Beef trade: The stagnation continues

The factory/farmer stalemate has continued and farmers selling cattle this week will find that processors have opted to keep quotes at last week’s levels.

Plants are starting negotiations at 395-400c/kg for steers and 405-410c/kg for heifers. Some farmers, especially those with large numbers of in-spec stock to market, have been receiving prices of 5c/kg above base quotes. At the upper end of the scale, this brings steers to 405c/kg and heifers to 415c/kg.

Again, deals are also being done on transport to encourage farmers to offload supplies.

During the week ending April 1, in-spec, R+3= steers made a top price of 424.97c/kg, while the average price paid stood at 414.33c/kg.

Furthermore, a top price of 440.36c/kg was achieved for R+3= heifers; the average price paid for these animals stood at 428.77c/kg.

Cow prices

Like the prime cattle market, cow prices have remained relatively unchanged. However, there is quite a variation in prices quoted to farmers and this depends on the quality and grades being presented. The location and demand of individual processing plants also has to be factored into the equation.

Buyers are offering 320-340c/kg to purchase P-grade animals. In addition, procurement managers are starting negotiations with farmers for O-grade and R-grade cows at 340c/kg and 355c/kg respectively.

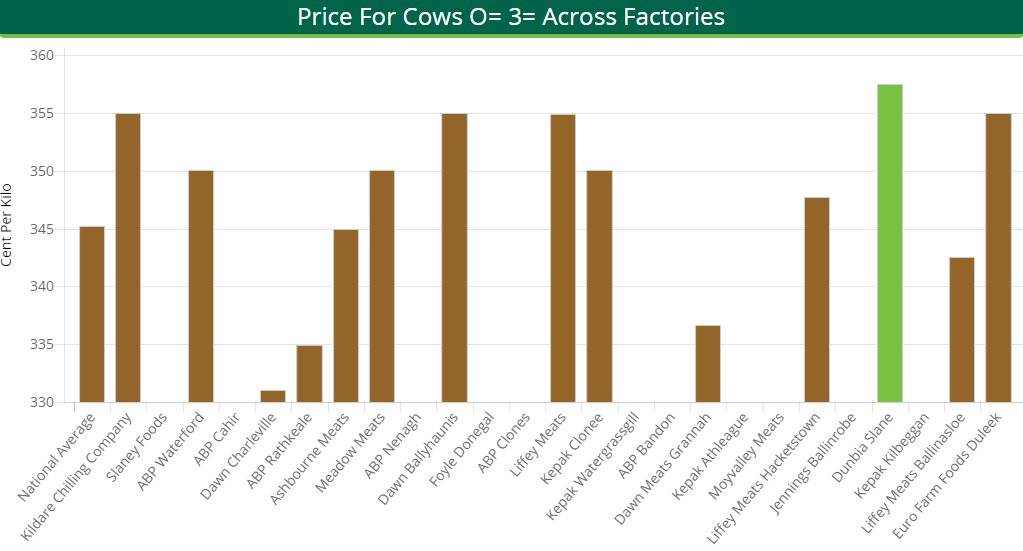

During the week ending April 1, O=3= cows made a top price of 357.52c/kg, while the average price paid stood at 345.19c/kg.

Supply update

The latest data from the Department of Agriculture’s beef kill database show that some 11,846 steers were slaughtered in approved export plants during the week ending April 1 – an increase of 155 head.

However, heifer numbers decreased during the last week of March. Official figures show that 9,400 heifers were bought by beef factories – an decrease of 14 head or 0.1% on the week before.

An increase was also witnessed in both the young bull and aged bull categories – up 171 head and 15 head respectively.

In total, some 32,812 head of cattle were sent for slaughter – an increase of 856 head or 2.6%. Much of this increase can be attributed to cow throughput. Week-on-week supplies of these animals grew by 529 head or 7.1% during the week ending April 1.

‘Finished cattle supplies to tighten’

The Irish Farmers’ Association’s (IFA’s) national livestock chairman Angus Woods outlined that procurement managers are on the hunt for cattle.

He said: “Agents are saying that, based on their usual supply lines, they don’t know where they are going to get finished cattle in ten days to two weeks’ time and they expect prices to rise significantly.”

Woods also highlighted that cattle prices in the UK have increased and are running 14p/kg ahead of last year’s levels. He added: “Cattle prices in our main export market are the equivalent to 443c/kg and there is significant potential for factories to increase prices to feeders.”

Moving to the main European markets, Woods outlined that prices remain strong; R3 bulls are making 427c/kg in Germany (including VAT) and 413c/kg in Italy and Spain.