There was some good news this morning as the Minister for Agriculture, Michael Creed, announced the opening of the Chinese market to Irish beef. However, only time will tell if primary producers will reap the rewards of this market access.

Also Read: Don’t judge Chinese beef access until it puts money in farmers’ pocketsDespite this morning’s announcement, there has been little movement in the prices beef factories are offering for steers and heifers; many have opted to maintain quotes at last week’s levels.

For the most part, factories are offering 400c/kg for steers and 410c/kg for heifers. These quotes exclude Quality Assurance (QA) bonus payments.

However, some finishers have noted that buyers are willing to pay 5c/kg on top of the base quotes to secure supplies. At the upper end of the scale, this brings steers to 405c/kg and heifers to 415c/kg.

During the week ending April 8, in-spec, R+3= steers made a top price of 432.98c/kg, while the average price paid stood at 417.60c/kg. These prices are inclusive of breed-specific and QA bonuses where applicable.

Moving to heifers, a top price of 438.89c/kg was achieved for R+3= heifers; the average price paid for these animals stood at 431.19c/kg.

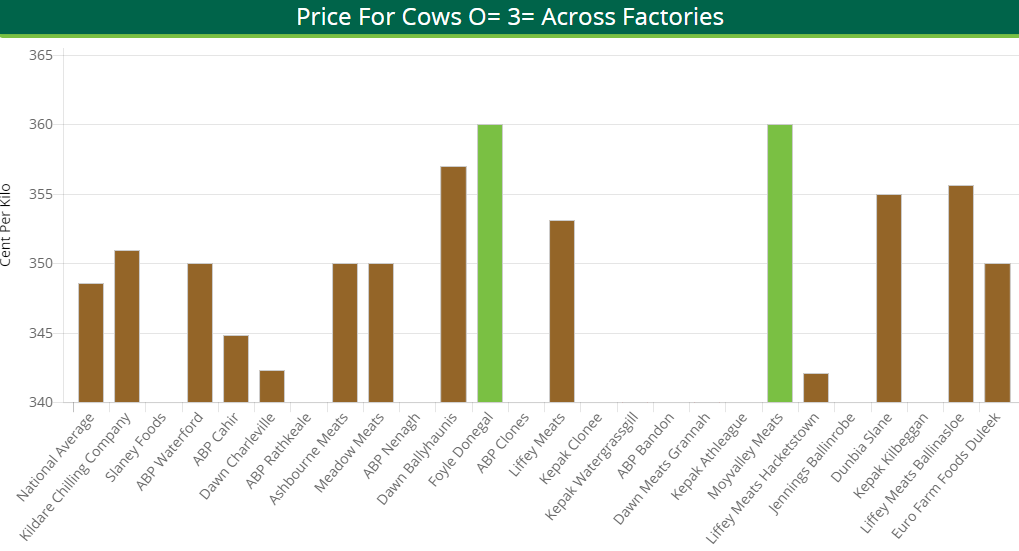

The cow trade

The demand for manufacturing beef remains strong and most buyers are offering 320-340c/kg for P-grade animals. Procurement managers are starting negotiations with farmers for O-grade and R-grade cows at 340c/kg and 355c/kg respectively.

However, it must be noted that there is a wide variation in the prices being quoted to farmers. This depends on the location and demand of individual processing plants.

Cattle throughput

There was a decrease in the number of cattle slaughtered in Department of Agriculture approved beef export plants during the week ending April 8; this was mainly due to the Easter public holiday (April 2).

In total, some 32,514 cattle were slaughtered during that week – a decrease of 1% or 298 head on the number processed one week earlier.

During the week ending April 8, some 11,757 steers were slaughtered – a fall of 89 head or 0.7% on the quantity witnessed during the preceding week.

In addition, young bull slaughterings also decreased by 487 head. However, aged bull numbers increased by nine head, while 275 more cows were processed that week. Furthermore, the number of heifers killed in beef plants amounted to 9,334 – a decrease of 66 head.

- Young bulls: 3,058 head (-427 head or -12%);

- Bulls: 676 head (+9 head or +1.3%);

- Steers: 11,757 head (-89 head or -0.75%);

- Cows: 7,689 head (+275 head or +3.7%);

- Heifers: 9,334 head (-66 head or -0.7%);

- Total: 32,514 head (-298 head or -1%).

The trade in Britain

The Irish Farmers’ Association’s (IFA’s) national livestock chairman Angus Woods indicated that cattle prices in the UK have increased and R3 steers are now trading at the equivalent of 447c/kg (including VAT).

In Britain, the Agriculture and Horticulture Development Board (AHDB) reported that – during the week ending April 8 – R4 steers made 372.3p/kg (430c/kg). R4 heifers also made the equivalent of 430c/kg.

Looking at young bull returns, it was reported that overall prices amounted to 338.7p/kg (390c/kg); R4 young bull prices increased by 7.3p/kg (8c/kg) to the equivalent of 417c/kg on the previous week.

Overall cow prices were reported to have decreased during the week ending April 8. However, prices for cows falling into the O-grade category increased. These animals made the equivalent of 324c/kg.

According to the AHDB, the diverging trend between the overall price and the ‘in-spec’ price indicates that beef processors are keen for prime cattle meeting the more desirable specifications.

Data source: AHDB