Beef trade: No change in quotes but farmers hold out for more

There is increasing pressure on factories to pay more for cattle, as the factory/farmer beef price stalemate has continued and both parties are ‘sticking to their guns’.

Steers are currently sitting at a base of 390c/kg, while heifers are trading at 400c/kg in most cases. Some farmers, especially those with large numbers of in-spec stock to market, have been receiving prices of 5c/kg above base quotes. At the upper end of the scale, this brings heifers up to a base of 405c/kg.

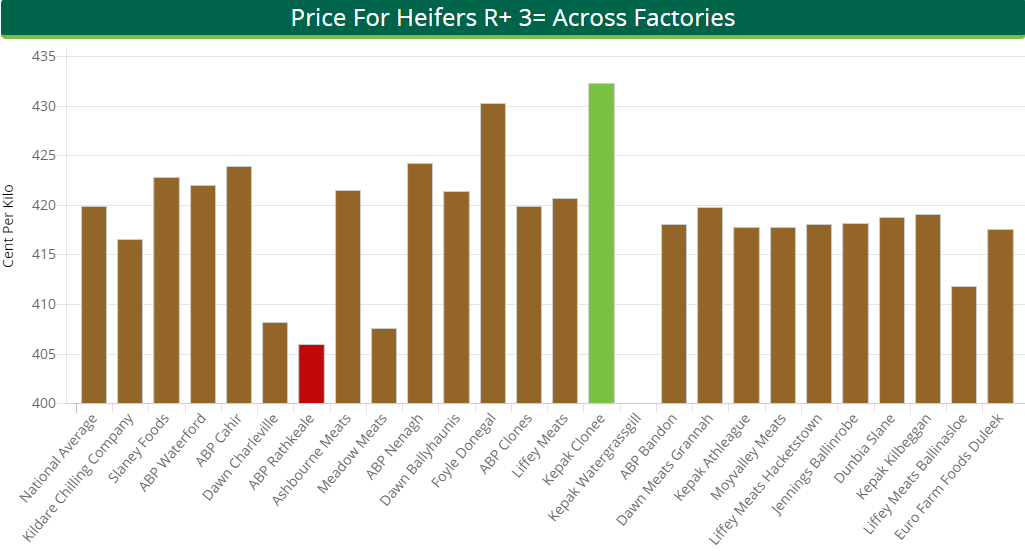

During the week ending February 11, in-spec, R+3= heifers made a top price of 432.25c/kg, while the average price paid stood at 419.91c/kg. These prices are inclusive of breed-specific and QA bonuses where applicable.

Furthermore, a top price of 417.49c/kg was achieved for R+3= steers; the average price paid for these animals stood at 406.84c/kg.

As has been the case in recent weeks, cow prices have also remained relatively stable and most buyers are offering 325-330c/kg for P-grade animals. Procurement managers are starting negotiations with farmers for O-grade and R-grade cows at 330c/kg and 350c/kg respectively.

However, it must be noted that there is a wide variation in the prices being quoted to farmers. This depends on the location and demand of individual processing plants.

Cattle Supplies

Of the 34,732 cattle slaughtered during the week ending February 4, just over 60% of these animals were steers and heifers.

Some 11,153 steers were slaughtered in beef plants that week – an increase of 719 head – and heifer throughput stood at 10,000 head. Meanwhile, throughput decreases were recorded for young bulls (-123 head), cows (-198 head) and aged bulls (-112 head).

Cattle supplies at Irish processing plants for the week ending February 4 amounted to 34,732 head. This was an increase of 1.7% on the previous week. It is also a 0.79% or 275 head increase on the corresponding week in 2017.

EU markets

In Britain, the Agriculture and Horticulture Development Board (AHDB) reported that – during the week ending February 10 – R4 steers made 368.5p/kg (416c/kg). R4 heifers also made the equivalent of 416c/kg.

Looking at young bull returns, it was reported that overall prices increased by 3.9p/kg (4.4c/kg) on the previous week. R3 young bulls made the equivalent of 392.6c/kg.

Prices were reported to be strong for cull cows during this period. Animals falling into the O-grade category made the equivalent of 307.4c/kg.

The Irish Farmers’ Association’s (IFA’s) national livestock chairman Angus Woods outlined that prices in the UK and across Europe are all ahead of Irish returns.

An analysis by the IFA shows that for the week ending February 4, R3 steers in the UK made the equivalent of 437c/kg; R3 young bulls made 436c/kg in Italy; and 411c/kg in France. Meanwhile – in Germany – young bulls made 422c/kg, while similar animals made 419c/kg in Spain.