Beef kill: 2026 cow kill down by 15.5% or over 28,000 head

Latest official beef kill figures show weekly cattle supply numbers remaining steady despite the overall kill this year being down by 9.2% or almost 74,700 head.

The largest drop-off in supplies to date this year has been in the cow category, with factory cow supplies down 15.5% or just over 28,400 head.

The heifer kill-to-date this year is down by 9.9% or 25,700 head while the steer kill is down by 6.8% or 20,300 head.

The table below details weekly beef kill numbers in the week ending Sunday, June 14, versus the same week of last year, the cumulative beef kill-to-date this year versus the same week of last year, as well as the change in numbers and percentage changes:

| Animal Type | Week ending June 14 | Same week of 2025 | Weekly Change | Cumulative 2026 | 2025 Cumulative | Cumulative Change |

|---|---|---|---|---|---|---|

| Young Bulls | 2,917 | 2,901 | +16 (+0.6%) | 56,336 | 56,443 | -107 (-0.2%) |

| Bulls | 790 | 537 | +253 (+47.1%) | 11,605 | 11,701 | -96 (-0.8%) |

| Steers | 10,862 | 10,094 | +768 (+7.6%) | 277,946 | 298,251 | -20,305 (-6.8%) |

| Cows | 6,553 | 7,041 | -488 (-6.9%) | 154,666 | 183,083 | -28,417 (-15.5%) |

| Heifers | 8,828 | 8,529 | +299 (+3.5%) | 234,722 | 260,461 | -25,739 (-9.9%) |

| Total | 29,950 | 29,102 | +848 (+2.9%) | 735,275 | 809,939 | -74,664 (-9.2%) |

Some procurement bosses had suggested supplies were becoming tighter last week but the official figures show supplies remained steady which could be a signal of some lift in demand levels.

Price cuts have halted for this week also after several consecutive weeks of declines.

There are some signs of more positivity entering the trade although these have yet to materialise in official factory price offer increases.

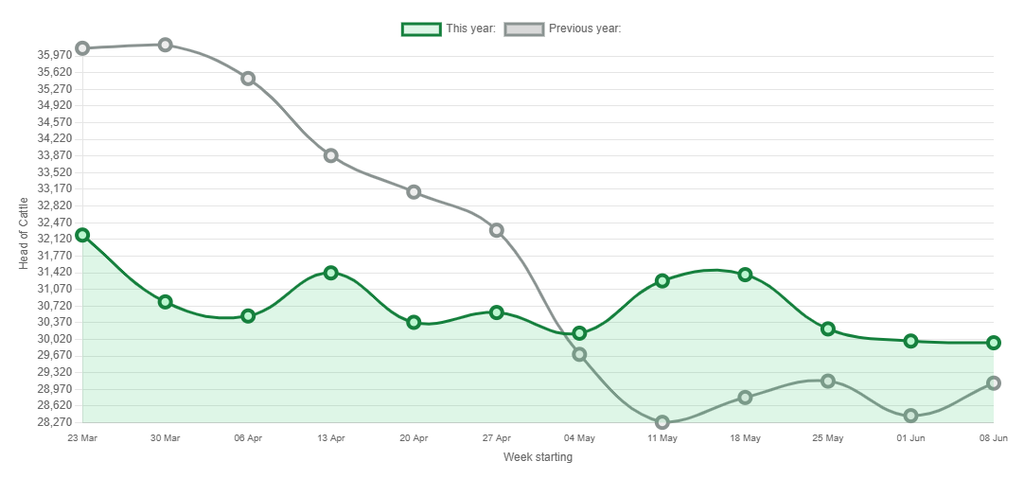

The graph below shows how weekly beef kill numbers have been trending compared to last year:

While overall kill numbers to date this year are down, supplies are expected to recover. As the graph above indicates, supplies dropped off significantly into the second half of 2025 and failed to recover for the remainder of the year.

This year (2026), supplies have been remaining more steady at above or below the 30,000 head/week point.

The first quarter of 2026 also saw a rise in average carcass weights, which is a positive for both farmers and processors.

Generally speaking, most factory outlets have no issue with carcass weights up to 400kg. While most do have markets for heavier carcasses, these are more niche.

The average steer carcass weight in the first quarter of this year was 360kg, up 25kg from the first quarter of 2025 when the average steer carcass weight was 335kg.

The average heifer carcass weight was up 17kg in the first quarter of this year compared to last year.

In Q1 of 2025, the average heifer carcass weight was 298kg vs 315kg in Q1 of this year.

The average cow carcass weight increased by 11kg in Q1 this year compared to Q1 of last year.

In Q1 2025, the average cow carcass weight was 292kg. In Q1 of 2026, the average cow carcass weight was 303kg.