‘Agflation’ breaks through the 30% barrier

UK ‘agflation’ has been soaring since the beginning of the year and shows no sign of flattening off, according to farm business consultancy, The Andersons Centre.

This trend has been driven, primarily, by the Russia-Ukraine conflict.

AgflationThe term 'agflation' has been coined to specifically reflect the cost pressures on farming businesses.

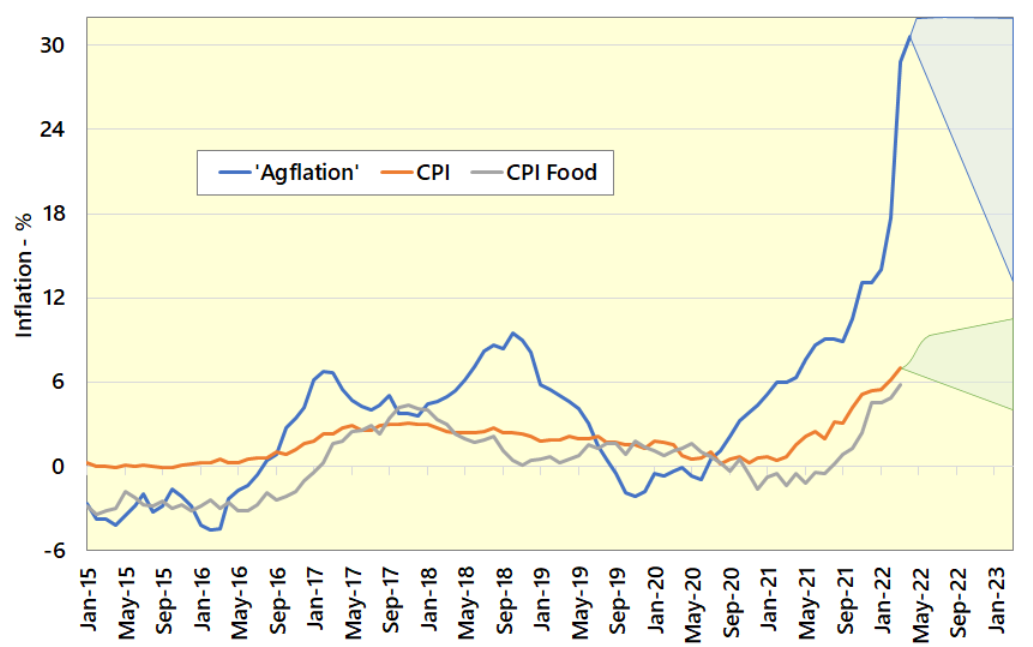

The latest estimates for April show that the index now stands at 30.6% – levels not seen in a very long time.

All the while, general inflation, as measured by the consumer price index (CPI) and food prices (CPI Food) have been rising at a much slower rate - circa 6%.

This means that many farm businesses are now feeling a severe squeeze on margins and this is set to continue for the foreseeable future.

Northern Ireland is included within the remit of the UK-wide index.

Agflation trends

However, director of The Andersons Centre, Michael Haverty, has confirmed that the agflation trends identified in the UK are equally relevant, where Irish agriculture is concerned.

“I am basing this very much on the anecdotal evidence currently available,” he said.

The agflation index builds upon official price indices for agricultural inputs and weights each input cost (e.g. animal feed) by overall farm spend by UK farmers.

The Andersons Centre then provides a more up-to-date estimate of the price index for each input cost category.The most recent figures confirm that the Russia-Ukraine conflict has had most effect on feed, fuel, and fertiliser prices.

However, as these underpin most agricultural inputs in some form, cost increases are also showing elsewhere (e.g., contracting costs, crop protection products, and building materials).

Several livestock sectors are now showing signs of ‘stress’. The pressure is most pronounced in the pig and poultry sectors where feed traditionally accounts for 65-80% of production cost.

Dairying and grazing livestock are also feeling the strain, particularly for those farms that have not bought forward their fertiliser.

According to The Andersons Centre's analysis, the tillage sector is less affected for 2022 as most farmers had bought forward their fertiliser, and output prices have hit record levels recently.

For many farmers in this position, 2022 is shaping up to be a stellar year: The value of the yet-to-be-harvested wheat crop has risen by more than 50% since it went in the ground.

But significant challenges loom for 2023. It is envisaged that high input costs and taxation on 2022 profits will stretch working capital requirements.

According to The Andersons Centre, without significant price increases to cover elevated production costs, many farms will struggle during the period ahead.

In such times, it is especially crucial to demonstrate competent cost management.