Stalemate in factory/farmer beef price battle

Our Duke was a ready winner of the Irish Grand National in Fairyhouse on Monday, but there appears to be no clear winner in the factory/farmer beef price battle this week.

Cattle supplies continue to remain relatively tight but, buoyed by a four-day week, factory buyers are confident that they will secure the numbers they need in the coming days.

And, as a result, many plants have opted to maintain steer and heifer quotes at last week’s level of 390-395c/kg for steers and 400-405c/kg for heifers. Both prices exclude Quality Assurance scheme bonus payments.

Despite the lack of movement in the steer and heifer markets, there appears to be a bit more bite in the cow trade and factory buyers are willing to offer 320c/kg for P-grade cows, 330c/kg for O-grade cows and 340-350c/kg for R-grade cows.

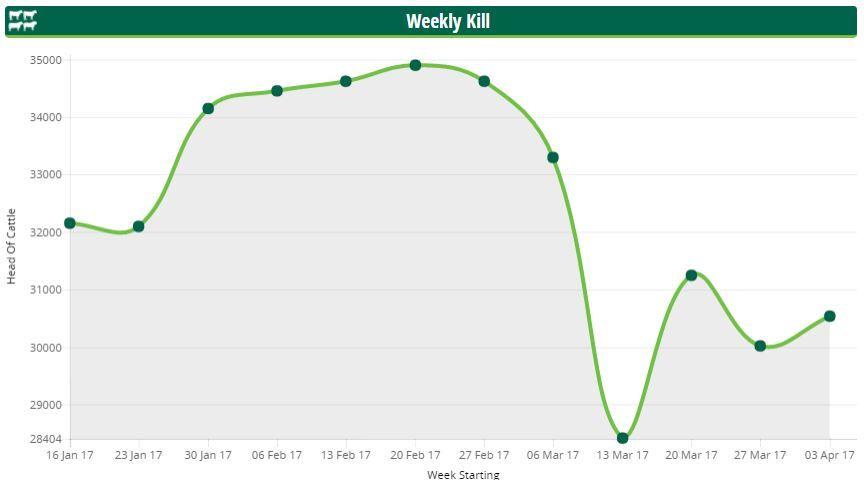

Cattle supplies balance out

In recent weeks cattle supplies have also returned to more normalised levels.

During the week ending April 16, some 30,162 cattle were slaughtered in Department of Agriculture approved beef export plants.

This brings the average weekly kill for the last four weeks to 30,731 head – a substantial drop from the weekly throughputs of almost 35,000 head seen during February.

In total, some 487,002 cattle have been slaughtered in approved export plants so far this year. This is an increase of 10,583 head or 2.22% on the corresponding period in 2016.

A closer look at the weekly kill

Of the 30,162 cattle slaughtered during the week ending April 16, over 67% of the total weekly kill were steers and heifers.

Some 11,726 steers were slaughtered last week, which is a fall of 197 head or 1.6% on the week before. Meanwhile, the weekly heifer kill increased by 4% or 332 head to reach 8,635 head.

Increases were also seen in aged and young bull throughputs, which climbed by 25% (125 head) and 2.4% (+74 head) respectively.

However, cow throughput actually declined by almost 12% as just 5,932 of these animals were slaughtered last week – a fall of almost 800 on the week ending April 9.

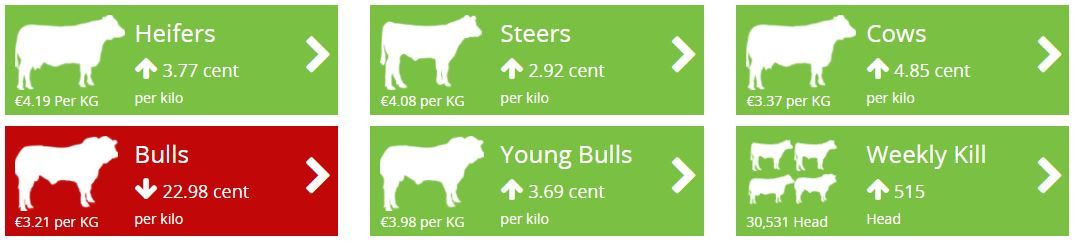

Prices up with the exception of aged bulls

The average price paid for aged bulls (U-2-) during the week ending April 9 stood at 321c/kg – a drop of almost 23c/kg on the week before.

All of the other categories of cattle, including heifers, steers, cows and young bulls posted price increases on the Agriland Beef Price Calculator.

Base heifers traded at 419c/kg (+3.77c/kg) during the week ending April 9, while farmers were paid an average price of 408c/kg (+2.92c/kg) for base steers.

Meanwhile, cull cow (O=3=) and young bull (R=2+) prices also increased in early April climbing by 4.85c/kg and 3.69c/kg respectively.

Main markets

According to Bord Bia, a firm cattle trade was reported in the UK last week.

Cattle prices from the AHDB remain relatively steady in Sterling terms and R4L grade steers averaged 356.5p/kg or 420.06c/kg during the week ending April 8.

In France, it says, a further increase was reported in the trade on the back of a seasonal upward shift in demand due to Easter.

Demand was highest for domestically-produced beef and retail promotions focused on rump, ribs and loins produced in France.