Beef production in Europe is down - Rabobank

Consumer demand for beef continues to be under pressure because food price inflation remains high in the European Union (EU), according to a new report from Rabobank.

The bank has warned that beef consumption is likely to be "under downward pressure" as latest figures show inflation drove food prices up by 13.6% year on year in April 2023.

The latest Global Beef Quarterly report published by the bank shows that beef carcass prices in the EU have seen a "gradual softening" in recent weeks.

The EU average beef carcass price, according to Rabobank, has been marginally higher this year compared to where it was in 2022, however it is still sitting at 23% higher than the five year average.

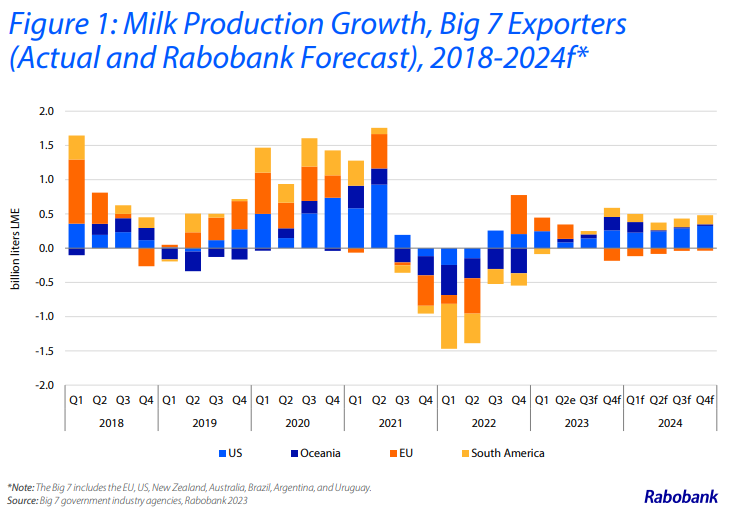

The bank's latest report also highlights that the easing of carcass prices in the EU has been largely driven by "an expanding supply of cattle" and this, it outlined, is a knock on effect of the correction in milk prices.

Rabobank expects that this trend will lead to higher slaughter rates in Europe to mirror the decline in milk prices.

One other key trend noted by Rabobank was a decline of 2.2% in beef production across the European Union and in the UK in the 12 months up to February.

The bank expects this "structural decline" to continue into quarter three.

The biggest decline in production in any European country so far this year has been in Italy where it slumped by 20% but Spain also recorded a 6% drop in production while Germany said there had been a 1% drop in beef production.

Meanwhile France recorded a 1% increase in production while the Netherlands recorded an increase in beef production of 9%.

Beef exports and imports

According to Rabobank there has been a pattern of declining beef exports from the EU and UK but a definite increase in imports.

Beef exports from the EU and UK were down by 22% in the year to date while imports had risen by 6%.

But one key exception to this was that total exports to Hong Kong tripled year on year in February -although volumes remained quite small.

Rabobank noted that Irish beef exports to China had resumed after the bovine spongiform encephalopathy (BSE) - related ban was lifted at the beginning of this year and the first shipment from Ireland had arrive in China in April.

The latest Global Beef Quarterly report also highlights that there has been a higher volume of imports into Europe and the UK from Argentina - which jumped by 43% and the United States also up by 42%.

There was a slight fall in imports from Brazil which dipped by 2% but overall the country remained the number one beef supplier into Europe.

Global outlook

Beef supplies will remain "balanced" over the next 12 months according to Rabobank but there are a number issues that could dominate on the horizon.

Cattle prices in the United State and Canada have hit record highs driven by "declining production volumes and firm demand" which is in stark contrast to other countries and regions the bank detailed.

Research analysts at the bank have highlighted that both Brazil and Australia are relying on an increase in export volumes as domestic consumption "remains static or in decline".

Specific to Australia Rabobank noted that the "closure" of live exports will have an impact on its beef market and that staff shortages and "low availability of skilled workers" could damped slaughter volumes.

Analysts also believe that beef imports to China, which was considered a growth opportunity as the country emerged from Covid-19 lockdowns in late 2022, will slow in quarter two and potentially decline in quarter three.

Rabobank has also stressed in its latest report that a key market to keep a close eye on in the coming months will be Argentina.

Angus Gidley-Baird, senior analyst – animal protein at Rabobank said:

“The landscape of Argentina’s beef industry is changing.

“Despite export restrictions in an effort to curb rising inflation and limit rising beef prices, beef exports have increased. This is partly due to increased Chinese demand.”