Rabobank: Global beef demand likely to remain steady

According to a new Rabobank report, global beef demand is likely to remain steady in 2024 despite economic challenges and consumer shifts toward lower-priced proteins, but trade flows are shifting.

Across most markets, beef retail prices have risen since 2019, and the impact of inflation in 2022 and 2023 added to the cost of living, pressuring consumers’ budgets and changing spending patterns.

With consumers trending toward cheaper options in 2023, foodservice and retail companies began promoting value-based propositions more frequently, some of which outperformed, according to the research.

Angus Gidley-Baird, senior analyst – Animal Protein at Rabobank said: “While there was some channel shifting and movement to lower-priced options for beef, overall demand held up relatively well in 2023, supporting consumption levels."

Pressure on consumers

However, Rabobank expects GDP growth rates to slow and unemployment rates to rise in many countries in 2024.

Rising unemployment suggests that upward pressure on wages should ease, and if inflation remains high, real wages should decline, putting more pressure on household income, according to the research.

“Questions about economic performance, income levels, costs, and the direction of monetary policy remain unanswered, but we expect overall beef demand to hold in 2024 and, therefore, consumption levels to remain steady,” Gidley-Baird added.

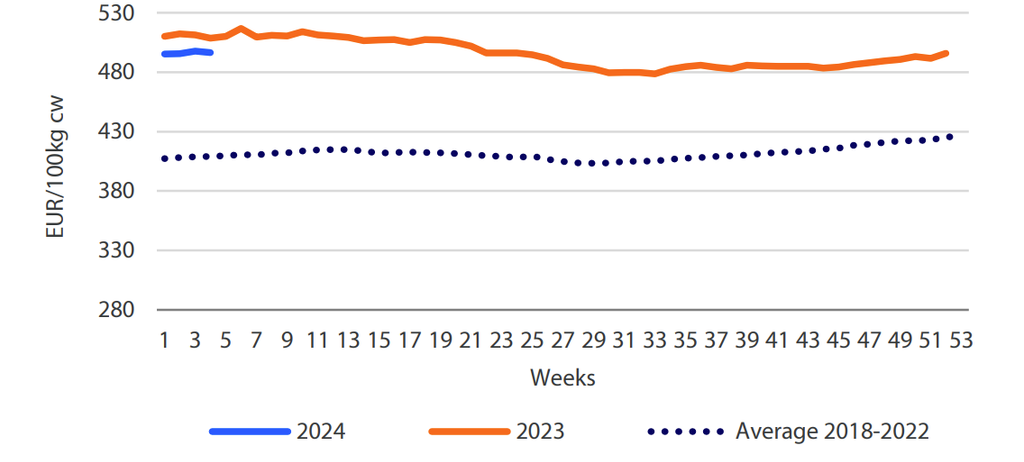

Despite the economic headwinds, Rabobank maintains a neutral outlook for global beef production, with increases in Australia and Brazil offsetting declines in Europe and the US.

“Without strong demand pulling volume through the supply chain and bidding prices up, price setting falls back to the producer end of the chain and, with it, increased exposure to seasonal conditions and producer sentiment,” Gidley-Baird explained.

The strength of the economic outlook in different beef-consuming markets creates an interesting overlay to the global beef production situation and the balance of trade, according to Rabobank.

“With limited or negative real wage growth expected in 2024, coupled with the higher cost environment, we believe global beef consumption will, at best, remain steady and possibly decline through 2024, with some notable regional variations,” Gidley-Baird continued.

Beef producers and price

For those in the supply chain, this poses important questions around margins and trade.

Rabobank has said that one questions which arises is 'can prices be maintained or pushed higher to make up for the loss of consumption, or do retail prices have to ease to encourage higher consumption'?

In a market where beef production growth is limited – the US for instance – the consumer may be willing to tolerate higher prices at the expense of some consumption, i.e., maintaining demand, accordng to Rabobank.

On the other hand, in a market with growing supply – such as Australia – lower prices may be needed to encourage consumption.

The research suggests that China’s import demand should remain sluggish in 2024 – at least in the first half – and with demand strength and lower domestic supplies in the US market, beef trade is being diverted.

“Brazil’s exports to the US in January 2024 were ahead of 2023, and Australian volumes were up 127% year-on-year," Gidley-Baird continued.

"If China’s recovery is better than expected, global beef markets could become quite tight, fueling price rises."

Due to its reasonable economic outlook and lower domestic supplies, the US is likely to lead the beef price-setting market and draw increased volumes from Australia, New Zealand, Brazil, Canada, and Mexico.

“But value will become the predominant theme across most markets in order to retain consumers faced with balancing the tighter economic condition," he concluded.