Mercosur and other FTAs to boost EU exports by almost €4bn

A study assessing the potential impact of 10 free trade agreements (FTAs) - recently concluded or currently under negotiation - confirms that the EU trade approach opens new commercial opportunities for EU agri-food exporters.

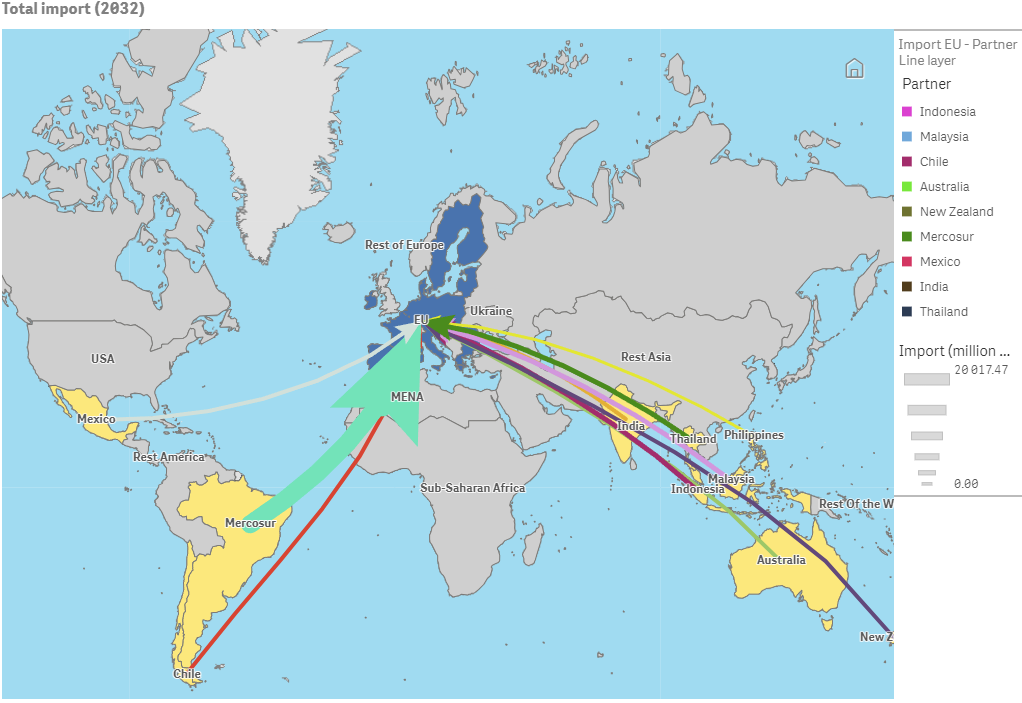

Engaging in preferential trade relations diversifies import sources, improving the resilience of EU food supply chains, according to the research by the European Commission's Joint Research Centre (JRC).

According to the commission, the development of new markets through preferential trade relations will help consolidate the EU's position as the world's top exporter of agri-food products; in 2022, the EU's positive agri-trade balance reached €58 billion.

A recent report on diversification in the EU agri-food trade showed that the EU position as the world's top exporter and one of the top importers of agri-food products allows for balanced and favourable trade relations with third countries.

Exports

The study published today (Thursday, February 22) focuses on the agreements with Australia, Chile, India, Indonesia, Malaysia, Mercosur (Argentina, Brazil, Paraguay, and Uruguay), Mexico, New Zealand, the Philippines, and Thailand.

These are agreements which are all either currently negotiated or concluded but not yet implemented.

It is estimated that the value of EU agri-food exports would be between €3.1 billion and €4.4 billion higher in 2032 than they would have been without these 10 trade agreements.

Trade opportunities are expected to develop for EU agri-food commodities, such as dairy (+€780 million), wine and other beverages (+€654 million), and processed agri-food products (+€1.3 billion).

Imports

Upon the entry into force of the 10 trade agreements covered in the study, the value of EU imports is expected to be between €3.1 billion to €4.1 billion higher in 2032 than it would have been without these agreements.

This would result in a balanced increase of both exports and imports, with the overall EU trade balance slightly increasing as a result, according to the research.

The study acknowledges that some sensitive sectors, notably beef, sheep meat, poultry, rice and sugar, are expected to face increased competition by the 10 partners referred to in the study.

According to the JRC, this conclusion validates the current EU approach of systematically protecting sensitive sectors with carefully calibrated tariff rate quotas (TRQs).

It said that this essential tool in trade agreements can help mitigate possible market disruptions, providing protections to EU farmers and agri-food producers.

For the first time, the commission's study also looks at the impact on EU agriculture of the trade agreements recently concluded by the UK with Australia, New Zealand and the member countries of the Comprehensive and Progressive Agreement for trans-Pacific Partnership (CPTPP).

The study shows that these trade partners will take some shares from EU producers in the UK market.

The resulting impact would be limited and the EU is still expected to remain among the main suppliers of the UK, according to the commission.

Nevertheless, some impacts are expected for sectors such as beef, wine and other beverages (and tobacco), processed food, dairy and sheep meat.

However, the commission has argued that the overall positive impact of the 10 trade agreements that could enter into force would compensate the market losses from the UK trade agenda.

Study of FTAs

The study published today is the second update of the 2016 initial study on cumulative economic impact of upcoming trade agreements on EU agriculture.

The first update was published in 2021. It aims to provide valuable insights for policy makers and negotiators on the link between the EU trade agenda and EU agriculture, by assessing two different scenarios depending on the extent of liberalisation efforts.

It does not replace the broader and more detailed impact assessments carried out for each individual trade agreement negotiation.

In today's study, the more ambitious scenario analysed corresponds to a full liberalisation of 98.5% of all products, and a partial tariff cut of 50% for the remaining products while the more conservative scenario would be a liberalisation of 97%, and a 25% tariff cut for the other products.

The model used relies on the tariff in 2014, 2022 and a projection of 2032.

Trade agreements that entered into force several years ago (e.g., with Switzerland, Ukraine, Colombia, Peru, Ecuador, South Korea, Canada, Japan or Vietnam) are taken into account in the baseline as well as the autonomous trade measures with Ukraine for the year 2022.