indicates that price volatility is a persistent feature of global trade in food commodities, and in particular, the dairy sector.

Indeed, price volatility was very much what was promised when the EU dismantled the pre-1990, interventionist CAP support system, along with the removal of controlled supply through milk quotas in 2015.

As part of this new 'freedom to farm' market-led ideology post-2008, the quid pro quo for fluctuating prices (and incomes) was to be the ability to increase or decrease production to adapt to increasing demand or increased supplies.

This supply response element of freedom to farm has been forgotten in the anti agriculture trope of the last two years in Ireland and the EU in support of the suppression of EU and Irish agri output.

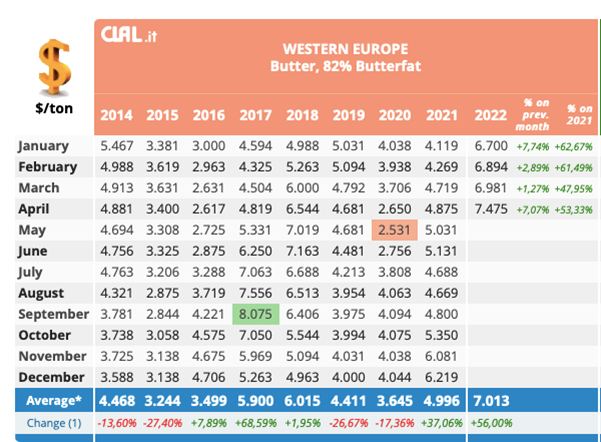

Increasingly, the time lag between high and low prices is not very long as the chart below from CLAL (an Italian dairy economic consulting firm) indicates; EU butter prices reached a high of over €8,000 in September 2017 and were down to €2,500 or so in May 2020.

Dealing with price volatility not part of CAP

The major change in the focus of CAP supports over the last 30 years was the introduction of direct payments as a replacement for market supports in the 1992 CAP reform.

With the requirement of the World Trade Organisation (WTO) to decouple direct payments from production and the evolution of environmental imperatives, the current CAP sees a continuing dilution of market supports with direct payments morphing largely into environmental or greening payments.

As indicated by the table and charts above however, volatility never went away and actually increased when intervention systems were dismantled.

And so, the need to address volatility through a macro policy across agri sectors has not diminished either.

Anti-volatility policy

The best of example over a long number of years and clearly one that is compatible with WTO rules of a fully functioning, meaningful anti-volatility policy measure, is the U.S Department of Agriculture (USDA) crop and livestock insurance programmes and its variations.

The principal USDA programmes are:

In the CAP reform discussions in 2014, and to a lesser extent the 2020 CAP reform process, the issue of addressing price and income volatility in agriculture through some form of EU-wide-based support system like the US crop insurance programme was broached, but was not accepted by the EU Commission.

The EU has refused consistently to look at 'public' EU-wide, anti-volatility insurance measures in any shape or form and so EU and Irish agriculture remains vulnerable to a surge in input prices that is not reflected in the prices of commodities/output.

This 'disconnect' between extremely high input prices and non responsive market prices is at the heart of the current pigmeat sector crisis.

Importance of fixed milk schemes

In that context and particularly in the absence of any change in attitudes to an EU-wide CAP-based 'insurance' approach, Ireland is lucky to have well developed fixed price schemes in dairying which were first introduced in 2011.

They can currently cover up to 15% of producers' output and also have an input price adjuster factored in.

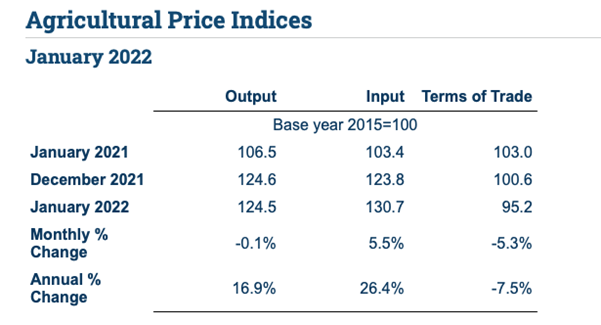

As the Central Statistics Office (CSO) overall Agricultural Input Price Indices below indicates, even where there have been increases in output prices in areas such as dairy and beef, the overall input/output index (which still doesn’t show the further increase in input prices due to the Russian invasion of Ukraine), is negative for producers.

While in times of significant output price increases, fixed price schemes may not seem perfect, but over the medium to long-term, they are an essential element in combating volatility risks for Irish dairy farmers.

Not only is price volatility a fundamental feature of global trade, but the EU continues to shy away from any form of public EU-wide scheme.