Record-high dairy prices but milk collection marginally down in EU

EU dairy prices are at record levels but farms' margins remain tight; milk collection looks set to drop by 0.6%; while butter exports are due to rise by 2% in 2022. These are just some of the highlights contained in the EU’s latest Short-term outlook for EU agricultural markets in 2022.

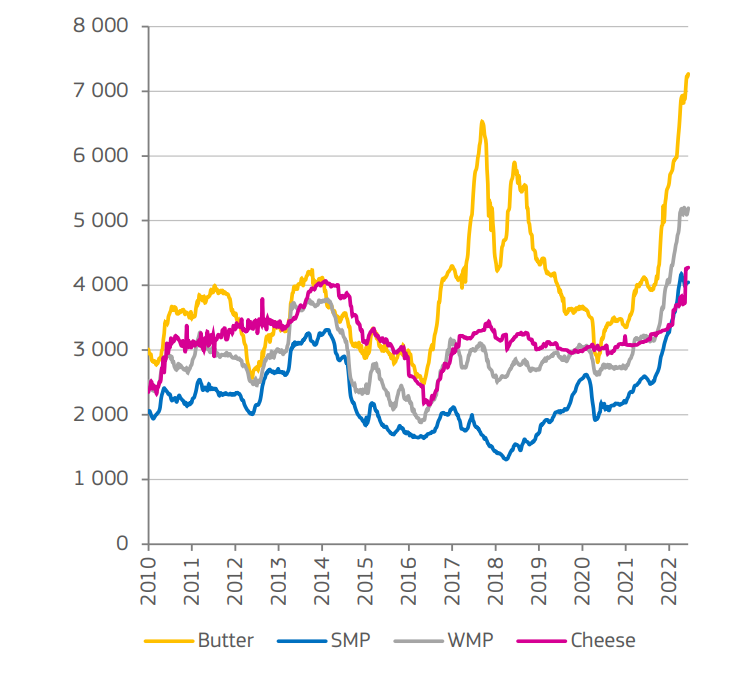

Since the beginning of the year until mid-June, dairy prices grew by around 25% for skim milk powder (SMP) and cheeses, and by 30% for butter and whole milk powder (WMP).

Prices for EU whey powders lag behind this, by 16%.

Russian invasion

While EU SMP prices showed some relaxation after an initial shock caused by the Russian invasion of Ukraine, and now remain stable, EU butter and cheese prices continue to increase.

Contrary to SMP, EU prices for WMP did not relax and remain at a stable but high level since the invasion, according to the outlook.

All these EU dairy prices are at a record high.

In mid-June, EU butter prices reached close to €7,300/t, SMP prices are more than €4,000/t, and WMP prices are close to €5,200/t.

By contrast, EU whey powders prices are at a lower level - €1,300/t - and compared to other products, even showed a declining trend since the invasion started.

Raw milk

These developments are driving up the EU raw-milk price, which, in May, was almost €48/100kg (40% above five-year average).

The EU milk equivalent price (based on SMP and butter prices) remains high also.

Considering the relationship between the two, the upward trend on EU raw-milk prices is expected to remain for the following months, and no seasonal price relaxation is likely to take place, the outlook states.

Despite an increasing EU raw milk price, dairy farms’ margins remain tight due to sustained high input including feed and logistic costs.

High costs

Record EU dairy prices also affect the EU’s competitiveness in trade compared to other main players - Oceania and the US, for example - according to the outlook.

In mid-June, the EU is competitive only in cheese (9% below the US price, the second-lowest market price), while in butter and WMP, the EU is more than 30% above the lowest market price (Oceania prices), and 5% for SMP (the US price).

The global milk-supply growth is likely to remain limited in warm and dry weather in some US producing regions, and high input costs are considered a limiting factor for a significant expansion of milk production, despite an increase in the size of dairy cows' herd. Nevertheless, the growth of the US milk production could be still positive.

In the case of New Zealand, high input costs could weigh negatively on farms’ profitability, although less than in other world regions due to a higher share of grass feeding.

The milk production increase will depend on weather conditions. However, seasonal prospects remain positive taking into account the comparably low levels of the last season.

Milk

From January to April, EU milk deliveries dropped by 0.6%. Among the largest-producing countries, only deliveries in Poland, Italy and Denmark grew by 2.4%, 0.4%, and 0.6%, respectively.

Germany, France and Netherlands continued to decline, however, down 1.7%, 1.3%, and 2.3%, respectively.

Irish milk deliveries dropped as well, down -0.7%, compared to an exceptionally high level of last year.

Warm and dry weather during spring - causing heat stress to cows and affecting grass and crop development - combined with high feed costs and the difficulties of sourcing GM-free feed in Germany, resulted also in a drop of milk fat and protein availability.

In January to April, the drop for both was 0.8%.

Weather

Weather prospects in upcoming months remain negative for pasture developments in Central and Eastern Europe as well as in Italy, the outlook predicts.

Combined with sustained high prices of crops destined to feed, this is likely to affect farms’ economy negatively and to lead to a further herd reduction (-1%) in 2022, and lead to lower yield growth (+0.4% compared to 1% in spring).

As a result, in 2022 EU milk deliveries could drop by 0.6%, mainly due to a drop in Q2 (-1%), followed by declines in Q3 and Q4 (-0.6% for both).

This would then contribute to tighter global milk supplies in 2022.

Dairy products

In May, an annual rate of change of EU consumer prices for milk, cheese and eggs combined was above 11%, stronger for fresh milk (almost 14% for the whole milk, close to 13% for the low fat milk), butter (more than 26%) and lower for the yoghurt (9.5%) and cheese (10.6%).

Nevertheless, it is assumed that EU dairy consumption could grow, overall, by 0.3%, supported by the ongoing recovery of foodservice, with other food products seeing even higher inflation rates.

After a period of lockdowns in 2020 and 2021, accumulated personal savings will likely

Even if the EU milk deliveries are expected to decline in 2022 by 0.6%, EU cheese production could grow by 0.5%.

This is thanks to the competitive prices on the world market (+2% of export growth), and mainly thanks to growing flows to the US and recovery of the UK-destined exports.

This could be combined with stable domestic retail sales and foodservice recovery, supporting the level of the consumption of last year (+2% on 2020).

Among other dairy products using milk fat in their processing, EU cream production is expected to grow as well (+1%), also supported by the domestic and global demand, although less than in 2021 due to a likely reduced demand from China.

This reduced demand could also weaken the flows of drinking milk but EU FDP exports could still grow by 2% while domestic use could continue declining (-0.4%).

EU butter production is expected to be reduced (-1%), with domestic consumptionbeing stable and despite some recovery of EU shipments.

This could be supported by the reduction of stocks (-35 000 t) which are expected to be at the low level. The EU WMP production is likely to decline as well (-5%), with negative expectations for exports (-8%) as well as domestic processing (close to -3%).

Among the milk powders, it is expected that only the EU production of whey powders could grow (+1%), related to an increase of the cheese production.

Given the current price levels of these milk powders, it is still assumed to be a cheaper alternative to other milk powders in some processing applications, thus supporting some domestic use increase (+2.4%).

Contrarily, EU shipments could decline (-2%), driven mainly by a reduced demand from China.